Why You Can Trust CNET

Why You Can Trust CNET The surprising history of credit cards: How this tech has evolved and where it's headed

The history of credit cards goes back further than you might think -- here's the origin story of this tech and some predictions about what their future holds.

At this point in time, it's an oddity to come across someone who doesn't have a credit card. More than three-quarters of US consumers have a credit or charge card. And you probably have more than one, as Americans have 3.84 credit cards in their wallets on average. As ubiquitous as they seem, however, credit cards as we know them are a relatively recent development -- Diners Club claims to have launched the first official charge card in 1950. But you can trace the roots of the modern-day credit card much further back in history.

What started as a simple piece of metal or plastic that let you purchase something at the store while paying for it later now lets you make digital payments worldwide, processed nearly instantly, using information you have securely stored on your phone or computer. In many cases, you no longer even need to carry a physical credit card with you. Take a look at how credit has evolved throughout history -- and what experts have to say about where credit cards are headed.

The history of credit cards

According to Lewis Mandell, author of Credit Card Industry: A History, the idea of credit can be traced back to agrarian life. Farmers needed to find a way to cover the cost of seeds and supplies at planting time and then pay back the debt later, after harvest. Here's a credit card timeline -- from ancient tablets to digital wallets -- with major events that shaped the direction of the modern credit card.

5,000 years ago: The ancient credit tablet

The concept of "buy now, pay later" isn't unique to the last hundred years or so: Credit was the way of the world in ancient times. Mesopotamia may have had the first system of virtual money 5,000 years ago, long before currency as we know it today existed. Cuneiform, an early script, was used to record transactions onto clay tablets as a form of counting and record keeping. Debts could even be literally wiped clean, on occasion, to protect debtors.

Late 1800s: Credit coins

Credit coins were issued soon after the Civil War. The metal coins were provided by merchants such as department stores and taxi companies as a form of payment. The coins could be stamped with an image and an account number that would identify the consumer. When the purchaser used the coin for payment, the merchant would look up the paper file linked to the account number to review the credit limit and authorize it.

1914: Western Union Metal Money

Western Union got started by offering customers reliable money transfers between New York, Boston and Chicago. The company expanded nationwide within a year, followed by international money transfers. In 1914, Western Union introduced metal cards nicknamed "metal money," an early version of a consumer credit card that let people defer paying for Western Union services.

