I Bonds' High Rate Makes Them a Great Last-Minute Christmas Gift

Learn how to buy I bonds online and print out a certificate for your recipient.

I bonds currently pay more interest than CDs or high-yield savings accounts.

Christmas arrives tomorrow, and if you're scrambling to find a last-minute present for anyone, consider the gift of financial stability and security. It's not hard to buy savings bonds online, and the current 6.89% rate on Series I savings bonds blows away the return you can get on CDs or high-yield savings accounts. The US Treasury even provides announcements that you can print out and wrap.

I bonds have a few catches, though. First, you'll need to hold the money in I bonds for at least a year, and you'll lose three months of interest if you cash them in before five years. Next, you can only buy $10,000 per year electronically, plus another $5,000 in paper bonds from your tax return.

However, you can buy as much I bonds as you like for other people, as long as you don't pass a $10,000 yearly threshold per person. The security of money in I bonds could be a great gift during a holiday season filled with economic uncertainty.

Also, the interest earned on I bonds can be tax free if it's used for higher education, making I bonds even more appealing to young people with college in their futures. Read on to learn exactly how to purchase Series I savings bonds for yourself or as a gift, step by step.

For more investing advice, see our best CD rates and best high-yield savings accounts.

How do I purchase I bonds?

I bonds are sold online at TreasuryDirect. All US citizens, young or old, can take ownership of $10,000 in electronic I bonds each year. Additional paper I bonds can only be bought with money from your tax refund, up to $5,000 per year (see more below).

To purchase Series I savings bonds online, you first need to create an account at TreasuryDirect. The process is about as bureaucratic as the site's name might suggest. There are no mobile apps or even a mobile version of the website.

I recommend using a laptop or desktop, or a device with a keyboard, because there's a lot of information to enter manually, and the Virtual Keyboard step is almost impossible on a phone screen.

TreasuryDirect was redesigned back in early October, and it does look much cleaner overall than before. The old landing page was jumbled with all sorts of links, while the new front page now is simple and direct. Most of the site, research and information sections on TreasuryDirect also sport the new, lighter look and feel.

However, the process for signing up for an account and buying I bonds is virtually unchanged and still looks the same as before the redesign.

Pro tip: Double-check your banking details. If you make a mistake with your banking information or have to change it for any reason, you'll need to mail in a paper form that is signed in the presence of an "authorized certifying official."

- Visit TreasuryDirect.gov and click on the green Open an Account link.

- Review the terms and conditions of the site and the information you'll need to open an account: Social Security number; email address; bank account and routing numbers.

- Click the blue Apply Now button.

- Select the Individual radio button and click Submit.

- Enter your personal information, including email address and banking account and routing details and click Submit.

- Review your info and click Submit.

- Select a personalized image and caption (security measure) and hit Submit.

- Choose a password and answer three security questions (I suggest recording your answers somewhere) and Submit again.

- TreasuryDirect will then email you an account number that is one letter followed by nine numbers. Record your account number.

- Go to the home page again and click on the TreasuryDirect login link, then click the orange Login button.

- Enter the account number that was emailed to you and hit Submit.

- Since it's your first login, TreasuryDirect will email you again with a one-time passcode -- check your email (and hang in there!).

- Enter your passcode and click "Register this computer" to avoid the one-time password at future logins.

- Enter your password. You can't paste it. You can't even type it! You need to enter it using your mouse and a virtual keyboard (sorry, fellow users of password managers).

- Exhale -- you're in.

You need a valid bank account and routing numbers to sign up for TreasuryDirect.

When I first purchased I bonds in August, I experienced more than a few hiccups in the process, including site outages that seemed to be related to high traffic. Based on my most recent time with the site, those pains could be lessening. In my latest trip in and out of TreasuryDirect, BuyDirect and ManageDirect, as well as most of the registration process, the site does seem more responsive.

Once you've gotten through the tricky part of creating a TreasuryDirect account and logging in, buying and cashing in I bonds isn't too bad of a process:

- After logging in, click BuyDirect at the top of the page.

- Under Savings Bonds, click the radio button for Series I then click Submit.

- On the BuyDirect page, enter the bond amount you'd like to purchase, any exact amount to the penny from $25 to $10,000.

- As an optional step, you can set up recurring I bond purchases at various time intervals like weekly or monthly.

- Confirm that your banking account info is correct and hit Submit.

- Review the terms of your purchase once more and hit Submit for a final time.

You can buy I bonds in any exact amount over $25 and under $10,000.

You just bought an I bond!

You'll need to wait one additional business day for the bond to show up in your TreasuryDirect account. But then it's yours to keep or sell (after a year) whenever you'd like.

How can I buy I bonds as gifts for other people?

It's not hard to purchase I bonds for someone else as a gift, but as you might guess, there are a few extra hoops to jump through on the TreasuryDirect site to do it. To give and deliver I bonds to another person, you'll need three pieces of info about them:

- Full name

- Social Security number

- TreasuryDirect account number

That's right -- if you want to give someone electronic I bonds, they'll need to have their own TreasuryDirect account. Unless you can get their account number surreptitiously, it's hard to make an I bond gift without a recipient's knowledge. If your recipient is a minor, they'll need an account that's linked to a custodial account (see below).

