Manilla vs. PageOnce: Building better bills

The paper bills you get in the mail? Holdovers from a bygone time. But they'll be with us for a while yet, judging by the current state of the art in online billing.

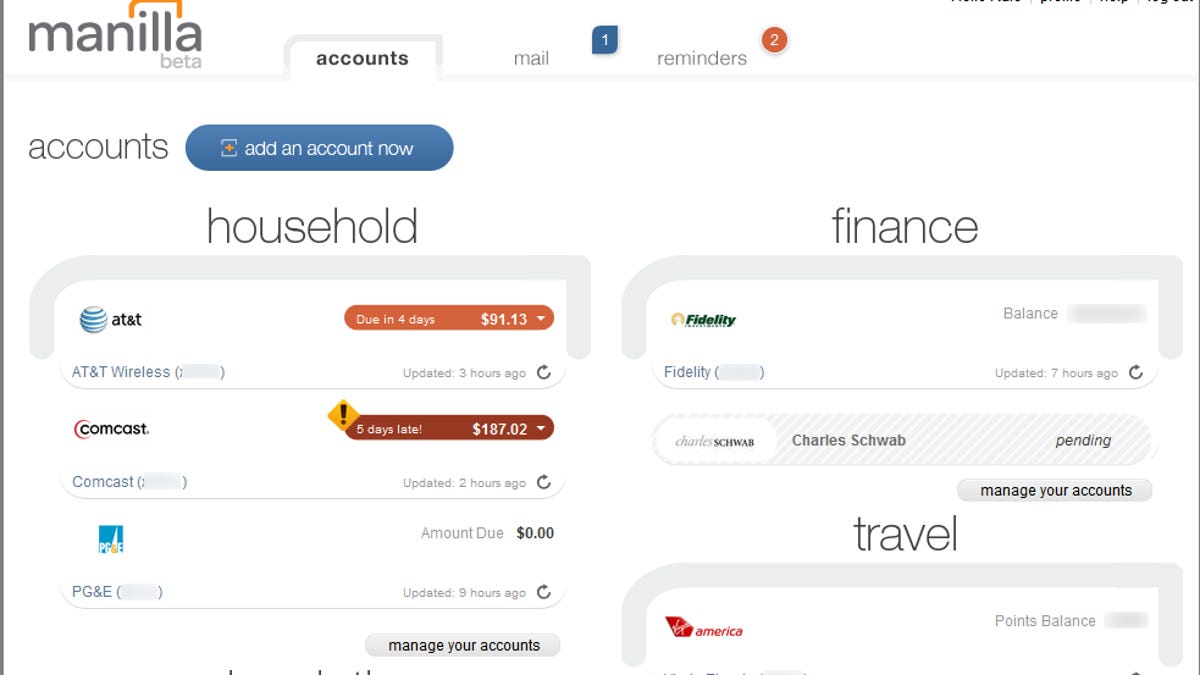

The bill organizing service Manilla launched at Demo this week. The pitch: it's a portal for your household bills. It will collect bills from your service providers, as well as bank statements and other financial data for you, and remind you what's due, to whom, and when. Furthermore, it'll keep records of all your bills and statements for you securely.

It should work with nearly any billing company, and in some special cases, you can use it to turn off your paper bills, doing your bit for the environment.

Using Manilla to receive and file electronic statements (called "bill presentment" in billing industry lingo) is far superior to asking your service providers to send your statements to e-mail, where they're highly likely to get ignored or accidentally spam-filtered (trust me on this). That's probably why only a small percentage of consumers allow their paper bills to be turned off. Having a single, dedicated, junk-free site for financial transactions makes more sense. That's what Manilla is.

It also makes some bottom-line sense for business. It costs about 73 cents to process and mail a paper bill, according to Manilla CEO George Kliavkoff, compared with nearly nothing for providing Web access to show the consumer an online statement.

On the other hand, businesses do get something for that 73 cents. They get to stuff your bill envelope with upsells, marketing materials, and pitches from partners. Manilla will offer an online version of that channel to businesses that decide to use it (like Comcast, at launch). For other billers, the service will just log in to users' accounts on their behalf, get their billing data, and present it to them on Manilla.

