Handicapping cloud computing: The big picture

ZDNet's Larry Dignan outlines the landscape for cloud computing, including how big the stakes really are, and how well Google and Amazon.com will fare.

Cloud computing isn't going to dominate the tech landscape but will raise a ruckus for software vendors. Google and Amazon will be cloud-computing winners, but the spoils will be relatively small. And there's a race to deliver a cloud developer stack for both consumers and enterprise customers.

Those are some of the key takeaways from a Bernstein Report dubbed The Long View: Netbooks, Wireless and Cloud Computing--Client Software's Imperfect Storm.

The report, which I mentioned in my Microsoft analysis Thursday, is notable because it maps out the cloud landscape and puts Amazon in its place. Bernstein analyst Jeffrey Lindsay notes that Amazon's much-ballyhooed cloud-computing efforts--S3, EC2 et al--are more about the "gee-whiz factor," and portraying the company as something more than an e-tailer, than really delivering revenue.

"Although Amazon was arguably a pioneer of cloud Web services, and some analysts got swept up in the 'Books to Bits' hype, we think the revenues generated by Amazon's Web services are effectively negligible," Lindsay writes in a research note.

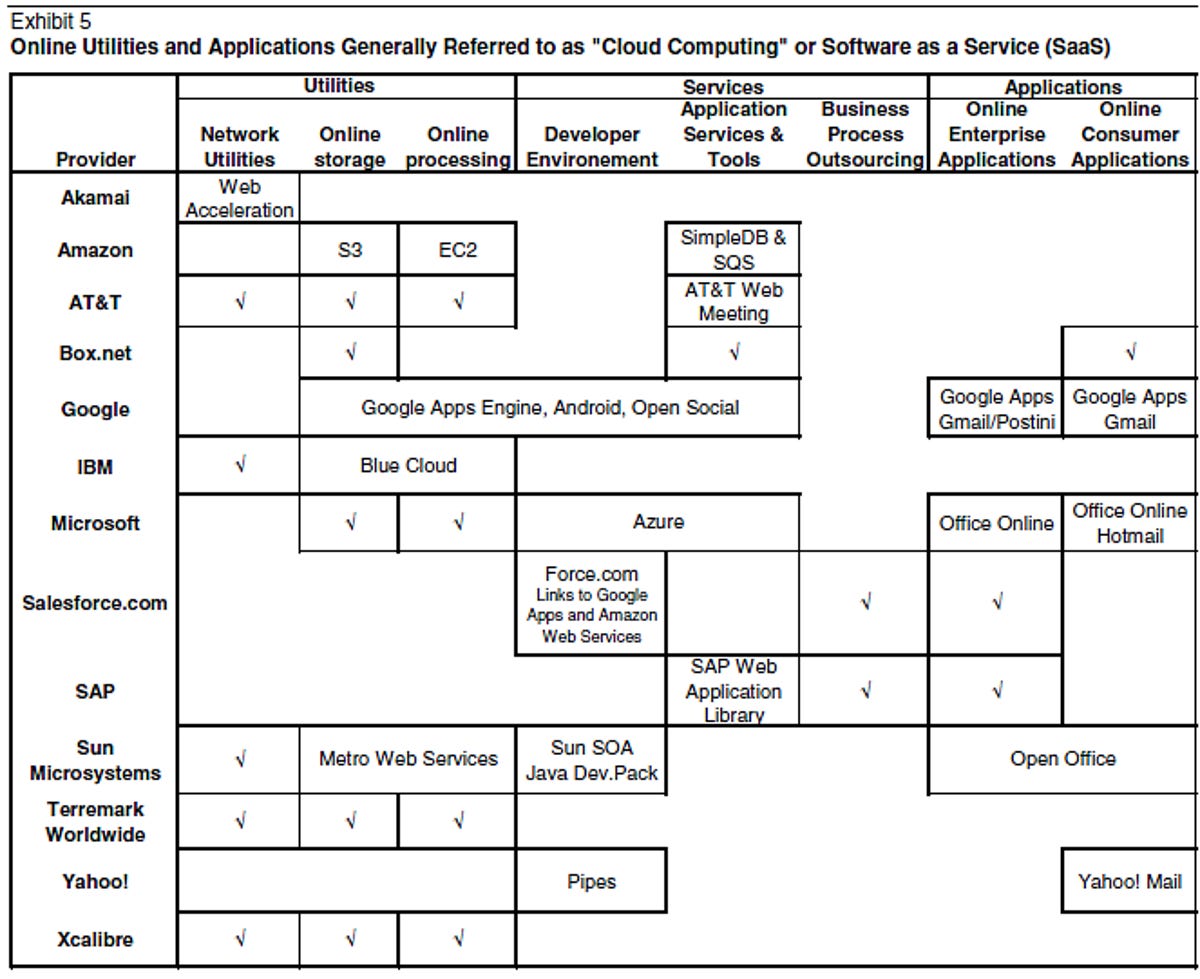

But before we get into that discussion, let's outline the landscape. Lindsay has cooked up this helpful chart that lines up the cloud stack that various vendors are trying to build. While Lindsay forgot a few vendors, the chart provides a handy overview:

What's notable is how much Sun Microsystems has been a player in cloud infrastructure yet has failed to capitalize. Besides Lindsay's chart, the report doesn't mention Sun again. Much of the focus is on Amazon, Google, and Microsoft. Bottom line: Microsoft will take a hit from cloud computing and software as a service, but not as much as folks think.