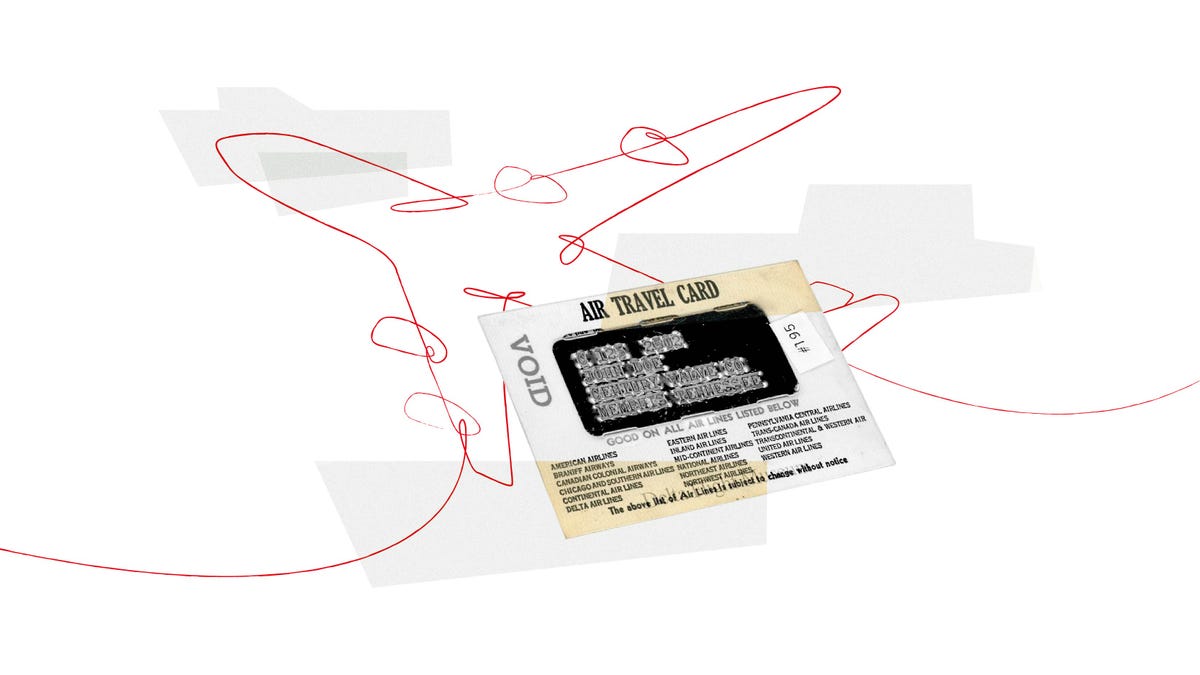

1936: American Airlines Air Travel Card

American Airlines issued customers the Air Travel card with a charge plate as a way to pay for air travel. It could also be considered the first travel rewards credit card: It offered customers who used it to purchase plane tickets at a 15% discount. American Airlines would continue to evolve its travel card and shows up again later in the timeline.

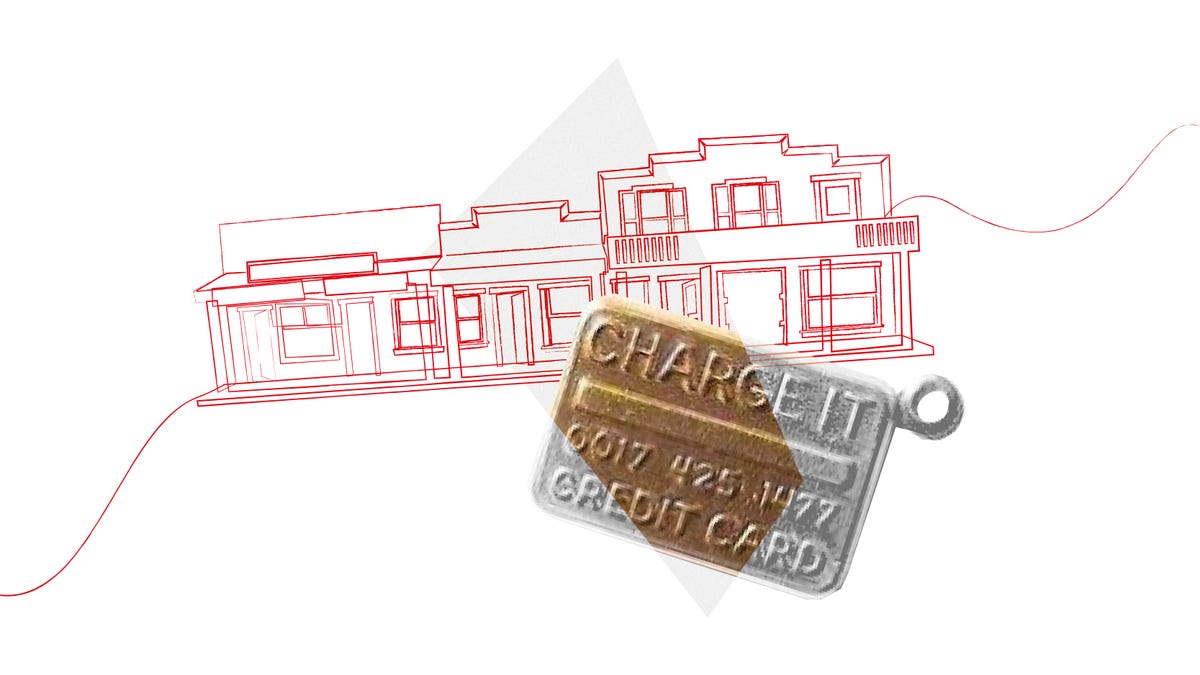

1946: Charg-It

A banker named John C. Biggins of Flatbush National Bank in Brooklyn, New York, introduced Charg-It, which may be the earliest bank-issued credit card. However, the concept wasn't convenient yet -- the bank only worked with local stores within a two-block area. Merchants would need to drop off the original sales slips at the bank so it could collect the debt.