Those other, non-signed-up billers, which make up the enormously vast majority of businesses, in fact might find that Manilla is not such a fantastic deal for them. Customers who sign up for Manilla are likely already online-savvy users. They're already going to business Web sites to view, and maybe pay their bills. On those Web sites, business cannot only market to their customers (as they can via snail mail), but can also track what they're doing, offer surveys, and learn more about them. Once a middleman presentment service like Manilla is their online destination, the businesses lose that direct channel to the customer--until they get on board, like Comcast did, and start using the marketing channel.

So while the businesses of America figure out whether they should do a deal with Manilla, should you consider using it? Maybe, but you can probably do better.

Manilla is not a new pitch

Manilla is a compelling idea and will likely be a strong and highly usable product fairly soon; hopefully it'll be better when it comes out of its invite-only beta. If you're really interested in consolidating your bills into one online portal right now, I'd recommend using PageOnce, a two-and-a-half-year-old, but recently updated product that I found just as easy to set up, but more useful for tracking the really important data: what you owe now and whether you have enough money to cover it.

While Manilla acts a great repository for statements and bills--it's a really good electronic filing cabinet--PageOnce does a better job of parsing your current financial status. It can get details from bank statements and bills, where Manilla will only link you to your online account or show you an un-digested Web version of most of your statements.

PageOnce is almost Mint-like in its capability to dig into your finances and get useful data from them. It doesn't have all of Mint's historical or analytical chops, but it's still quite useful--and Mint doesn't do bill presentment at all.

Unfortunately, just like Manilla and Mint, PageOnce doesn't have a direct bill payment function. Yet. One is coming, though, and from what I know of it, it'll be unique and useful. Manilla does at least dump you onto the biller's site when you want to pay a bill.

