X1 Card

- Intro Offer

-

No current offer

- Annual fee

- None

- APR

- 15.50% – 27.75% Variable

- Recommended Credit A credit score is used to indicate an applicant’s credit worthiness and may provide guidance about account eligibility. It does not necessarily guarantee approval for any financial product.

-

670 – 850

Good – Excellent

- Rewards rate

-

2x – 10x 2X points on every purchase regardless of category; 3X points every time you spend $1,000 in a month; 4X, 5X and even 10X points for every friend who gets a card; Up to 10X points at leading online stores such as Apple, Nike and Sephora when you shop in the X1 App

The X1 Card is a unique new credit card that offers innovative features in security, rewards and credit-building features. On Thursday, the X1 Card ended its waitlist program and opened up applications to the public.

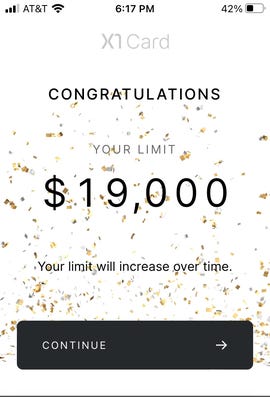

The application itself weighs your income more heavily than your credit score, giving those with high incomes and less-than-stellar credit a chance to get approved. The X1 Card claims to give up to “5x the average credit line” of other issuers, which can in turn help boost your credit score. I was not disappointed when I was granted an unexpectedly high credit limit.

This metal credit card runs strictly from a mobile app, where you can generate a number of different virtual online credit card types to keep your personal information safe when shopping online. There are a lot of ways to earn rewards boosts, and you can earn up to 4% back on all of your purchases if you strategize well. Put simply, the X1 Card is raising the bar for credit cards.

1. You can get approved even with a lower credit score

The X1 Card has the potential to help cardholders boost their credit score, in large part because approval is based more on income than on credit. While the application does require a credit pull, a hard credit check was only conducted after I was approved, though it did request my Social Security number to do a soft pull (which doesn’t affect your credit score) before approval. I was approved for the X1 primarily based on my income.

To verify your income, X1 asks you to log into your bank account where your paychecks are deposited via Plaid, a secure financial data connection service. If you have two-factor authentication turned on with your online bank account, you may have to temporarily disable that feature for Plaid to work, depending on the bank.

2. The X1 gives a large credit line

X1 told CNET in December that it grants credit lines up to five times as large as those offered by traditional issuers -- the average credit line granted to successful X1 applicants was $24,300. I was a bit skeptical about this “big credit line” promise, but X1 followed through, granting me a credit line nearly three times what most credit cards typically offer me.

You might be asking why a big credit line even matters, especially since we recommend paying off credit card balances in full each month. The answer is that a larger credit line can boost your creditworthiness. As long as you maintain low balances, the more total credit available to you will lower your credit utilization ratio. Your credit utilization refers to how much credit you have access to versus the debt (or balances) you hold -- and the lower your credit utilization, typically the higher your credit score.

For example, if you have access to $20,000 in credit and have combined balances totaling $4,000, your credit utilization would be 20% ($4,000 divided by $20,000). When you gain access to a higher credit limit, let’s say, another $20,000, your credit utilization drops even lower. For example, having access to $40,000 in credit and carrying that total balance of $4,000 would give you a lower credit utilization of 10%, which is great news for your credit score.

3. The X1’s rewards program gets better the more you spend

The primary reason I signed up for the X1 was its robust, flat rewards structure. You earn 2x points on all your purchases -- points are worth 1 cent each -- and if you spend $1,000 in a month, you get upgraded to earning 3x points. Earning three points on all purchases is the pillar of top rewards rates, and very few cards offer it. And, the cards that do offer 3% back in rewards on all purchases typically require a much higher spending threshold to unlock those rewards.

