Banks charge a lot of fees -- monthly service fees, ATM fees, excessive transaction fees and many more. While all those costs can be annoying, one of the most frustrating fees that can land on your account statement is a nonsufficient funds, or NSF, fee. NSF fees are often lumped in with overdraft fees, but they’re not the same.

Read on to learn exactly what NSF fees are, why banks charge them and how you can avoid paying them.

Read more: The Best Banks with Reduced or Eliminated Overdraft Fees

What are NSF fees?

Banks charge NSF fees when you don’t have enough money in your checking account to cover a payment, whether from a bounced check or a denied electronic bill payment. For example, let’s say you’ve set up automatic bill pay with your telephone provider. If the monthly bill is $107, but you only have $50 in your account on the day it’s due, your bank might hit you with an NSF fee. And if you write a check that can’t be cleared due to a shortage of money in your account, those NSF fees can pop up, too.

Sound punitive? It is. A bank can charge you money for not having enough money. It’s why the Consumer Financial Protection Bureau has been pushing banks to do away with NSF fees. The efforts have been paying off, too. According to data from Bankrate, CNET’s financial sister site, the average NSF fee dropped to $19.94 last year -- a record low. In fact, you won’t find NSF fees at any of the biggest banks in the country.

What is the difference between an NSF fee and an overdraft fee?

NSF fees are often lumped in with overdraft fees, but it’s important to understand the difference. NSF fees are charges when a payment can’t be processed because you don’t have enough money in your account. If your bill can’t be paid, or your check won’t clear, the transaction won’t be approved and you’ll get charged because of insufficient funds.

Overdraft fees occur when a bank covers the transaction for you (instead of declining it) but then charges you. That means your bill is on time, or your check clears, but you wind up paying extra for the service. These aren’t great, either, and the CFPB has been working to do away with them as well.

Banks typically don’t charge NSF fees for debit card transactions that are declined, whether you’re trying to buy groceries or take out cash from an ATM. But the bank could allow the debit-card transaction to go through and then hit you with an overdraft fee.

Will an NSF fee go on my credit report?

Bounced checks and associated charges like NSF fees aren’t usually reported to credit bureaus. But if your check was supposed to pay a utility or credit card bill, missing a payment could affect your credit report. Also, if you wait too long to replace the missing funds, the bank may report you to a collection agency, which can also be reported to the credit bureaus.

While NSF fees won’t go on your credit report, any bounced checks or overdrafts could be reported to ChexSystems, a banking reporting agency that works similarly to the credit bureaus. Too many bounced checks or overdrafts could make it hard to open a bank account in the future.

Are there banks that don’t charge NSF fees?