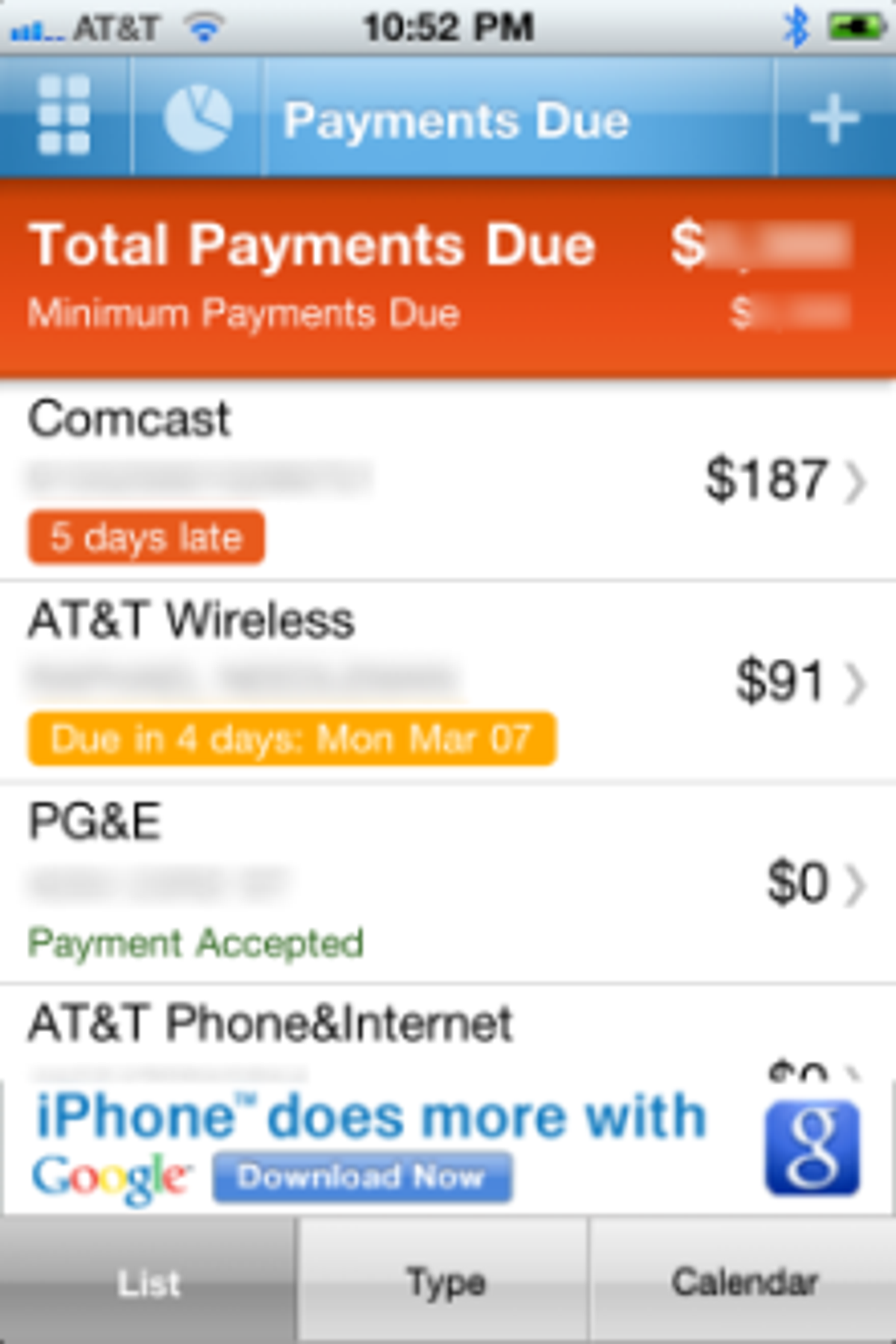

PageOnce has extremely good mobile apps, something Manilla hasn't yet shown. PageOnce makes it easy and clear to see what's happening in each of your accounts on a smartphone's small screen. There's even a calendar view that shows bill due dates. Manilla CEO Kliavkoff told me that when the company comes out of closed beta, it will also have a dedicated mobile product.

I do have to note that neither PageOnce nor Manilla are 100 percent accurate. In my tests, while most accounts I added worked perfectly, both services indicated that I had an overdue balance on my Comcast account. Genuinely concerned (I'm far too OCD to let this happen), I logged onto the Comcast Web site, only to find that my payment had been received earlier this week. Similarly, both threw an error when trying to access my Schwab account, although neither would say exactly what was wrong.

Other paper-replacement options

There are other emerging ways to get paperless bills, but they're not quite ready for real users. Doxo, in particular, has a Manilla-like focus on replacing your paper filing cabinet with an electronic one. Customers of businesses on the Doxo network get full access to their accounts as well as all the marketing materials the businesses want to send out--the same business benefit as Manilla. Doxo is also adding a centralized payment system. Doxo, like Manilla, is in invite-only beta test now, and has only three billers set up on its system: Sprint, Kansas City Power & Light, and Puget Sound Energy. For billers not on the network, Doxo does little more than provide their customers a place to store user IDs and passwords, and whatever documents they opt to scan in themselves, like Evernote with a focus on home documents.

Likewise, Zumbox is trying to replace paper bills with electronic ones. It makes it easy for billers to send bills to you without knowing either your Zumbox account ID or your e-mail. Zumbox instead creates accounts based on your postal addresses. The service seems to be fallow, as it has no way that I could see to request that billers send statements to your Zumbox "address." But it's still an intriguing idea.

If you want to get and actually pay your bills online on one service today, you can look to Intuit's Paytrust. The service costs $9.95 a month, though, which is too much to pay when you consider how much money you're saving billing companies by using it. Intuit's Aaron Patzer (the founder of Mint), told me that the company is working on new consumer bill management services, but he wouldn't give a time frame for a feature or product release.

It's still too early

PageOnce CEO Guy Goldstein told me that the annual American cashflow through consumer bills is $3.7 trillion. There's limited direct revenue to be made by just showing customers those bills. It is, though, not too hard to make a few pennies each time you facilitate an actual bill-pay transaction. With that amount of money in the balance, expect to see more companies try to get a piece of that big, fat, cash pie.

That's the future. If you want to use a service today to consolidate your bills, and you can live with less than perfect accuracy, PageOnce is your best bet.