Coin delays product launch until spring 2015 as questions remain

The startup behind a smart electronic device that stores credit and debit cards will offer a beta program for 10,000 customers.

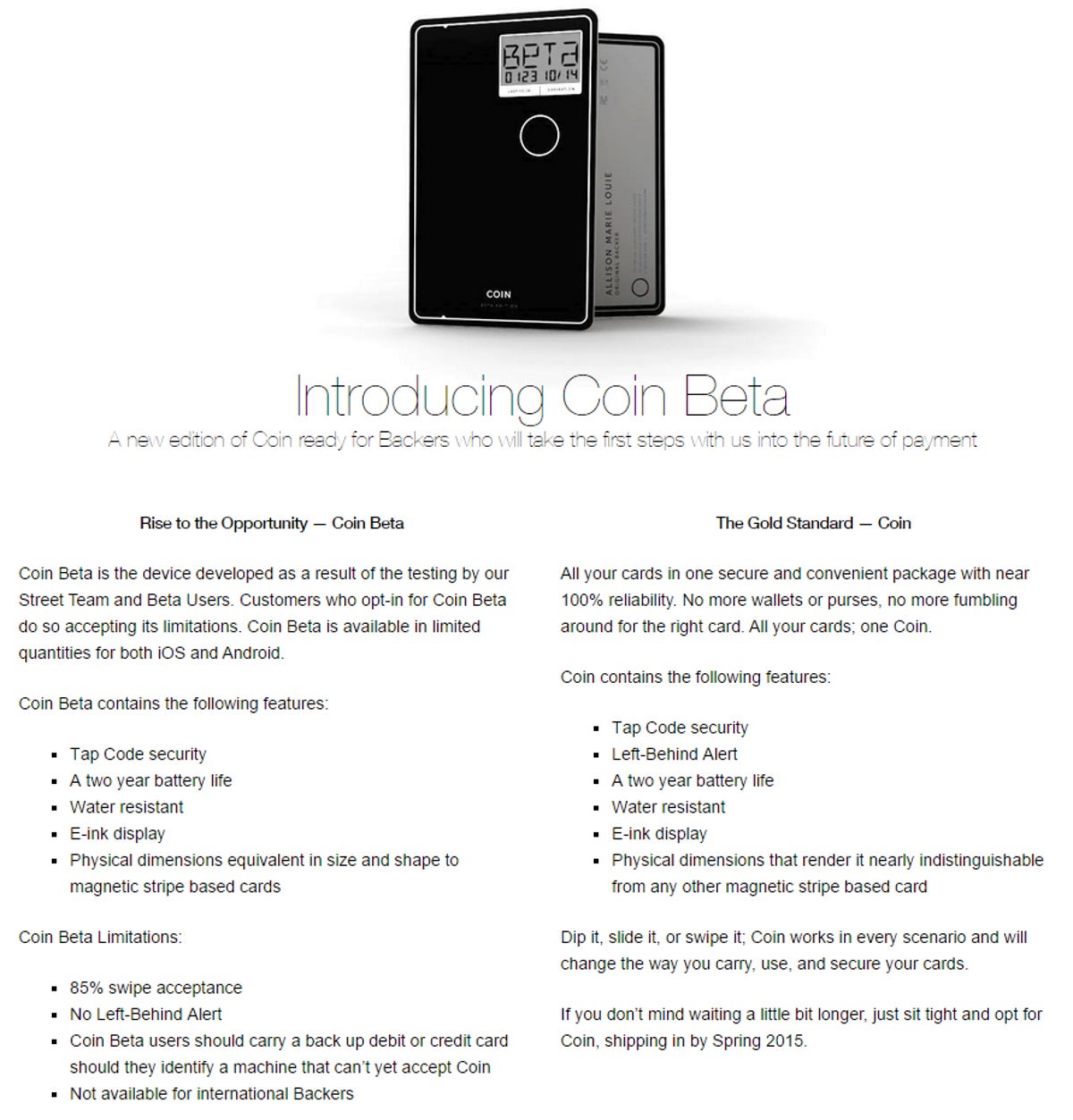

Coin, the makers of an electronic device that works like a credit and debit card by storing information on all on your cards, is taking a pause.

On Friday, the startup said it's delaying its full product release until spring of 2015 while it refines the device and works out kinks in manufacturing. Instead, the company says it will ship what it's calling Coin beta, the latest iteration of the all-in-one card, to the first 10,000 pre-order customers who opt-in to the program.

The pushed back shipping date is not Coin's only cause for concern. Complicating the company's roadmap is the absence of a specialized security microchip that is in the process of being adopted by the US credit card industry. When the consumer version of Coin launches next year, it will not contain such a chip. The company has said that it will only begin addressing that issue after its current product begins shipping next spring.

Customers who spent $55 to pre-order the device last year have also expressed concerns that Coin's promise to bring technology's simplicity to our wallets may already be behind the times. Coin has worked to address criticism by publishing periodic progress reports for its pre-order customers. Notably absent, however, has been discussion about these security chips.

"Coin, being in this business, has to know the changes in this industry," a pre-order customer calling himself Robert Jon commented on one of the company's blog posts. "It's their business to know this information."

A coming struggle

Though Coin represents a platform and a product that hopes to be the future of how we pay for groceries, gas and restaurant bills, the device being released next year isn't future-proof.

