Why You Can Trust CNET

Why You Can Trust CNET Advertiser Disclosure

Apple Card, Venmo Card and PayPal Card: Which should you get?

Here's how different digital credit cards stack up.

- Named a Tech Media Trailblazer by the Consumer Technology Association in 2019, a winner of SPJ NorCal's Excellence in Journalism Awards in 2022 and has three times been a finalist in the LA Press Club's National Arts & Entertainment Journalism Awards.

Apple Card rolls out this summer.

This article was originally published on May 29, 2019. Some of the features and offers described below may have changed or expired since then.

When Tim Cook launched Apple Card at a March event, he vowed in typical Apple fashion it would shake up the industry.

"There are some things about the credit card experience that could be so much better," Apple's CEO said. Apple Card, he noted, would eliminate fees, offer clear rewards programs and provide security and privacy. "We're going to do all of this and so much more, changing the entire credit card experience."

This story is part of CNET's ongoing Follow the Money series.

It's not just Apple Card that's looking to revamp the scene. Tech companies including PayPal , Amazon and Square have also supplemented their digital services with physical credit and debit cards that offer a range of perks, from ATM withdrawals and cash-back rewards at restaurants to zero monthly fees. They also offer integration with online payment platforms many people have come to rely on and trust.

Now with the array of credit and debit cards on the market, it can be hard to know which one is right for you or whether digital cards offer anything you won't get with traditional bank cards. Keeping a few key points in mind can help guide your decision.

How to choose a card

If you're a die-hard Apple fan, you may be tempted to get Apple Card simply because of the brand name. (The same goes for users of Venmo , PayPal, Square, etc.)

But it's better to base your decision on the rewards and fees associated with a card and see what best fits your financial situation, says Jim Miller, vice president of the banking and credit card practice at J.D. Power.

The rewards that accompany a card can be tempting, but Miller cautions against spending more than you have just to rack them up. If you carry a balance, focus on getting a card with the lowest interest rate and paying down that balance. "You'll never get enough in rewards to offset a high interest rate," Miller says. "Shop first for interest rates rather than rewards or the technology."

Users of the PayPal Cash Card can access money in their PayPal account and spend it anywhere Mastercard is accepted.

Also familiarize yourself with the user and cardholder agreements to find out if your funds are protected. Venmo Debit Card and Square Card debit cards, for example, aren't FDIC insured. That means that in the unlikely event Venmo or Square shut down, you'd lose your money. Customers are, however, protected against fraud or stolen funds, and Square says it's "actively working to address" its lack of FDIC coverage.

It may be a good idea to keep a little cash in your Venmo account, but it's probably best not to carry a large balance in there for long since Venmo doesn't pay any interest.

Still, the PayPal Cash Card and Square Card are viable options for people who don't have or want a traditional bank account. All you'll need to do is sign up for PayPal or Venmo and apply for the companies' debit cards to access your balance.

Apple Card rewards

There's a lot of buzz surrounding Apple Card, which will roll out in the US this summer. It'll be both a virtual offering in Apple's Wallet app and a physical titanium card.