1950: Diners Club

Diners Club is officially hailed as the first universal credit card, as at this point the virtual-money concept finally took hold. This card was originally to pay for meals in restaurants and then extended its reach to other services. By 1951 there were 42,000 Diners Club members. It was the first internationally accepted charge card by 1953, accepted in Canada, Mexico, Cuba and the UK.

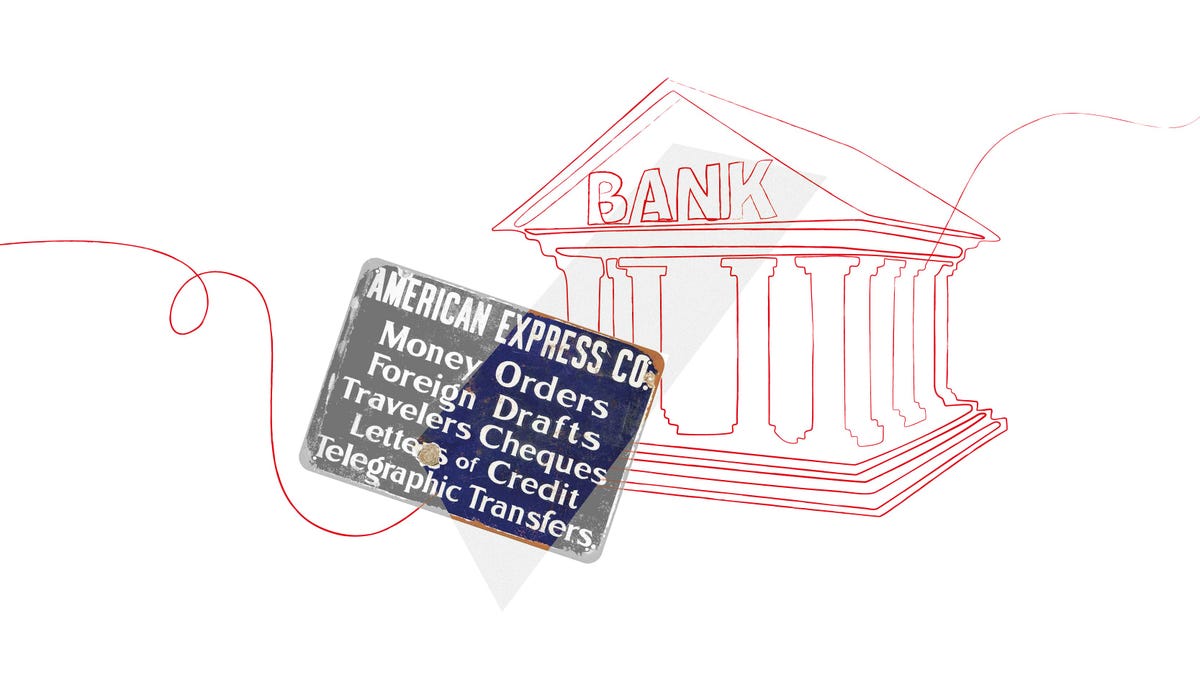

1958: American Express

The Diners Club credit card was prestigious but made of cardboard. American Express launched its first charge card in 1958, made of durable plastic. It was released to both the US and Canada. In 1966, they started marketing separate charge cards to businesses.

1958: BankAmericard

The BankAmericard is called "the first general purpose credit card." In the fall of 1958, Bank of America mailed 60,000 of its new cards to residents of Fresno, California, with a $500 line of credit. Within a year, the bank had sent more than a million cards to Californians, which helped drive the card's adoption and spur regulations about whom a bank could and couldn't send credit cards to.

1969: American Airlines Air Travel Card

American Airlines' Air Travel Card hit another major milestone in 1969 when it became the first card with a magnetic strip, changing credit cards forever by making them faster to process and more convenient to carry. The magnetic strip, now a staple in credit cards, was invented by IBM engineer Forrest Parry in the 1960s as a way for CIA staff to embed and transmit their identifying information easily. The first magstripe card was primitive — it was a credit-card-size piece of cardboard with a magnetic stripe affixed with clear tape. American Airlines was the first to embrace the invention.

