How to deduct your home office without an audit

CNET@Work: If you run a home-based business, you may be eligible to expense the use of home office space and reduce your tax burden. However, you have to be careful.

With technology increasingly intertwined with all aspects of business, CNET@Work can help you -- from prosumers to small businesses with fewer than five employees -- get started.

One of the benefits of running your own small, home-based business is the possibility of paying less tax by expensing the use of your office space. This is an area that is greatly scrutinized, however, and a good working knowledge of the rules is necessary in order to be in compliance, and minimize the possibility of the dreaded Internal Revenue Service (IRS) audit, the mere thought of which strikes fear in the hearts of many US taxpayers.

It's always a good idea to consult your tax advisor or preparer regarding your specific situation.

Read next: Small business taxes: A primer

The good news is that if you make use of space in your home for business purposes, you may be able to take advantage of what is known as the home office deduction on your tax return. When used properly this is an expense that not only reduces income for federal and state tax purposes, but may also reduce self-employment taxes (social security and Medicare taxes that are effectively doubled for the self-employed) as well.

You have to be careful, however, in order to make sure that you're legally able to utilize the home office deduction, and to that end, the IRS has some fairly stringent rules to follow that may help avoid being questioned on the deduction, or worse yet, audited.

The IRS lists two basic requirements in order to qualify for the deduction:

1. The space must have "regular and exclusive use." In other words, you must use the designated area in your home only for "conducting business". That extra room in your house, be it a former bedroom or den, may qualify.

2. The space must be your "principal place of business." You can conduct business outside the home and still qualify for the deduction, as long as you're still using the space at home "exclusively and regularly" for business.

(Two exemptions apply to the "regular and exclusive use" rule: One if the office is used to store inventory or samples used in your business, the other if you are a day care provider for children, the elderly or the handicapped.)

See also: Best free tax software for your 2017 IRS return

Here's what all of this means: If your current bedroom is doubling as your office for your home-based business, you cannot take the home office deduction. Ditto for the family room where you may run your business, but it's also where the family gathers to watch TV. It's the same if you conduct your business from your kitchen table -- you cannot legitimately take a deduction for the space.

If your current bedroom is doubling as your office for your home-based business, you cannot take the home office deduction.

That spare bedroom that's no longer in use since your kids moved out may qualify. Same for the part of your basement that you walled off, where you simply added a desk, chair and PC from which you run your budding business empire. The garage that was just gathering junk over the years that you turned into an office would also qualify, just as long as the space is used solely for your business. In this case having it walled off as designated may help.

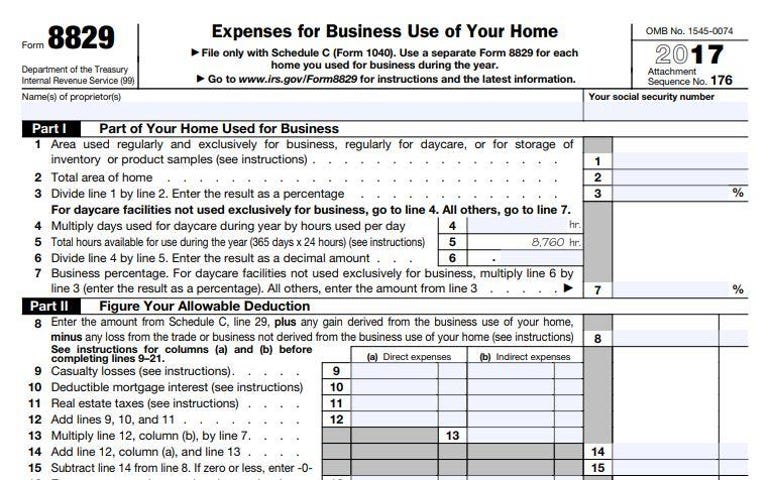

There are two methods you can use in order to determine the amount of your deduction: The Simplified Method or the Regular Method. These two methods are incredibly different in terms of what is required, and the potential longer-term implications.

