Kiva humanizes microlending to third-world entrepreneurs

Nonprofit start-up of former PayPal executive helps people lend their pocket change to cash-strapped businesses in developing countries over the Internet.

Updated at 1:40 p.m. PST with additional comments from Shah.

For $25, you can get four collector's stamps, 25 moving boxes, or a Care Bear cuddle pillow on eBay.

Or you could help Lucía Chávez Rivera, a single mother of three, buy shoes and linens to sell at a market in Peru, and get your money back within the year.

Kiva, a peer-to-peer online microlending nonprofit organization, is changing the dynamics of microfinance by linking people who have money to loan up with entrepreneurs in developing countries who need some capital, all over the Internet. What is considered pocket change for many people in the United States can go a long way toward helping a struggling businessman get started in another part of the world.

The nonprofit is basically an "eBay for microfinance," Premal Shah, president of Kiva, said in a talk as part of the PARC Forum at PARC (formerly Xerox PARC) headquarters in Palo Alto, Calif., on Thursday night.

Since launching in 2005, Kiva has attracted more than $20 million in loans from more than 100,000 people. People choose whom they want to lend to. They can loan from $25 to $150 per entrepreneur, although recent demand to loan has forced the site to cap the loan amounts to allow more people to participate. The site gets money to grow from loan percentages donated to it by individual lenders.

Kiva raises more than $1 million over the Internet every 12 days, and most loans are typically repaid within a year, says Shah, formerly a principal product manager at PayPal, which is now owned by eBay. About 90 percent of the individual lenders take the repayment and fund other entrepreneurs with it.

And how do the funded businesses fare? The repayment rate is reportedly 99 percent, but Shah says he suspects that the actual figure may be closer to 90 percent.

Part of the success of Kiva is that it humanizes the lending experience, literally allowing lenders and borrowers to see the people with whom they are dealing. The site has profiles and photos of the entrepreneurs and lenders, as well as information on how much people have borrowed and repaid.

Because people can see exactly who is getting the loan and what it is being used for, the process works better than in traditional institutional-lending situations, Shah says. For example, despite the political turmoil in Kenya, the loans keep coming, he said.

"Someone in Des Moines, Iowa, really cares about Kenya now...(it) creates a persistent tie to somewhere around the world," Shah says.

