Why Sprint's push for a T-Mobile merger will likely be in vain

[commentary] It's clear the powers that be at Sprint aren't willing to give up on a bid for T-Mobile. But what are the company's chances of making headway in convincing regulators to accept a deal?

Once Softbank CEO and Sprint Chairman Masayoshi Son gets a bee in his bonnet, he's apparently a hard man to discourage.

Despite the fact that regulators have already expressed their skepticism of a deal between Sprint and T-Mobile to Son and Dan Hesse, Sprint's CEO, Son is not giving up. The Wall Street Journal reported this week that Son plans to take his arguments for why more wireless consolidation is needed to business and policy leaders gathering in Washington, DC, at a US Chamber of Commerce event on March 11.

While the article said that Son isn't expected to mention T-Mobile by name, he is likely to continue his mantra about why it's important for smaller wireless operators to combine efforts to compete against AT&T and Verizon Wireless.

But try as he might to make the case for consolidation, Son will still have a hard time convincing policy wonks inside the Beltway of his plan. Even though a merger with T-Mobile would effectively double Sprint's customer base, it does very little to improve its spectrum position or expand its footprint. And it's these two factors -- footprint especially -- that determine success in the wireless market.

Is bigger better?

Fundamentally, Son's argument hinges on the fact that Sprint, T-Mobile, and a slew of smaller regional players are dwarfed in comparison to AT&T and Verizon Wireless. These two carriers control more than two-thirds of the nation's wireless subscriber base and the bulk of the industry's profits. And Son has argued that it's impossible for any single player to compete against such a duopoly. As a result, Americans pay higher prices for their service and it's not as fast or as reliable as coverage elsewhere.

In order to effectively compete, Son has said that Sprint needs scale.

"With scale merit, we don't have to settle with No. 3. We can compete fiercely," Son said during the company's earnings call last month.

Son argues that this scale will help the company build out its network more quickly and with less cost. This notion of scalability is one that most executives use to justify mergers of any kind. The idea is that by consolidating functionality, the bigger business can run more efficiently. And in the wireless world, having more subscribers means better leverage with device manufacturers to secure superior terms for handsets and network equipment.

It's an argument the persistent Son has used with regulators to grow his business at home in Japan. The company fought and won to acquire Vodafone Group's Japan operations in 2006.

Once the company made that acquisition, it had the scale to get the attention of major phone manufacturers. It quickly began slashing prices to upend competitor NTT DoCoMo. And it got Apple's iconic iPhone, which also helped strengthen its competitive position.

In an interview with the Journal in 2012, Son said that AT&T and Verizon were too concerned about keeping shareholders rich and happy with healthy profit margins and big dividends. And he suggested he would do as he had done in Japan and force competitors to choose between cutting prices or losing customers.

There may be something to Son's argument that having a larger customer base will help in terms of scalability and cost savings.

The problem is that T-Mobile, which is the smallest of the big nationwide wireless operators, is actually already shaking things up. The company, which had for several quarters been losing customers, actually added 4.4 million subscribers in 2013. Its aggressive moves to eliminate contracts and reduce pricing have gotten the big players to respond. AT&T and Verizon have each tweaked their plans to reflect the stiffer competitive pressures.

While neither of these players has dramatically changed their plans in response to T-Mobile, the fact that the two largest carriers have even budged is likely a sign that competition is working. And as T-Mobile continues to push its Uncarrier strategy and roll out new initiatives, it's not inconceivable that the bigger players will continue to respond.

Of course, it's hard to say if T-Mobile will be able to sustain its strategy. In spite of its quick growth, the company saw heavy losses in the fourth quarter.