Among the takeaways from the report:

Sure, SaaS is taking share in human resources and customer relationship management software, but only 10 percent of companies manage their documents online. Most prefer Word and Excel, Lindsay notes. Will that change? A bit. Lindsay expects Microsoft's Office to remain dominant. The reasons Office will stay entrenched are interesting. Lindsay writes:

While Google Apps and Open Office from Sun have almost all of the functionality of Microsoft's Office, the conversion of documents is still not 100 percent effective, although Open Office comes very close indeed.

In a recent test, Open Office could easily open a Word version of one of our published notes with formatting that was over 98 percent accurate. Open Office could similarly open one of our financial models written in Excel--over 3Mb, and using a variety of Microsoft functions with iterative calculation.

Once again, the document opened almost perfectly, but a minor change was needed to ensure that the model converged properly. Google Docs did less well and could not handle the Excel model, but opened our Word note and preserved about 90 percent of the formatting.

Even though these programs are very nearly comparable in functionality and can offer additional functionality, in terms of allowing users to simultaneously edit documents--which the client versions of Word and Excel cannot do--we still perceive considerable reluctance on the part of users and IT departments to use them.

Our own IT department cited several compliance and security issues mitigating against the use of Open Office and Google Apps--some of them inaccurate--even though termination of our corporate contract with Microsoft would save a considerable sum of money.

The hangup: Companies don't want to rebuild templates, convert existing spreadsheets, and question future support for open-source document formats.

Cloud computing isn't everything. Lindsay writes:

We expect the software and applications environment to remain heterogeneous for the foreseeable future--more in line with Microsoft's vision than Google's. We disagree with the "computers as a utility" and "device as dumb terminal" models, where all applications run in the cloud, largely on the grounds that even today's best networks are 100 percent available and reliable, and that devices still perform vastly better when they have at least some of their own processing power--taking some of the load off the online processing and connection, and allowing processing to continue when the devices themselves are not connected."

Google Apps: Interesting but not a huge business. Lindsay notes:

Early assessments of Google's revenue potential from cloud computing were, we believe, greatly exaggerated. Some even speculated that Google's cloud-computing revenues could overtake its paid-search advertising business. While we think that Google's efforts in the cloud space, and initiatives such as Google Apps will appeal to consumers and small enterprises, we do not expect that they will displace more than 10 percent of Microsoft's Office software franchise, at best.

Even apportioning a degree of incremental Google search revenue to the increased Web traffic arising from use of Google Apps, we do not expect Google Apps revenues to exceed $1.5 billion by 2012.

What's the problem? Focus. Lindsay gives Google Apps props for the Postini purchase, and landing government and educational accounts. But "there are already signs that its product development team seems to be committing their familiar mistake of failing to improve its products sufficiently to fend off its competitors. Google lost its first trophy account, General Electric, with 400,000 seats, to start-up ZoHo in September."

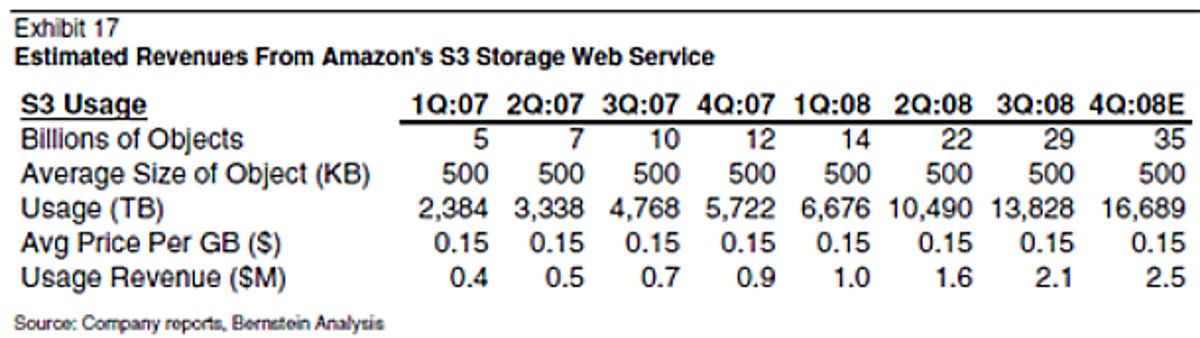

And finally, Amazon Web Services has a big opportunity, but is really chump change through 2012. Lindsay writes:

Although S3 is one of approximately 20 identifiable services, including infrastructure services (e.g. Elastic Compute Cloud, or EC2, SimpleDB, Cloudfront, and Simple Queue Service); payment and billing services (Amazon Flexible Payments Service and Amazon DevPay); on-demand workforce services (e.g., Mechanical Turk); and Web Search (e.g. Alexa Web Search and Information Services), we doubt they will, as currently configured, (they) generate even $50 million per year by 2012. This compares with Amazon's retail revenues for 2008, which are expected to be $19 billion and expected to reach approximately $30 billion by 2012.

Here is a look at Lindsay's guesstimates for S3 revenue, which is lumped into the "other" category, which includes Web services, Kindle, and other stuff, on Amazon's earnings statement.

Instead of a hard return, Lindsay surmises that Amazon is following the Web services path for more soft benefits.

In summary, we think Amazon's Web Services are not a major growth or revenue generator for the company. Instead, they provide benefits such as PR positioning of Amazon as a "technology" company rather than simply (as) an online retailer. They also provide interesting projects for Amazon's developers, who otherwise would be primarily confined to developing the shopping platform. This, we think, enables Amazon to attract a higher caliber of engineers and developers than (can) its competitors, such as eBay.

That final point is very interesting--especially for someone like me, who is firmly entrenched on the Amazon Web Services bandwagon. Makes you go "hmmm," as you ponder Amazon's motives with its Web services foray.