The 5-Step Process to Build Your First Personal Budget

With rising inflation, understanding where your money is going is more important than ever.

I built my first budget as a first-year college student. At 19 years old, I was responsible for more expenses than ever before, and I needed a better way to track my money. While I knew that writing down my expenses and checking my accounts would be helpful, I hated the process -- it felt tedious and made me anxious.

Through months of trial and error, I developed a system that works for me. Rather than a chore, I eventually began to see my budget as a useful road map to navigate my money. And the best part? It was helping me save. I'd managed to bank enough to help pay for an international spring break trip. I've even become the go-to friend for budgeting advice.

If you're just beginning to build your budget, the endless strategies you'll find online can feel overwhelming. But a budget doesn't have to be complicated or difficult. In my experience, simplicity is key.

Here are the five steps I took to build my first budget -- plus, access to my own spreadsheet for you to customize.

Get clear on your money goals and why you need a budget

Mastering your money isn't about being a math genius. It's more important to understand what you want your money to represent. In other words, what do you want to accomplish in the short and long term? That's the first step.

CNET Money Editor-at-Large Farnoosh Torabi advises: "Know your 'why' for spending and saving. Align it with your values. Money is meaningless without goals." Some examples of concrete goals may include getting out of debt, affording a vacation or building up to a big purchase. Once you know what you'd like to achieve, attach a specific dollar amount to it so you can design your budget.

You gotta see it to believe it (even if it's frightening)

Before I started maintaining a budget, logging into my online bank account was always a dreaded event. I never wanted to see how much I had spent and was deeply wary of seeing a negative balance. I wasn't alone with this fear. My friends also admitted that checking their accounts was nerve-wracking.

But like anything challenging, if you do it enough times, it eventually becomes less difficult. Reviewing my accounts and spending patterns consistently not only helped ease the pain, it reduced my financial anxiety. As it turns out, knowledge can be empowering. When I understood my spending behavior and had awareness around my cash flow, my finances were no longer a guessing game.

Organize and understand your spending habits

Getting comfortable with seeing my transactions online was helpful, but not without limits. A never-ending screen of deposits and withdrawals all clumped together was not easy to follow. I had a hard time grasping where to feasibly cut back or slow spending.