The downside: Redeeming rewards as cash back lessens their value

While you have the opportunity to earn a higher rewards rate than most cards, the X1 may only make sense if you can take advantage of its redemption partnerships. Rewards can be redeemed as a statement credit against your purchases at more than 40 brands -- including Amazon, Costco, Home Depot, Ikea, Airbnb, several airlines, Apple and more -- at a value of 1 cent per point.

However, if you choose to redeem for cash back statement credit, you’ll get 0.7 cents per point. This system is similar to American Express rewards cards, but the X1’s 1 cent redemption brands cover a wider scope of purchases.

So, if you’re a consistent Amazon or Costco shopper, frequent flyer or can otherwise take advantage of the redemption partners, this may not be an issue. But if you’re hoping to earn rewards as cash back and will spend less than $1,000 per month, you might want to turn to other cards. Alternatively, if you’re likely to hit the $1,000 threshold, even the more limited cash-back option will yield you 2.1% back on your purchases -- still a top flat rewards rate.

You can earn additional points -- up to 10x points -- on the “Shop” tab of the app as well. There are about 50 brands where you can earn extra points, including at Apple, Macy’s, Nike, Sephora, H&M, Home Depot, Lowe’s, The North Face and Walmart. You’ll have to shop through the X1 app to have these rewards applied, however. This type of feature is becoming more common with newer credit card companies.

4. The referral bonus isn’t taxable, like most others

Only some credit cards offer a referral bonus, and X1 is one of them. You can invite as many friends as you want, and if they get the card, you both can earn 4x, 5x or even 10x points on all of your purchases for up to 30 days. This can be more valuable than the typical $100 range for referral bonuses, depending on how much you spend in a month.

There’s something else that’s special about this referral bonus. While most credit card referral bonuses are taxable, because this one comes in the form of the potential to earn more points rather than a cash payout, you won’t owe taxes on these referral bonuses. That’s because the IRS considers points a “rebate” rather than income.

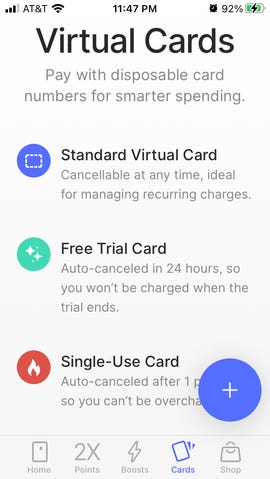

5. The virtual card capability is unmatched

The X1 app allows you to generate a variety of different virtual credit card types, demonstrating better technology than most credit cards offer. Virtual cards are one-time use card numbers meant to keep your real information secure. But X1 takes the virtual card concept a step (or two) further and expands it.

You can employ X1 virtual cards for a variety of reasons. Multiple virtual cards can be used at once, and you can cancel individual ones at any time. Or you can just start off with a virtual card set to auto-cancel after one use or after 24 hours. The virtual cards can be used to sign up for free trials, so you don’t get charged when a subscription trial ends and you forget to cancel it ahead of time. You can also give a virtual card number to others -- like a babysitter or family member -- for temporary use, and can cancel it at your discretion.

You can even make separate virtual cards to manage your automatic payments from the app at your discretion. For example, if you needed to cancel an auto payment because you were a little short that month, you could do it all from the X1 app instead of logging in to separate accounts for each payee.

6. Insurance and other protections

Some credit cards offer one or two types of courtesy protections, typically focused on an area like travel. But the X1 offers one of the broadest combinations of protections.

First, it covers your eligible purchases from damage or theft for 90 days via “purchase security,” which may reimburse you up to $1,000 for affected purchases, for up to $10,000 per cardholder. The X1 card will also add an additional year to any eligible warranties on items you buy with the card (including purchases made with virtual cards).

Cell phone protection is a rare but useful offering, too: If you pay your mobile phone bill with your X1 card, your phone is covered for damage or theft in the following month (with a $50 deductible).