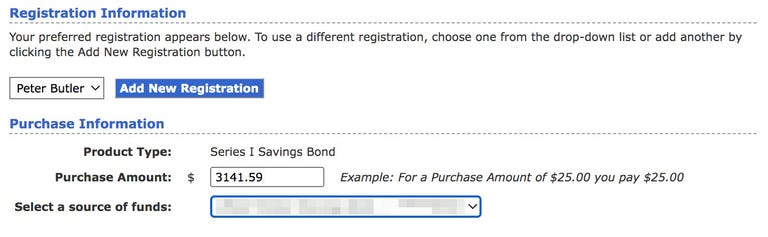

Once you've got the necessary info, log into TreasuryDirect, click BuyDirect and select I bonds, just as you would if you were buying them for yourself. However, when you get to the main purchase page for I bonds, click the blue Add New Registration button in the "Registration Information" section. This page is where you'll enter information about the person receiving your gift.

To give I bonds to another person, start by clicking the Add New Registration button.

On the new registration page, select Sole Owner and enter the personal details for your recipient, including their full name and Social Security (which is listed on the form as "Taxpayer Identification Number"), then hit Submit.

The person you just registered on your account should now be available from the drop-down menu in the Registration Information section of the BuyDirect purchase page. Select that person from the menu, enter the purchase amount of your gift, then hit Submit. You'll have one more chance to review your purchase, then hit Submit again to finalize it.

After you've purchased the I bonds, your gift needs to be delivered to your recipient. First, you'll need to hold the bonds for at least five business days, a self-imposed waiting period from TreasuryDirect to ensure your money has gone through its system. Then you'll need to deliver each gift manually.

To deliver an I bond, select Gift Box from the far right side of the upper navigation of TreasuryDirect. Here you can see all of your savings bonds gifts that are awaiting delivery. Select the gift purchase that you want to deliver and click Submit. You'll get a confirmation page that displays all of the information for that gift. If everything looks right, click Deliver to send it.

You're still not done. The following Delivery Request page is where you'll need to add your recipient's TreasuryDirect account number. Once you've entered the account number, click Submit, and you'll get one last chance to review all the information. Again, if everything looks correct on the Delivery Review page, click Submit to finally deliver your savings bonds gift and receive a confirmation page that you can print or save.

Your I bonds will be delivered with an email from the US Treasury announcing your gift. You can also print out a customized gift certificate from TreasuryDirect that can be wrapped for the holidays.

As far as paper savings bonds go, while the timing doesn't work well for the winter holiday season, you can buy paper I bonds as gifts when you file your yearly federal tax return. See below for more information on how to buy $5,000 in paper bonds with your tax refund.

How do I purchase I bonds for children?

If you want to buy I bonds for a child, click the blue Add New Registration button on the BuyDirect purchase page. Then, create a linked Minor Account before completing your purchase, following the same registration steps above.

Minor accounts are custodial accounts that can only be accessed by the primary account holder, that is, the parent or adult who opened the account. You can also use the Add New Registration button to buy gift I bonds for anyone with a Social Security number who is eligible.

How can I buy paper I bonds?

Paper I bonds can be purchased only when you file your tax return each year. To do it, use IRS Form 8888, Allocation of Refund, which is included in all leading tax software.

You can designate up to $5,000 a year total toward paper I bonds for two recipients -- that could be you and your spouse, but it can be any two people you like. Your paper bonds will be mailed about three weeks after the IRS processes your return.

Paper I bonds feature famous Americans such as Helen Keller and Dr. Martin Luther King Jr.

How do I cash out I bonds?

To cash out, or redeem, your electronic I bonds, you'll need to again log on to TreasuryDirect. Once you're on your My Account page:

- Click the ManageDirect link at the top of the page.

- Select the type of security (savings bonds) that you'd like to redeem and click Submit.

- Select all the individual I bonds that you'd like to cash out (up to 50 at a time) and click Submit.

- Choose the destination for your money on the Redemption Request or Multiple Redemption Request page and click Review.

- Review your information and Submit to complete the redemption.

- You've redeemed your bond(s) and your money is on its way.

You can cash out paper I bonds at most banks with physical branches, though your options there are dwindling.

If you don't have access to in-person banking, you can mail your paper bonds to Treasury Retail Securities Services, P.O. Box 9150, Minneapolis, MN 55480-9150 along with FS Form 1522 from the Bureau of the Fiscal Service.

You'll still need to provide account and routing numbers to cash out a paper bond through the mail. If you don't have a bank account, many prepaid debit cards include account and routing numbers that you can use with paper or electronic I bonds.

Remember, you need to wait at least one year to cash out an I bond. If possible, it's a good idea to wait five years or more to redeem this investment. If you cash it in before five years are up, you'll miss out on the last three months of interest earned.

For more low-risk investments, check out our lists of best high-yield savings accounts and best CD rates.