1970: The Fair Credit Reporting Act is established

The Fair Credit Reporting Act was passed in 1970 to give consumers rights on what actions they could take regarding their credit reports. With this legislation, if a card issuer declined your application, you could request an explanation of why, as well as view your credit report for free. You could also opt out of unsolicited credit card offers. A provision was added to the FCRA in 2018 allowing consumers to freeze their credit to prevent others from opening accounts in their name without permission.

1974: The Equal Credit Opportunity Act becomes law

Although cards were becoming widely available in the 1950s, women and minorities were often excluded from getting a credit card. The Equal Credit Opportunity Act was passed in 1974 and prohibits creditors from discriminating against someone due to race, marital status and sex. Shortly after in 1977, the Fair Debt Collection Practices Act was passed to prevent abusive collection practices for delinquent credit card bills. The federal law prevents debt collectors from harassing you and calling you outside of the 8 a.m. to 9 p.m. window.

2004: Contactless credit cards are first used

The first contactless credit cards in the US were used in 2004. This method for payment became more popular in 2008 and beyond as Visa, Mastercard and American Express all started offering their own contactless cards.

2009: Credit CARD Act limits cardholder fees and interest charges

The Credit Card Accountability, Responsibility and Disclosure Act of 2009 saves consumers billions of dollars in "gotcha" fees. The law pushes credit card companies to be more transparent about how much a credit card really costs consumers. The act also places limits on fees and interest charges.

2010: Chip credit cards come to the US

Although magnetic credit cards were a game changer, they posed security issues: The information stored in the magnetic stripe could be copied and signatures (used as a form of identity verification) could be forged. Chip technology offered additional layers of security, making fraudulent charges harder to pull off. Most credit cards in the US are now issued with EMV chips. When paired with a PIN instead of a signature, the likelihood of fraud is further reduced.

2011: Mobile wallets

The problem with a credit card is that even if it has a chip and requires a PIN, if someone else has the card, they could find a way to use it. Looking to make purchases more secure and convenient, Google introduced the first mobile wallet that stored your credit card information in 2011. Apple followed a year later. With a mobile wallet, you can use your smartphone to pay, eliminating the chances of a lost or stolen credit card. Sure, your smartphone could go missing too. But the security built into using phones -- such as passcodes, fingerprint recognition or facial recognition -- are designed to make it hard for someone to use your virtual credit card.

Looking ahead to the future of credit card technology

As the timeline shows, credit cards are ever-evolving. At some point, it's possible that credit cards will no longer exist in the physical form we're familiar with. Instead, the "credit card" could become an extension of some piece of technology we use. Four possible futures for credit cards include:

1. Payments from anywhere

According to Jodie Kelley, CEO of the Electronic Transactions Association, the mobile payments we make now from our phones and watches are just the start and we'll increasingly use voice command tools, such as Alexa, to make payments everywhere from retail stores to gas stations.

2. Buy now/pay later

The growing trend to buy now/pay later, sometimes shortened to BNPL, allows you to break up a purchase over a number of payment installments and often doesn't require a hard credit pull.

3. Biometrics

Magnetic-strip signature cards may become obsolete as signatures are a less secure form of identity verification. Jeff Sakasegawa, a trust and safety architect at fraud-prevention company Sift, thinks the changeover could happen soon: "By the beginning of 2024, Mastercard will start to phase out physical cards with magnetic strips and shift to biometric cards, combining fingerprints and chip technology to increase their security."

4. QR codes

QR codes, or quick response codes, have become popular since the pandemic started and are used for everything from viewing a restaurant's menu to paying for goods or services with the quick scan of a square image reminiscent of a barcode. When linked to a mobile wallet, QR codes make payments fast and secure.

"QR code payments will boom globally in the next few years," Sakasegawa predicted. "As e-commerce continues to boom, consumers will become accustomed to this method and will start to expect merchants to offer similar QR Code experiences in order to reduce additional friction in the buying experience."