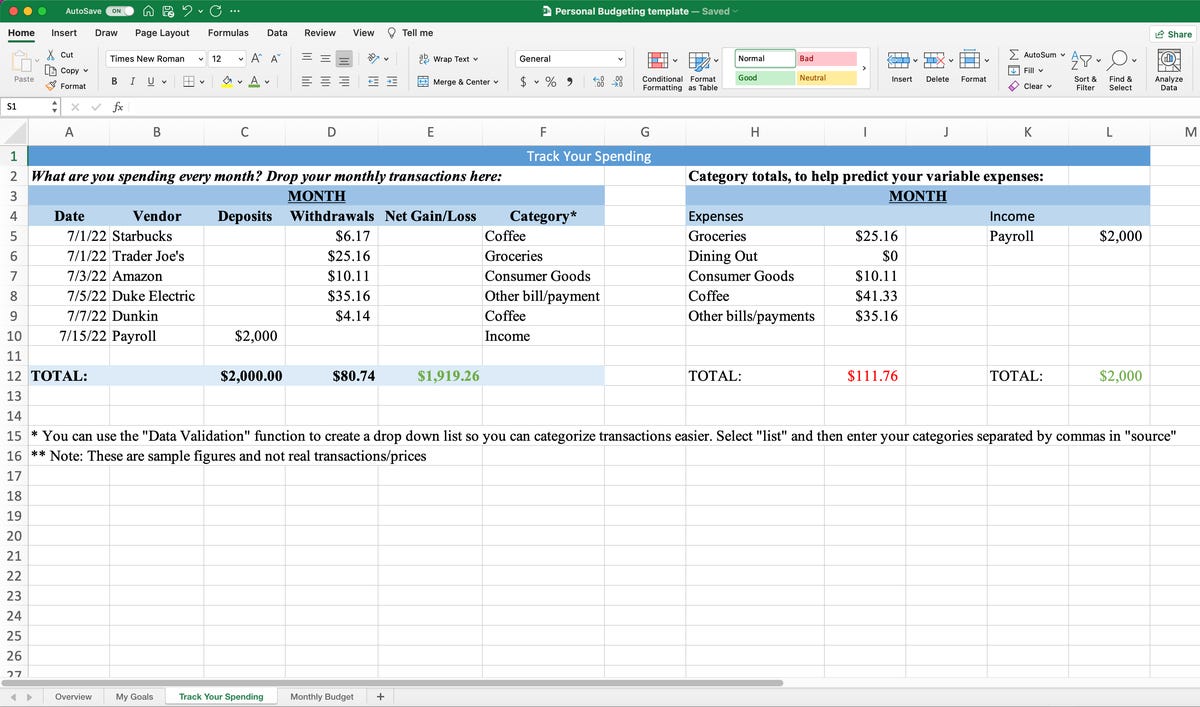

To make it simpler, I downloaded my bank data into an Excel spreadsheet. I eliminated some of the extra information I didn't need, such as transaction numbers and remaining balances, to focus on the essentials: the vendor name, the date, whether it was a deposit or withdrawal and the amount.

Then, I organized all my expenses into different categories -- fixed and variable -- so I could understand exactly where my money was going every month. This helped me locate the areas in my budget that I could feasibly control.

Building your budget

Now that you've defined clear goals for your money and have gotten comfortable with your accounts, you're ready to start mapping out a simple budget. For me, my budget was meant to set realistic spending expectations for the month and guide me to making smarter purchases.

There are thousands of different budget templates available online. To help you wade through them, CNET put together a list of the best budgeting apps if you would rather keep track on your phone. Some other best picks are these free budgeting templates from Mint, the Federal Trade Commission and NerdWallet. Microsoft Office and Google also have personalizable spreadsheet templates that would work.

Personally, I like using an Excel spreadsheet where I have three sheets: one that lists my financial goals I'm working toward, one where I track my spending and another where I build my actual budget of fixed and variable expenses. No matter what system or template you use, your actual budget should have these key elements. This is how I set up my own, which you can also access here.

I have my fixed monthly expenses in one column, including rent, utilities, insurance and subscriptions like streaming services. These are any expenses or fees you always have to pay and that typically don't change each month.

Next, using my past spending habits as a barometer, I set goals for my future spending in nonfixed or variable categories, including groceries, dining out and other bills. I also add personalized categories in other areas where I tend to spend relatively more money. For me, one of these is solely dedicated to coffee. Every month I allocate $50 for my (overpriced, but still essential) lattes. During midterm and finals seasons, I know this category of spending will skyrocket, so I'm able to plan for the increased coffee costs by cutting back in other areas.

Then, I leave a third column blank next to each expense category to fill in at the end of the month what I actually spent in reality. Leaving space for this "goal versus reality" comparison is helpful for seeing how well or poorly you stick to your budget.

To finish, I add a fourth column with my expected income for the next month. If you're an hourly or nonsalaried worker like me, your paychecks are probably harder to predict. Taking a few minutes to do the math on what you project to earn for the month can be helpful.

Use your budget proactively

Now you're ready to start using the budget, which may be tricky in the beginning. While my budget helped me understand my money, initially I had a difficult time using it to improve my savings. Knowing your money habits is different from changing them.

To help, I started each month by asking myself an essential question: Will I make more money than I plan to spend? We'd all like to think the answer to this question will be a resounding YES, but not every month will be a positive cash flow period because of any number of unplanned expenses. If you guess the answer is no, you can explore areas where you can make spending cuts ahead of time, instead of resorting to credit to pay for the overages. For me, being proactive was about understanding wants versus needs. By spending less on things that weren't must-haves, I could apply the net savings toward another financial goal of mine: an emergency account.

If you're also hoping to fund an emergency account (or any expense), and you know you'll be tempted to spend your net savings, commit to putting a fixed amount in a separate account such as a high-yield savings account, which has a greater rate of return. Putting aside your remaining money and pretending like it's not there could help better protect your savings.

More budget maintenance tips

- Aim to spend below your budget. I consider it a win if I spend 10% below my estimated budget.

- Make space to pay yourself. Torabi advocates allocating at least 10% of your income toward personal savings, which can help to cover an unexpected expense or splurge. Keep working on this savings strategy until you have enough to cover at least a few months of basic expenses.

- Be kind to yourself and your budget. Taking small steps now can go a long way in helping you achieve financial security and reach your goals.