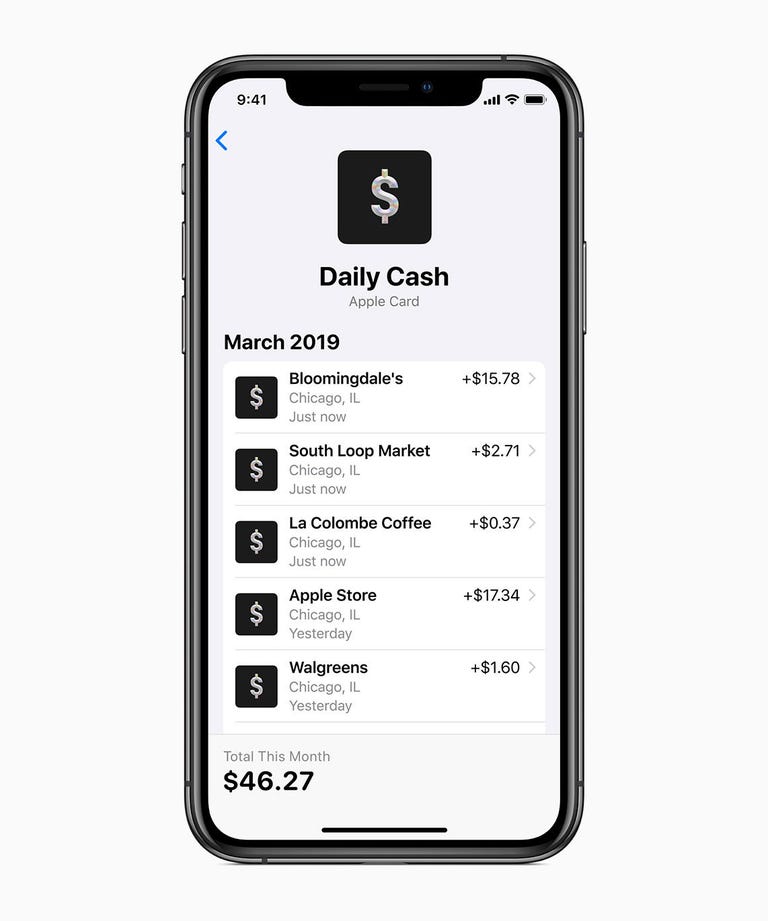

Apple touts benefits like Daily Cash, a cash-back reward that's added to a customer's Apple Cash card each day. Daily Cash can be used immediately for items bought using Apple Pay, or it can go toward an Apple Card balance. It can also be sent to friends and family via Messages.

Purchases made using Apple Card with Apple Pay will get you 2% Daily Cash. Those made for Apple products and services will get you 3% cash back.

Apple Card offers Daily Cash, a cash-back reward that's added to a user's Apple Cash card every day.

"That's a benefit if you buy enough in Apple products to make it worthwhile," Miller said.

The flashy laser-etched titanium card could be a status symbol, he adds, but the physical card offers just 1% cash back, which is relatively low. "When you pull out the cool card," he said, "you're probably making a financial mistake."

Ultimately, Apple Card isn't offering anything unprecedented. Other cards on the market have similar rewards.

Customization and convenience

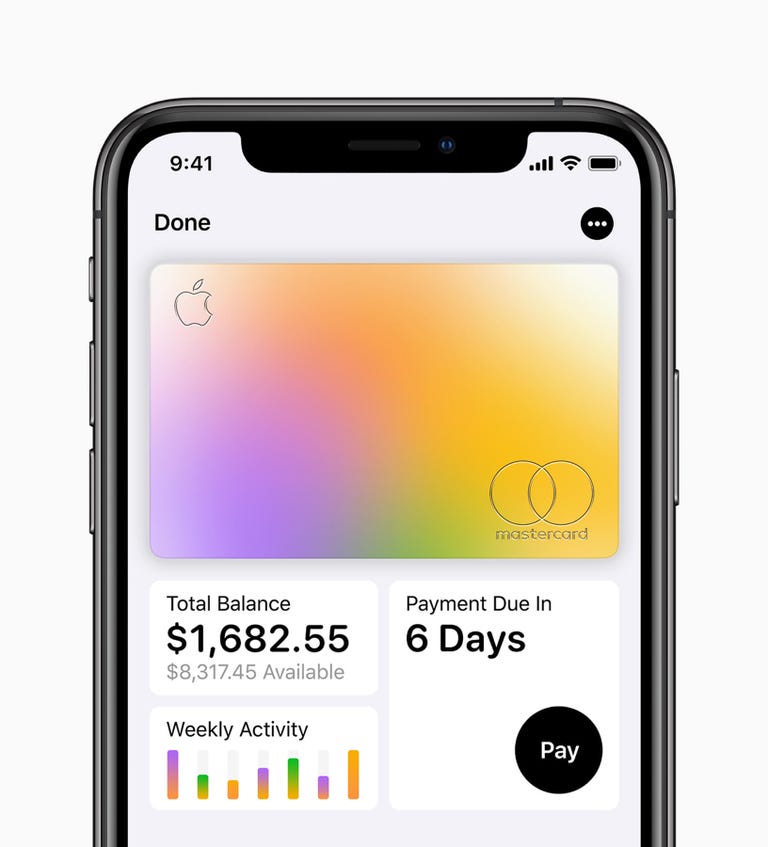

Apple Card offers perks such as no annual, late or international fees. The company says its goal is to "provide interest rates that are among the lowest in the industry." Apple Card will suggest customers pay more than the minimum owed each month to lower how much they pay in interest, and they'll have the option to schedule more frequent payments.