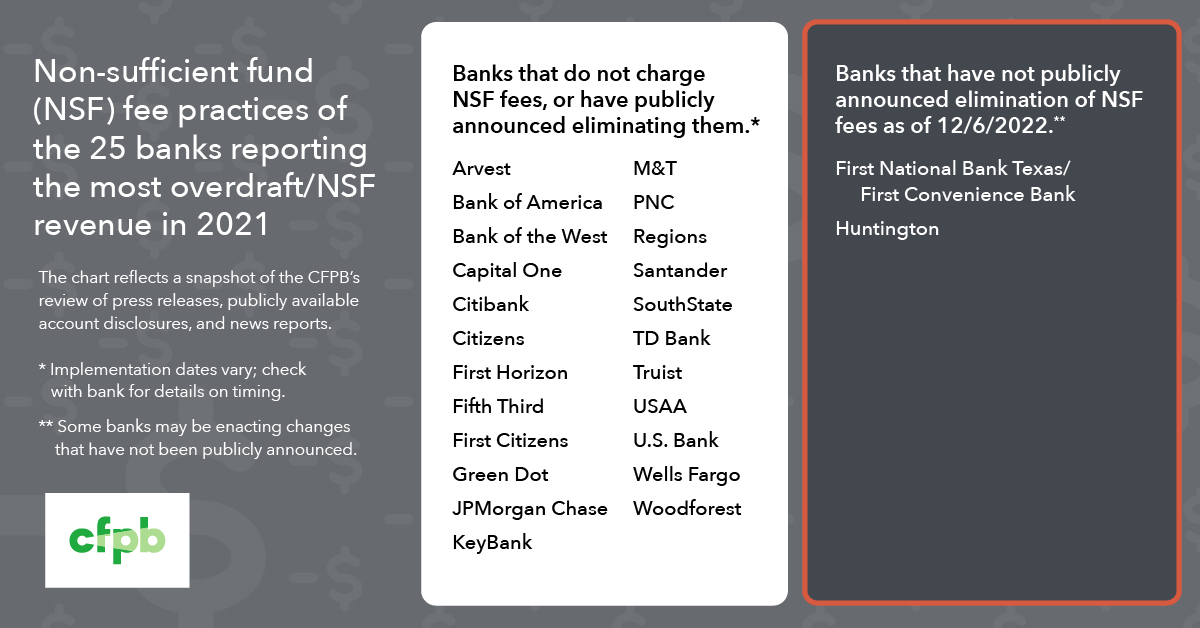

NSF fees are disappearing from the fee schedules at the biggest banks in the country. In fact, by the end of 2022, 23 of the 25 banks that had reported the most revenue from NSF and overdraft fees had eliminated NSF charges, according to the CFPB. And in some cases, banks are easing the pinch of NSF fees. The First National Bank of Texas, for example, does not charge NSF fees if the cost of a returned item is $5 or less.

{kind=link}

How do I avoid paying an NSF fee?

The best way to avoid paying an NSF fee is to open a checking account at a bank or credit union that never charges these fees. But if you’re still doing your banking somewhere with NSF fee revenue, here are some tips.

- Contact your bank. Depending on the circumstances and how reliable of a customer you’ve been, your bank may refund or waive an NSF or overdraft fee. (Don’t count on that kindness repeatedly, however.)

- Set up overdraft protection. Set up a balance transfer from a savings account with the same bank. If you dip into the red, your bank may automatically move enough funds to cover the balance. (There may be a fee associated with this service, but it will be smaller than the penalty for bouncing a check.)

- Monitor your checking account. The best way to avoid having to pay an NSF fee is not to bounce any checks. Keep close tabs on your accounts and make sure you don’t get close to zeroing out any balances. If you use online banking, set up account notifications to alert you when your balance hits a certain threshold. Rather than letting it drop too close to $0, transfer some funds to maintain a higher balance.

Criticisms of NSF Fees

Ask any consumer rights advocates about NSF fees, and you’ll hear plenty of reasons why these fees should be banned. They’re right, too. While you might get frustrated by other banking fees, at least you’re getting some type of service in return, like accessing cash from an out-of-network ATM, for example. With NSF fees, however, all you get is an extra cost.

The other concern is that NSF fees tend to add up for individuals who are already struggling to make ends meet. If you don’t have enough money in your account to cover a transaction, another fee is only going to make life worse.

“NSF fees intensify financial distress for consumers, who often are already at their financial edge and who will often also be hit by the fee merchants charge when a consumer’s payment bounces,” the CFPB noted in a statement last year.

The Biden Administration is working to eliminate overdraft fees and NSF fees, which both fall under the administration’s description of junk fees. While NSF fees still exist at plenty of institutions today, it seems likely that more will be eliminated.

FAQs

Some banks charge an NSF fee when a customer’s balance is not high enough to cover the cost of a bill payment or a check. The money represents significant revenue for banks: NSF fees cost an average of just under $20, according to Bankrate’s most recent data.

Technically, NSF fees are legal, although the CFPB has been working to get more banks to eliminate them. For now, expect NSF fees to continue showing up on some depositors’ statements.

NSF fees are capped by state laws, which typically range from $20 to $40 per transaction. It’s up to each bank to determine the cost of their NSF fees within the legal limit.

Technically, an NSF fee won’t hurt your credit. It’s important, however, to understand what type of transaction didn’t go through due to lack of funds in the account. For example, if you miss making a minimum credit card payment due to a low balance, that late payment will show up on your credit report.

Editor’s note: An earlier version of this article was assisted by an AI engine. This version has been substantially updated by a staff writer.