The real reason Sprint and T-Mobile can't compete

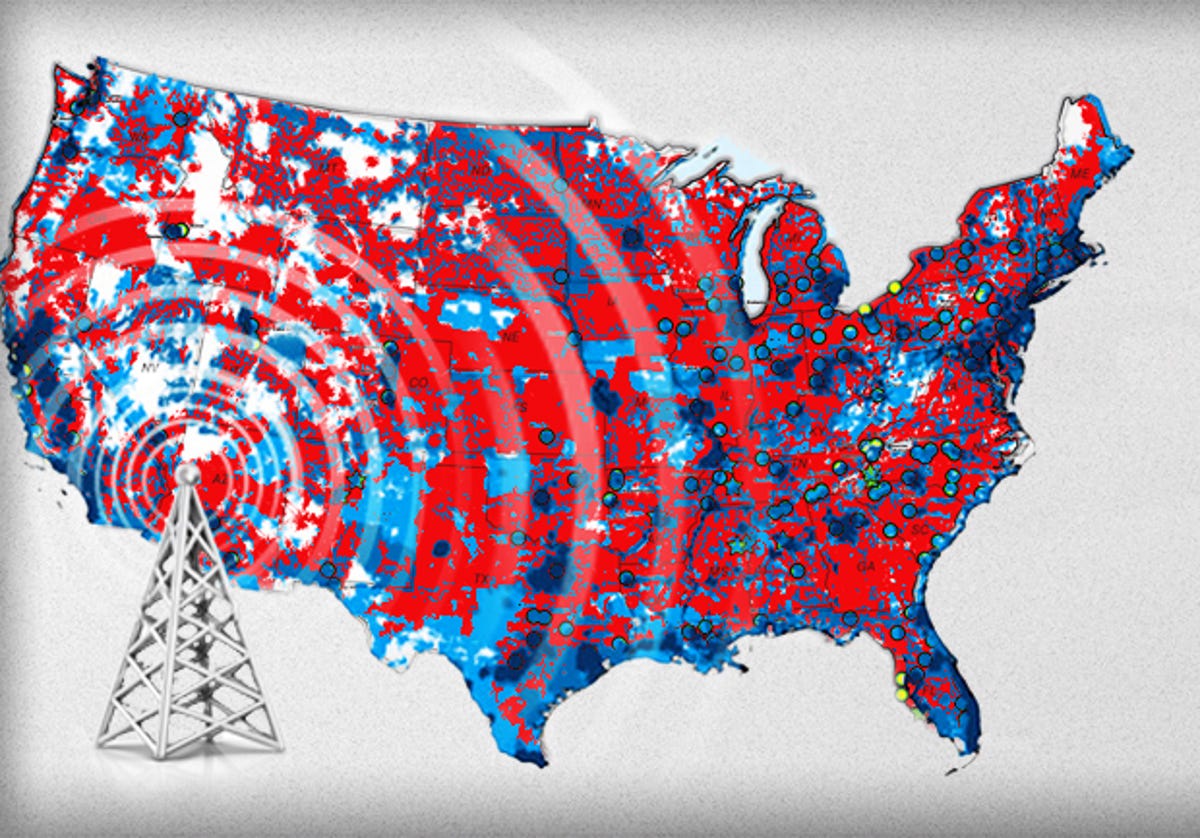

But it seems that Son might be missing the real reason why AT&T and Verizon dominate the US wireless market as much as they do. It's not just the large subscriber base that keeps AT&T and Verizon on top. It's the fact that their networks are truly nationwide. They offer service in large cities as well as in the suburbs. And when you're in many rural areas of the US, you're more likely to find an AT&T or Verizon Wireless signal than you are a Sprint or T-Mobile signal.

The two biggest reasons for this are the fact that AT&T and Verizon were essentially born from years of consolidating smaller regional operators throughout the country. So they have amassed networks and spectrum licenses that cover the entire US. AT&T and Verizon also have acquired a wide variety of low-frequency and high-frequency spectrum. This has not only allowed them to use low-frequency spectrum to more cost effectively expand networks in suburban and rural areas, but it also has helped with in-building coverage within dense urban settings.

Meanwhile, Sprint and T-Mobile each lack the breadth of network footprint as well as the scope of wireless spectrum holdings. T-Mobile especially is primarily confined to urban markets with little to no coverage in adjacent suburban or rural markets. Sprint isn't much better in terms of coverage.

The companies also lack a wide mix of low-frequency and high-frequency spectrum. Most of Sprint's spectrum holdings are in the higher-frequency bands. The spectrum it acquired from last year's acquisition of Clearwire is also higher-frequency spectrum. Sprint does own some lower-frequency spectrum through its merger with Nextel, but due to a variety of interference and network transition issues, the company hasn't used it to extend its network. That said, Sprint's massive network upgrade, which will make its network more flexible, will allow it to leverage this spectrum and integrate other network technologies more efficiently.

Up until last year, T-Mobile had no low-band spectrum at all. Through a spectrum deal with Verizon Wireless, it got its hands on some A block 700 MHz spectrum. While this is a significant acquisition for T-Mobile, most experts agree it's only a start. Most of the licenses that were acquired in this band were in cities already served by T-Mobile. So the company won't be able to use the spectrum to move into new markets. But it should help T-Mobile improve better in-building coverage. And most experts agree that T-Mobile still needs more low-frequency spectrum.

I would argue that the lack of true nationwide coverage and poor indoor coverage are two major factors that have kept Sprint and T-Mobile in third and fourth place respectively in the US wireless market.

True nationwide coverage is crucial for a wireless provider, because the service is meant to be mobile, which means that the people using these services don't stay in one place. And the bottom line is that people will only subscribe to a service that works where they use their phones. So the fact that Sprint and T-Mobile have been unable or unwilling to expand their networks deep into suburban and rural territories has limited their customer base -- a limitation that neither AT&T nor Verizon faces.

Consider this: Many people who work in large cities live in the suburbs. So even if they could subscribe to a Sprint or T-Mobile service that works fine in the city where they work, these services may not work at their homes. And even if the service works at home and at the office, it may not function on the way to and from work.