The Coin device is deceptively simple. It's roughly the same height, weight and girth of a typical credit card. But that's where the similarities end. A tiny screen occupies the top right corner of its face, with a button below. Press the button, and the screen comes to life, displaying the name of a credit card, the last four digits and its expiration date.

The technology Coin developed allows the device to replicate the magnetic strip on the back of a typical credit, debit or gift card. It's programmed wirelessly by a smartphone app, where users store card information. How does that credit and debit card data get in there? By having people swipe their plastic through a dongle that attaches to their phone.

The end result is an all-in-one-card that aims to slim our wallets by storing up to eight cards in its memory. Users can switch between them by clicking the card's button.

Though the product caught fire among early adopters in the Bay Area last year, it inspired cheeky condemnations and mocking write-offs, with headlines like Hot New Startup No One Needs: A Credit Card for Your Credit Cards from Gawker's Valleywag blog. While there's debate over the usefulness of a device that slims down your wallet, the pressing problem is not Coin's mission, but what's missing from its prototype -- and the product that comes after.

The US credit card industry is preparing for one of its biggest technological leaps in decades. New cards arriving in customer's mailboxes are being affixed with security chips, called "EMV." These chips promise to reduce fraud by making it hard to quickly copy a card's information, and by requiring that customers sometimes punch in a passcode.

By October 2015, the industry has said it will change its business practices, shifting liability for any fraud to merchants and card makers who don't upgrade to the new technology.

Coin may be one of them.

The San Francisco-based company, which transitioned from a cramped office in the city's South of Market district to occupying an entire floor of a nondescript building down the street, won't say it's researching new technology to meet these requirements. It also doesn't have a definitive answer for how merchants will react when the new security technology becomes the rule, not the exception.

Kanishk Parashar, the CEO and co-founder of Coin, said the company hasn't begun research and development of a next-generation product yet. "What we'll do is that once we get through this first shipment of Coins, we'll be able to have enough resources to do an R&D project," he said in an interview with CNET.

The time frame? "I don't know exactly," Parashar said. Coin has been in the works for nearly two years, subsisting on Y Combinator and K9 Venture funding, as well as the backing of former Google Wallet head Osama Bedier. Since launching its pre-order campaign, however, Coin, has taken in additional funding from customers.

By the end of 2015, some 575 million cards in the US are expected to have chips, according to the Payments Security Task Force, a consortium of the country's largest card issuers. At least half of credit card processing terminals will also support the chips by then.

The switch: for your protection

The goal of the EMV standard is to phase out reliance on magnetic stripes, which have been around for decades and are subject to all manners of fraud. The microchip generates a unique code for every transaction, and inside the chip is what MasterCard spokesperson Oliver Manihan calls a black box: a private section in which a cardholder's PIN and the cryptographic keys used to generate code are located.

As for Coin, even if it does find a way to include security chips on its device, Manihan said it may not be able to store information from the ones his company sends to customers. "You could only get a portion of the data," he said, adding that some of the information stored on the chips is designed to never be copied.

Manihan isn't ruling out that a device could somehow do what Coin is hoping it can achieve. But he's skeptical. "When you talk about copying the data from an EMV card and putting it on another card...that would be hard to do," he said.

Magnetic stripes won't be going away anytime soon -- but that's the ultimate goal, Manihan says.

Coin says the switch to EMV technology will be addressed in the future. Its devices are designed to only last about two years before the onboard battery dies.

In the meantime, the company says it will develop a device with a security chip in it, though Coin admits it doesn't know how that will work. In theory, the next generation Coin will be able to replicate the chip information of our new, safer, credit cards.

"We have good faith that it [Coin] will be able to do so," Parashar said.

The road to Coin 1.0

When Coin began taking pre-orders about a year ago, it said it planned to ship its device to customers this summer. The delay to 2015, Parashar says, was necessary to ensure Coin works as advertised in every corner of the country. Coin at the moment only works at 85 percent of credit card terminals in the US. The company is also working on finding a way to mass produce enough cards to fill demand.

The company of about 30 people has been creating prototypes and learning how to manufacture large quantities of the device. In March, it offered to give prototypes to about 1,000 customers in the San Francisco area. The plan is to expand that test to 10,000 nationwide.

Coin's latest round of prototypes will be sent out in September and October. Customers can opt in by downloading a mobile app from the company landing on Apple's iOS app store on August 28 and Android's Google Play store on September 25.

Customers originally paid $55 for the device, a price Coin claimed was half of what it will charge when it launches. Today, customers can pay $75, but that price will rise in mid-September. Customers can ask for a refund any time before Coin ships. If customers don't like the product, they cannot return it.

Parashar said the company received 20,000 orders -- at $55 that equates to $1.1 million -- in the first five hours last fall, but declined to say how many it has sold in total. If Coin sold only 100,000 more units over the next nine months, that would mean additional $5.5 million, though the discount has since shrunk, implying an increase in revenue for each unit sold.

While the 10,000 prototypes Coin sends to volunteers will work for up to two years, Coin will charge them $30 to upgrade to the finished product next year, but pledges it will offer 50 percent off any Coin products purchased over the next three years. The reason you may need to upgrade: to "make sure that consumers get the most functionality out of the most up-to-date Coin," Parashar said.