What you can deduct: The Regular Method

Under the Regular Method, you first calculate the percentage of the home that is used for qualified business purposes. For instance, if your office is 15 by 20 feet, for a total of 300 square feet, and your home is 2,000 square feet, then 15 percent of your home is used for business.

From there, your deduction would include the following:

- A depreciation deduction: If you use the regular method, you would effectively be depreciating the value of your home, and taking a deduction based on the percentage of use multiplied by the amount of depreciation. (More on this later.)

- Actual direct expenses related to the office, such as repairs.

- A percentage of the indirect expenses, such as real estate taxes, mortgage interest, insurance and utilities that apply to the entire home. These are calculated, again, by multiplying the percentage of business use by the indirect expenses. The nonbusiness portions of real estate taxes and mortgage interest that remain would be handled as they normally are, as itemized deductions on Schedule A.

- Total deduction is limited to business use of home minus business expenses.

- Expenses are taken on IRS Form 8829.

Detailed record keeping is absolutely essential in utilizing the Regular Method; in the event of an audit you will need to be armed with backup information for all of your deductions. That means keeping utility bills, repair bills and anything else that you deduct. Keep all of this in an expense file designated by year, and get in the habit of adding to it as expenses occur.

Downsides of the Regular Method

Beside the more complex calculations and record-keeping burdens associated with the Regular Method, there's an additional issue that taxpayers need to be aware of. When you sell your home, you must "recapture" the depreciation that you deducted from the use of your home office over the years. This essentially means that you will have to pay ordinary income tax on the depreciation you expensed, and that amount is not eligible to be shielded by the $250,000 single or $500,000 married capital gains exclusion that many homeowners may be eligible for upon the sale of the primary home.

The benefits of the depreciation deduction over many years (the "bird in the hand" affect) may outweigh the potential cost of depreciation recapture sometime in the future, but each situation is different.

The Simplified Option

As the name implies, the Simplified Option requires little to calculate, and reduces the information and record-keeping burden. Keep in mind, however, that it does not simplify the standards needed to qualify for the deduction.

Under this option, the taxpayer can:

- Deduct up to $5 per square foot of the space utilized for the business, with a maximum of 300 square feet, or maximum $1,500 deduction.

- No other deductions are taken, whether direct (such as repairs), or indirect (such as utilities, mortgage interest, real estate taxes or homeowner's insurance).

- No depreciation is recorded, and thus there is no tax depreciation recapture once the property is sold.

Which method should I use?

This is a rather complex question which should be posed to your tax advisor. Business owners often gravitate toward the method that will garner the larger tax deduction. Still, calculating the deduction both ways is a worthy exercise.

For those with rather small offices relative to the size of their home, the Simplified Method may offer a better deduction, and will greatly reduce both the record-keeping and tax filing burdens.

What if I have a home office and work for someone else?

The rules are different if you have a home office, but use it in working for someone else. (These rules will be heavily impacted by the newly enacted tax laws for 2018 and beyond.)

Thorough record keeping is a must, especially in case the IRS audits you.

For 2017, you must still meet the "exclusive" and "regular use" requirements previously listed, but in addition, your use of a home office must be for the "employer's convenience":

- The employer does not provide a place for you to work outside the home office, requiring you to work from home as a condition of employment.

- The home office is necessary in order for you to perform your duties as an employee.

Unlike the deduction for business owners, however, if you work for someone else, associated expenses are taken as a miscellaneous deduction on Schedule A (Itemized Deductions). Miscellaneous deductions are limited in that you get no credit unless they exceed 2 percent of your adjusted gross income. While still a legitimate deduction in 2017, the new tax law removes miscellaneous deductions from the tax return.

The bottom line

While the home office deduction, especially for the self-employed, can be of benefit to those who qualify, a great deal of scrutiny must accompany its use. The IRS rules must be adhered to, and thorough record keeping is a must, especially in the case that you are audited.

As always, consult your tax advisor for specific advice that pertains to your situation.

Read more:

3 ways the GOP tax bill will impact business and tech (TechRepublic)

Bitcoin: A cheat sheet for professionals (TechRepublic)

IBM reveals 5 methods hackers use to steal your tax info and 6 ways to protect yourself (TechRepublic)