Why You Can Trust CNET

Why You Can Trust CNET Advertiser Disclosure

How to Maximize Your Retirement Savings With a Roth IRA Conversion

Converting your traditional IRA into a Roth IRA isn't hard, but much of the decision depends on when you need the money.

A Roth IRA lets you pay taxes now to get bigger savings later.

If you've got a 401(k) account or individual retirement account (IRA), you've already got a good jump on planning for your golden years. Both plans let you make contributions tax-free, but you'll need to pay taxes on that money when you withdraw it later during retirement.

A Roth IRA, on the other hand, flips the equation by saving you taxes later when you withdraw money from your account. While traditional IRAs let you make tax-free contributions toward a retirement account, Roth IRAs instead eliminate the taxes on the distributions that you receive from the account once you are retired.

The good news is that you can convert money from traditional IRAs and 401(k) accounts into Roth IRAs whenever and as much as you'd like. A Roth IRA conversion can make sense if you can afford to pay the taxes and don't need the money anytime soon. And for those who don't qualify for yearly Roth IRA contributions, a Roth IRA conversion works like a "backdoor" Roth IRA.

Learn all of the important details about Roth IRA conversions to help you decide whether to consider transferring some of your retirement income into a Roth. For more on retirement, learn everything you need to know about early retirement and taking Social Security benefits once you do retire.

What is a Roth IRA, and how is it different from a traditional IRA?

Originally called an "IRA Plus," the Roth IRA was introduced with the Taxpayer Relief Act of 1997. It's named after William Roth, a senator from Delaware who sponsored the legislation.

In contrast to traditional IRAs, contributions to Roth IRAs are not tax deductible. Instead, investors can receive tax-free money from their accounts after they turn 59 and a half years old, with some restrictions. With a traditional IRA, all distributions of money -- including the initial contributions and investment income earned on them -- are taxed at the current rates when you receive them during retirement.

Roth IRAs are more flexible than traditional IRAs for withdrawals. Roth IRA owners can withdraw their original contributions at any time tax-free, and you can withdraw earnings from your investments tax-free if you are 59 and half years old and the account has been open for five years.

Another benefit of Roth IRAs is that they are not subject to required minimum distributions when you reach a certain age, as traditional IRAs are.

What are the restrictions on Roth IRA accounts?

Yearly contribution limits for both traditional and Roth IRAs are identical: $6,500 in 2023, or $7,500 if you are 50 or older (or $7,000 and $8,000, respectively for 2024). However, the amount of money you can contribute to a Roth IRA phases out with higher incomes.

The allowable amount of contributions to Roth IRAs starts to decrease at $138,000 of income for single tax filers and is eliminated completely at $146,000. For married taxpayers filing jointly, the contributions start phasing out at $218,000 and disappear at $228,000. Roth IRAs are essentially not available to married people filing taxes separately. If they lived together at all during the year, married people filing separately can only contribute to Roth IRAs if their incomes are less than $10,000.

While there are income limits for contributing to a Roth IRA, there are no such limits for converting a traditional IRA to a Roth IRA. That means that anyone at any income level can functionally contribute to Roth IRA by using an IRA conversion. That's why Roth IRA conversions are sometimes called "backdoor Roth IRAs."

Preparing and planning for retirement can involve reams of official documents with lots of fine print. Do yourself a favor and decrease your eye strain with this 3x lighted magnifying glass. The sturdy device is powered by three AAA batteries and also includes a 45x jewelers magnifying option.

How do I convert a traditional IRA to a Roth IRA?

There are a few practical methods of converting an IRA to a Roth IRA, but the basic premise is the same -- you transfer money from an existing IRA account to a new Roth IRA account. You'll then need to pay current income tax rates on the money you transfer, and you'll receive tax-free distributions upon retirement.

Converting an IRA to a Roth IRA is easier if both accounts are managed by the same financial institution, but it's not necessary. If a rollover requires mailing you a physical check, you'll need to deposit the check in your Roth IRA account within 60 days to avoid penalties.