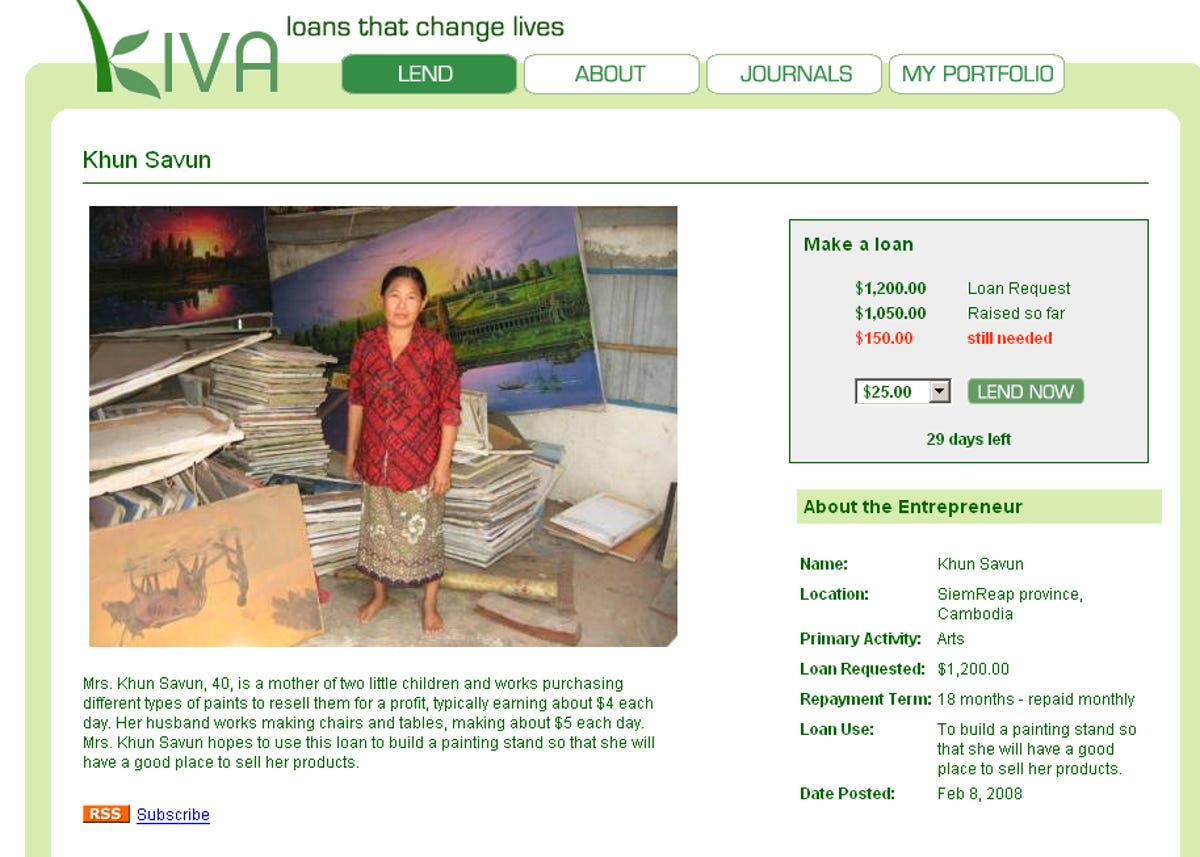

The stories are compelling. Khun Savun, a mother of two in Cambodia, is seeking $1,200 to build a stand where she can sell her paintings. She's raised $1,050 so far. Then there is Susan Lwanga, a pharmacy owner in Uganda who has repaid half of a $575 loan. She needed the money to buy "malaria drugs, painkillers, antibiotics, and mosquito nets for wholesale trading."

"People are more risk-tolerant than banks, when it comes to doing good," Shah says. "Iraq businesses get funded in just two hours on our site."

The loans are processed through nongovernmental microfinance groups in the region--"bankers on bicycles" as Shah called them--who deliver the money to the borrowers in the local currency and collect payment. They assume the risk when currency rates fluctuate, but they also charge an interest rate of 20 percent, on average. That compares with typical interest rates as high as 100 percent to 200 percent from traditional lenders in the developing world, according to Shah.

Shah shared some interesting statistics on lending. For instance, Kenyans are funded at nearly 11 times the rate of Bulgarians, for some unknown reason, and agriculture gets the most funding. Meanwhile, women get loans at more than twice the rate of men because they have a higher repayment rate, and they are more likely to spend the profit on food for the family, he said.

Eventually, Shah said he would like to see person-to-person financing without the microfinance middlemen, in which people could just transfer money over a cell phone to borrowers at minimal interest rates.

He also is hoping to one day enable more interaction between the lenders and the borrowers by, for instance, having Web chats or videos of entrepreneurs discussing their business.

In the meantime, Kiva is trying to stay on top of creating borrower profiles. The organization is launching a fellows program in which volunteers can visit borrowers around the world, and help research and write profiles about them for the Web site.

Shah got inspired by microfinance while getting an economics degree at Stanford University, where he received a grant to research the topic in India.

"It's an elegant and business-focused approach to fighting poverty in the developing world," he says. "The concept of getting a little bit of credit and someone taking a bet on you so you can pull yourself up by your bootstraps is very American."

For more on technologists turned philanthropists, read these stories on CNET News.com:

The end of philanthropy by Salesforce.com CEO Marc Benioff

Engineering change by CNET Editor Jessica Dolcourt