What's more, many people travel throughout the country, and they expect their phones to work wherever they go. This is especially true of so-called high-value customers who are more likely to travel for work or to have vacation homes in areas where a wireless operator whose network is concentrated in an urban area may not have coverage.

Why Comcast-Time Warner Cable and not Sprint-T-Mobile?

Some people have suggested that Son may be feeling emboldened by what appears to be the Department of Justice's and Federal Communications Commission's willingness to consider a merger between the No. 1 and No. 2 largest cable operators in the US. But the truth is that comparing these two mergers is a lot like comparing apples and oranges. Yes, they're both fruit, but they're very different.

First, at a basic level, the wireless market is far more competitive than the fixed line broadband market. In many metropolitan areas there are at least four choices for wireless service, plus dozens of operators reselling service from one of the big four operators.

By contrast, cable markets were designed as monopolies. Years ago, when cable companies came into communities to offer TV service, they were granted exclusive franchise agreements. And so for years, the cable operators were prohibited from building networks and competing in another cable company's territory. As a result, Comcast and Time Warner Cable essentially do not overlap in any meaningful way when it comes to their network or customer base.

What this means in terms of assessing whether a merger is good or bad for competition is that in the case of the wireless market, you typically have at least four major players in most major markets: AT&T, Verizon Wireless, T-Mobile, and Sprint. There are few markets where T-Mobile and Sprint do not overlap. So when you combine these companies, customers in those markets that were once served by four major wireless operators will now have only three choices.

The situation is very different for Comcast and Time Warner since the companies don't overlap at all in terms of their footprint. If the two companies merged, there would be no loss of a competitor in any single market. In other words, consumers living in Time Warner Cable's territory never had the choice of subscribing to Comcast. Likely their only choice has been Time Warner Cable. If they were lucky they might be able to choose a satellite provider like Dish for TV or a telecom such as AT&T and Verizon, which has been building high-speed broadband in both Comcast and Time Warner Cable territory to compete.

After a merger between Comcast and Time Warner Cable, customers would have the same number of choices for high-speed Internet, TV, and phone service that they had before the merger.

The conclusion

So what does this all mean in assessing whether combining Sprint and T-Mobile would actually benefit consumers or not? T-Mobile is making headway with its Uncarrier strategy. The 4.4 million customers it added to its network last year came from other carriers. So it's clear that the lower prices and marketing message are resonating with some consumers. But the company still isn't able to persuade many customers who otherwise would be very willing to try the service, because it simply doesn't offer coverage where these customers live, work, or travel.

Furthermore, because Sprint and T-Mobile compete in essentially all the same markets as well as lack coverage in most of the same markets, merging the two companies together does not achieve the one objective they each need to compete more effectively, which is to increase their footprints. In addition, because most of their individual spectrum holdings are in high-frequency bands, they don't gain spectrum assets that would help them build to unserved areas.

And, of course, there is the fact that both the Justice Department and the FCC rejected AT&T's acquisition of T-Mobile, stating that four nationwide carriers rather than three is most beneficial for competition. Regulators have essentially been slapping themselves on the back for rejecting the megamerger between AT&T and T-Mobile.

So what's likely to happen? No matter how persistent he is, I still think that Softbank's Son will have a difficult time convincing regulators and policy experts, or even business leaders who understand the wireless market, that a merger between Sprint and T-Mobile will create a single rival that can truly change the US wireless market. Based on the carriers' current spectrum holdings and network footprints, there isn't much to be gained from this merger.

That said, Son may try to convince regulators and business leaders that a larger customer base and more business synergies will provide the necessary capital for the combined company to invest in acquiring new spectrum and build out its network. The problem is that regulators would have to believe that the combined companies would actually make good on these promises. That could be tough given Sprint's disastrous past experience integrating the Nextel network with the Sprint assets.

Instead, I think regulators will want to take a wait-and-see approach. I imagine the FCC, in particular, will do its best to create an environment over the next two years in which Sprint and T-Mobile will have an opportunity to purchase more wireless spectrum in the hopes that the companies can use these assets to further scale their businesses.

Two important spectrum auctions are coming up over the next two years. There is the AWS-3 auction in September, which will auction higher-frequency spectrum. But since AWS is already so widely used, the spectrum licenses in this band are considered valuable because they could make roaming between networks easier. Operators that use this frequency band could also benefit from a wider handset and network ecosystem.

The second auction is the broadcast TV spectrum in the 600MHz frequency band. This is the last bit of unused low-frequency wireless spectrum that is likely to come up for bid. It's going to be a complicated auction to design given that there will be an incentive reverse auction, which will determine which broadcast spectrum will be made available for wireless operators to bid.

But I firmly believe it will be these auctions, more than a merger between T-Mobile and Sprint, that will determine the fate of the US wireless market. If Sprint and T-Mobile can get their hands on enough of this valuable spectrum and still have enough capital to build out their networks, the likelihood of one or both of these companies being able to unseat AT&T or Verizon is much greater.