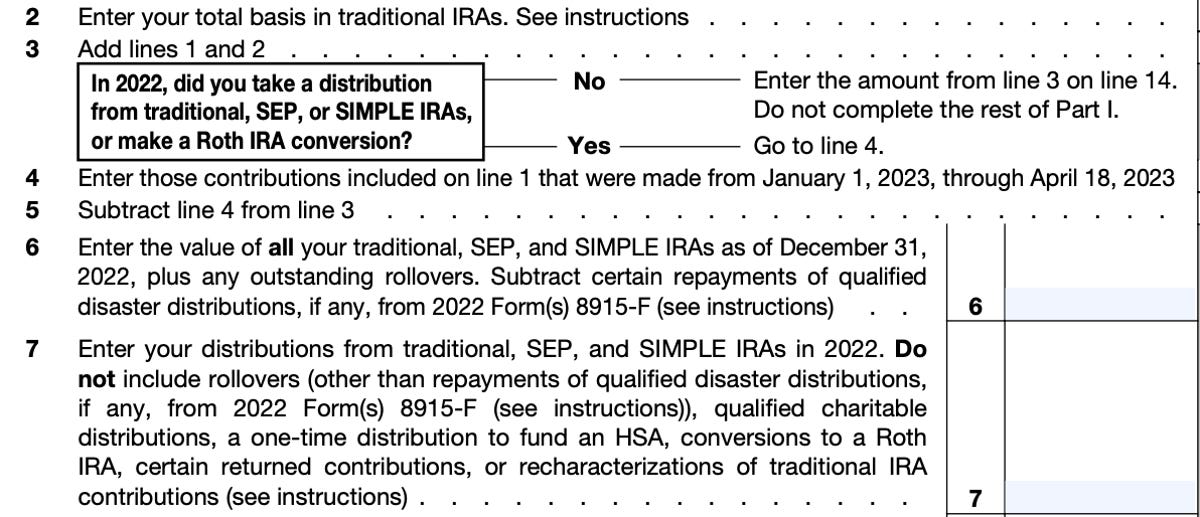

You'll enter the money rolled over into a Roth IRA on Line 4 of IRS Form 8606.

There's no limit to how much money you can transfer from a traditional IRA to a Roth IRA in one year, but remember that you'll be paying taxes on it come tax time. You may want to avoid rolling over your entire retirement fund all at once if it will bump you up to a higher tax bracket for one year.

At tax time, you'll receive a Form 5948 that shows the amount of money you rolled over into a Roth IRA, and you'll report that amount on your federal taxes using IRS Form 8606. There are currently no limits to the amount of money or number of times that you can convert retirement funds to Roth IRAs.

Important: As of 2018, you can no longer reverse Roth IRA conversions. The IRS formerly allowed "recharacterizations," or reversals, of Roth conversions up to Oct. 15 of the following year, but the Tax Cut and Jobs Act of 2017 discontinued the practice. Roth IRA conversions are now irrevocable, so be sure to consult with a tax pro before converting your IRA to a Roth IRA.

Who should convert a traditional IRA to a Roth IRA?

Everyone's tax situation is unique, but there are two main requirements for people converting traditional IRAs to Roth IRAs:

- You don't need to use your retirement funds for at least five years

- You can afford to pay the taxes on the amount of money you are converting

Yanelys Benham, wealth management adviser at TIAA, told CNET that tax diversification should be a major factor when considering a Roth IRA conversion.

"In most cases, people save on a pre-tax basis through their employer plan, which is an excellent way to start saving for retirement," she said. "However, if all your savings are pre-tax, then at retirement, they will be taxed as ordinary income which could be a tax ticking time bomb."

Benham also notes that the extra taxable income from traditional IRA distributions can potentially bump up your Medicare Plan B premium and the taxable amount of Social Security benefits.

Social Security benefits are taxed, and the tiers are 0%, 50% and 80%. "Single taxpayers with income over $34,000 and taxpayers filing jointly with income over $44,000 will have 85% of their Social Security benefits taxable," Benham told CNET.

Your distributions from traditional IRAs are treated like ordinary income, while your Roth IRA distributions are not. Converting your money from a traditional IRA to a Roth IRA could put you in a lower tax bracket during retirement, with included perks like the potentially lower Plan B premium.

Who shouldn't convert their IRA to a Roth IRA?

If you need your retirement money soon, it doesn't make much sense to convert your retirement savings into a Roth IRA. Most important, there is a five-year waiting period for funds converted into Roth IRAs, no matter your age. If you withdraw any money before the five-year threshold, you'll pay a 10% penalty.

Also, most of the tax advantages of Roth IRAs hinge on earning income over time, and paying taxes on your funds shortly before withdrawing them won't save you much money.

One other major factor when considering a Roth IRA conversion is whether you have the money to pay the taxes on your converted funds. You don't want to borrow money or dip into your IRA savings to pay the necessary income taxes. One popular strategy is to convert as much money into a Roth IRA as you can afford to pay taxes on that year.

Benham also stressed that converting your traditional IRA to a Roth IRA is not a good idea if you plan to give much of it away to charity using a qualified charitable distribution.

"People who plan to give a substantial amount to charity and/or leave their IRA to a charity should not consider converting to a Roth," she said. "At 70 and a half or older, you are eligible to make a qualified charitable distribution of up to $100,000 per year and not pay taxes on it."

The recipient must be a certified 501(c)(3) organization, and the IRA distributions must go directly to the charity from your financial institution.

A Roth IRA conversion calculator on the Bankrate site (CNET and Bankrate are both owned by Red Ventures) can help you figure out exactly how much money a Roth IRA could save you on taxes. Bentham also stresses that every investor should "consult with your accountant and financial advisor when deciding whether it makes sense for you to convert your IRA to a Roth."