Another perk is being able to sign up for the card right from the Wallet app on an iPhone .

Customers can view weekly and monthly summaries of their spending, and purchases are organized based on categories such as entertainment, shopping and food.

Read more: The best tax software

Apple Card users can see weekly and monthly summaries of their spending.

Ultimately, the card's user interface, customer experience and customized credit are what set it apart, says payments consultant Richard Crone.

"No other credit card issuer allows you to specify your terms as easily," he said.

There's also the undeniable power of the Apple brand, which will help attract people to the card, says Sara Rathner, credit card specialist at NerdWallet. Anyone who already has Apple products is likely to spend money at an Apple Store and can therefore reap the 3% cash-back benefit.

"They're definitely creating another level of brand loyalty where a certain high level of brand loyalty already exists," she said.

Other digital cards: PayPal, Venmo and Square

Other companies are also banking on brand recognition and special perks.

The PayPal Cash Card offers free signup, no monthly fees and no minimum balance requirement. Users can access the money in their PayPal account and spend it online or in stores that accept Mastercard . They can also withdraw cash from ATMs worldwide.

PayPal also has a credit card, with 2% cash back and no annual fee.

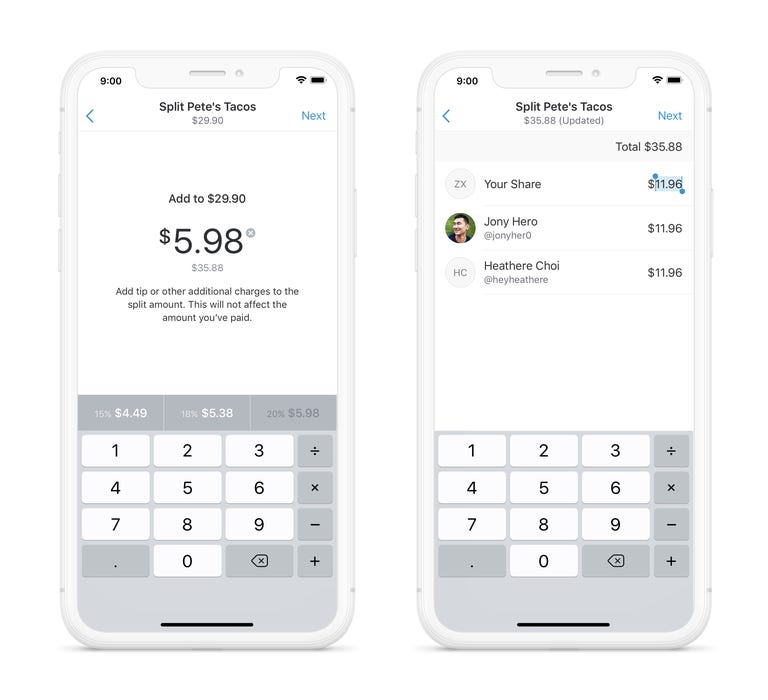

Venmo Card lets users split purchases with friends via the app.

Venmo, which is owned by PayPal, offers a debit card that's linked to a user's Venmo account. It can be used anywhere Mastercard is accepted in the US.

The Venmo Card lets users pay with the card and then split purchases in the app. They can also withdraw cash from MoneyPass ATMs in the US at no cost. There is one key drawback: the Venmo Card doesn't work overseas, so it won't make for a good travel companion.

Square launched a free business debit card in January that offers sellers a 2.75% discount on purchases made from other Square sellers. Customers can use Square Card wherever Mastercard debit cards are accepted and can withdraw cash at ATMs.

The company charges business owners a processing fee of 2.75% on swiped credit and debit card transactions, so Square Card owners can regain those funds by using the card.

Square also offers Cash Card, a Visa debit card that can be used to make purchases using your Cash App balance. You can use Cash Card's Boost feature to get discounts at certain businesses, such as coffee shops and Chipotle.

Square's free business debit card offers sellers a 2.75% discount on purchases made from other Square sellers.

Other tech companies have also rolled out cards that don't necessarily have a digital connection.

Ultimately, Crone says, customers should pick a card with rich rewards that are accessible and useful. That can vary depending on what you're looking for, so figure out what's most important to you -- rewards at restaurants, airline miles, cash back -- and go from there.

*All information about the PayPal Cash Card and Square Cash Card has been collected independently by CNET and has not been reviewed by the issuer.