Intuit's chief on economy: Welcome to the 'new normal'

Intuit CEO Brad Smith's recent comments show the software maker has a killer instinct and has what it needs to make it through the recession.

This was originally posted at ZDNet's Between the Lines.

Intuit delivered second-quarter results that illustrate that it is recession-resistant, but a lot of the game plan revolves around cost cutting and innovating in a downturn. The rub: Intuit CEO Brad Smith doesn't consider the economic landscape a downturn per se, but a "new normal."

On the company's earnings conference call (statement), Smith said:

Now clearly we have seen some fundamental changes in the economy in the recent months. These changes have only bolstered my confidence that we are on the right path. We don't view this as a short-term downturn. In fact, we think of it as a new normal. A new normal that plays well to who we are and what we deliver as a company.

Smith outlined the five parts of its grand plan: play offense and focus on customers; cut spending; commit to growth; innovate; and acquire companies that make sense.

What Smith was really getting at is Intuit's killer instinct. The tech sector is becoming a fascinating study in the survival of the fittest. Many companies are taking aim at each other for market share and the financial spoils. You're beginning to see examples every day: Citrix and Red Hat joining forces with Microsoft to hit VMware hard is a prime example; HP cutting pay instead of employees so it can give Dell and IBM fits; Intuit offering Coghead customers an out to add to its Quickbase roster of clients. (Coghead, which went out of business, was scooped up by SAP).

Intuit is clearly now in the recession-resistant club and it's likely to take on established rivals like H&R Block and thwart upcomers like Mint by offering a nice exit strategy. In other words, Intuit has what it takes to simply buy its threats. And it will because it has a decent mix of established products it can milk for cash, new growth services, and discipline to cut expenses to keep Wall Street happy.

Here's a look at those moving parts:

Established products: TurboTax and QuickBooks can fund new businesses for Intuit. The company reported earnings per share of 26 cents a share on revenue of $791 million, down 5 percent from a year ago. Revenue would have been up 2 percent if revenue weren't shifted for Intuit's tax products. Excluding charges, Intuit would have had earnings of 34 cents a share, 7 cents better than Wall Street estimates.

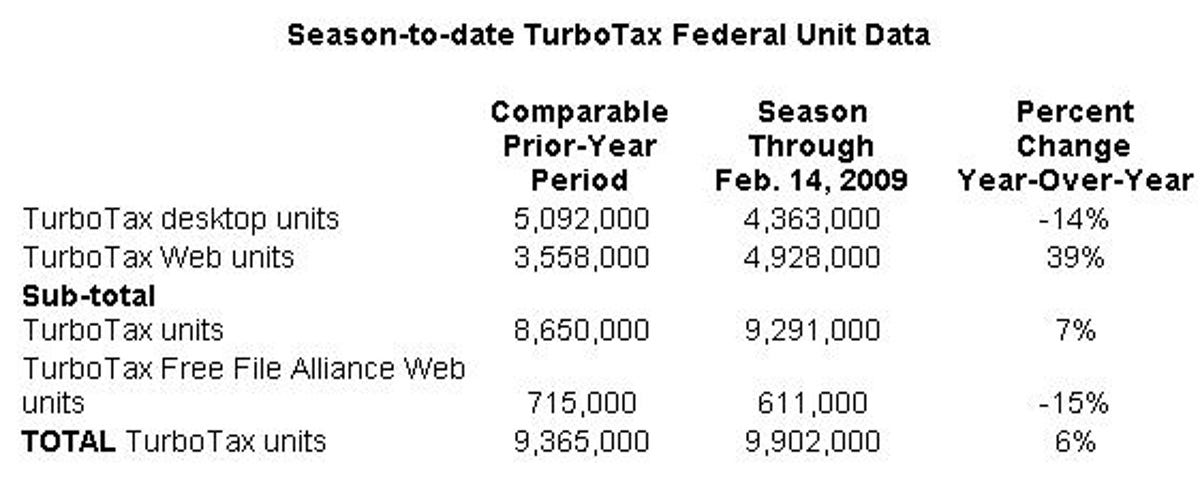

As is customary with Intuit, TurboTax pays the bills in the fiscal second and third quarters. Here's where Intuit stands with TurboTax as it shifts the product from the desktop to the Web.

QuickBooks, however, is under economic pressure. Smith said:

However, as I mentioned last quarter, some of our businesses are more exposed to the economic downturn. These businesses include QuickBooks, Real Estate Solutions, and Quicken. Each of them has come under increasing pressure as the economic environment has deteriorated. As a result we have reduced our full year revenue expectations for these businesses and adjusted the outlook for the company as a whole to reflect these changes.

Add it up and Intuit still has a solid stable of products that generate a lot of cash.

Growth services: Intuit has been adding extensions off of its QuickBook juggernaut, and some of these businesses are showing solid growth in a downturn. Intuit's payroll and payments revenue in the second quarter was $158 million, up 14 percent from a year ago. Professional accounting software revenue was $133 million, up 14 percent. Meanwhile, SaaS efforts such as Intuit's Quickbase tools aren't material to report, but will benefit from growing from a small base.

Financial heft: Sure, Intuit cut its outlook. For the third quarter, Intuit projected revenue of $1.38 billion to $1.46 billion, up 5 percent to 11 percent. Operating income will be $723 million to $778 million, up 7 percent to 15 percent. That tally equates to $1.38 to $1.49 a share for the third quarter. Excluding charges and other items, Intuit's third-quarter earnings are expected to be $1.57 to $1.68 a share. Wall Street was expecting earnings of $1.67 a share excluding items.

For fiscal 2009, Intuit projected revenue of $3.13 billion to $3.25 billion, up 2 percent to 6 percent. Intuit had projected growth of 6 percent to 10 percent. Operating income excluding items will be $917 million to $970 million, or $1.78 a share to $1.89 a share. Wall Street was looking for 2009 earnings of $1.79 a share.

Amid the weaker-than-expected outlook, Intuit said it is slowing hiring, evaluating compensation programs, monitoring marketing costs and cutting spending and "taking a hard look at what is truly necessary," said Intuit CFO R. Neil Williams.

Intuit seems to be navigating the downturn--or the new normal--well. Intuit ended the second quarter with $802 million in cash and investments and expects to generate $900 million in operating cash in fiscal 2009. Add it up and Intuit has more than enough to play offense and defense as needed.