It’s also rare for a nontravel card to offer trip interruption or cancellation insurance, as well as an auto rental collision damage waiver, but these perks can help prevent losses from unexpected changes to nonrefundable trips and save you money at the car rental counter.

How X1 Card compares to other cards

X1 Card

- Intro Offer

-

No current offer

- Annual fee

- None

- APR

- 15.50% – 27.75% Variable

- Intro Purchase APR

- N/A

- Recommended Credit A credit score is used to indicate an applicant’s credit worthiness and may provide guidance about account eligibility. It does not necessarily guarantee approval for any financial product.

- Good – Excellent

- Rewards rate

-

2x – 10x 2X points on every purchase regardless of category; 3X points every time you spend $1,000 in a month; 4X, 5X and even 10X points for every friend who gets a card; Up to 10X points at leading online stores such as Apple, Nike and Sephora when you shop in the X1 App

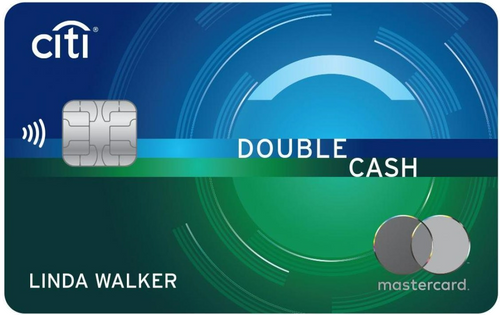

- Intro Offer

-

$200 cash back Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

- Annual fee

- $0

- APR

- 19.24% – 29.24% (Variable)

- Intro Purchase APR

- N/A

- Recommended Credit A credit score is used to indicate an applicant’s credit worthiness and may provide guidance about account eligibility. It does not necessarily guarantee approval for any financial product.

- Fair – Excellent

- Rewards rate

-

1% – 5% Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time.; Plus, for a limited time, earn 5% total cash back on hotel, car rentals and attractions booked on the Citi Travel℠ portal through 12/31/24.

- Intro Offer

-

$200 cash rewards Earn a $200 cash rewards bonus after spending $500 in purchases in the first 3 months. Select “Apply Now” to take advantage of this specific offer and learn more about product features, terms and conditions.

- Annual fee

- $0

- APR

- 20.24%, 25.24%, or 29.99% Variable APR

- Intro Purchase APR

- 0% intro APR for 15 months from account opening

- Recommended Credit A credit score is used to indicate an applicant’s credit worthiness and may provide guidance about account eligibility. It does not necessarily guarantee approval for any financial product.

- Good – Excellent

- Rewards rate

-

2% Earn unlimited 2% cash rewards on purchases

FAQs

After the approval process was completed, I was invited to download the X1 app to start using my card until it arrived via FedEx in about a week’s time. You can track the FedEx shipment right from the app.

In line with the rest of the card’s swanky branding, the app announced the card was being “manufactured” for me (marketing trick or not, it does make you feel important). I was also prompted to add the X1 Card to my phone’s wallet app, which I did for convenience.

While cash back is a more accessible concept, cash back and points both have their strengths and weaknesses. While cash back can be more universally applicable, points are often worth more in value than their cash-back equivalents. Depending on your shopping preferences and plans, you may find points or cash back to be more valuable to you.

After your card application is complete and approved, X1 will ship your card via FedEx. The issuer will send you a tracking email once your card ships. It may take 3-7 business days for your card to arrive after it ships.

Our methodology

CNET reviews credit cards by exhaustively comparing them across set criteria developed for each major category, including cash-back, welcome bonus, travel rewards and balance transfer. We take into consideration the typical spending behavior of a range of consumer profiles -- with the understanding that everyone’s financial situation is different -- and the designated function of a card.

The editorial content on this page is based solely on objective, independent assessments by our writers and is not influenced by advertising or partnerships. It has not been provided or commissioned by any third party. However, we may receive compensation when you click on links to products or services offered by our partners.