Lending Club plans IPO -- maybe within 18 months

The startup, which offers borrowers and lenders better interest rates than banks, is angling to become a publicly traded company.

- Shankland covered the tech industry for more than 25 years and was a science writer for five years before that. He has deep expertise in microprocessors, digital photography, computer hardware and software, internet standards, web technology, and more.

PARIS -- Lending Club, a startup that connects people who want to borrow money with those who want to lend it, is profitable and plans to go public.

Chief Executive Renaud Laplanche discussed the initial public offering at the LeWeb conference here. "We're planning on going public in the next few years," he said in an on-stage interview, then confirmed he'd earlier said 18 months.

An IPO of course brings new funds, though Lending Club currently has $50 million in cash, but Laplanche said he wants to go public for the higher profile it brings. "There are a lot of benefits of being public," he said.

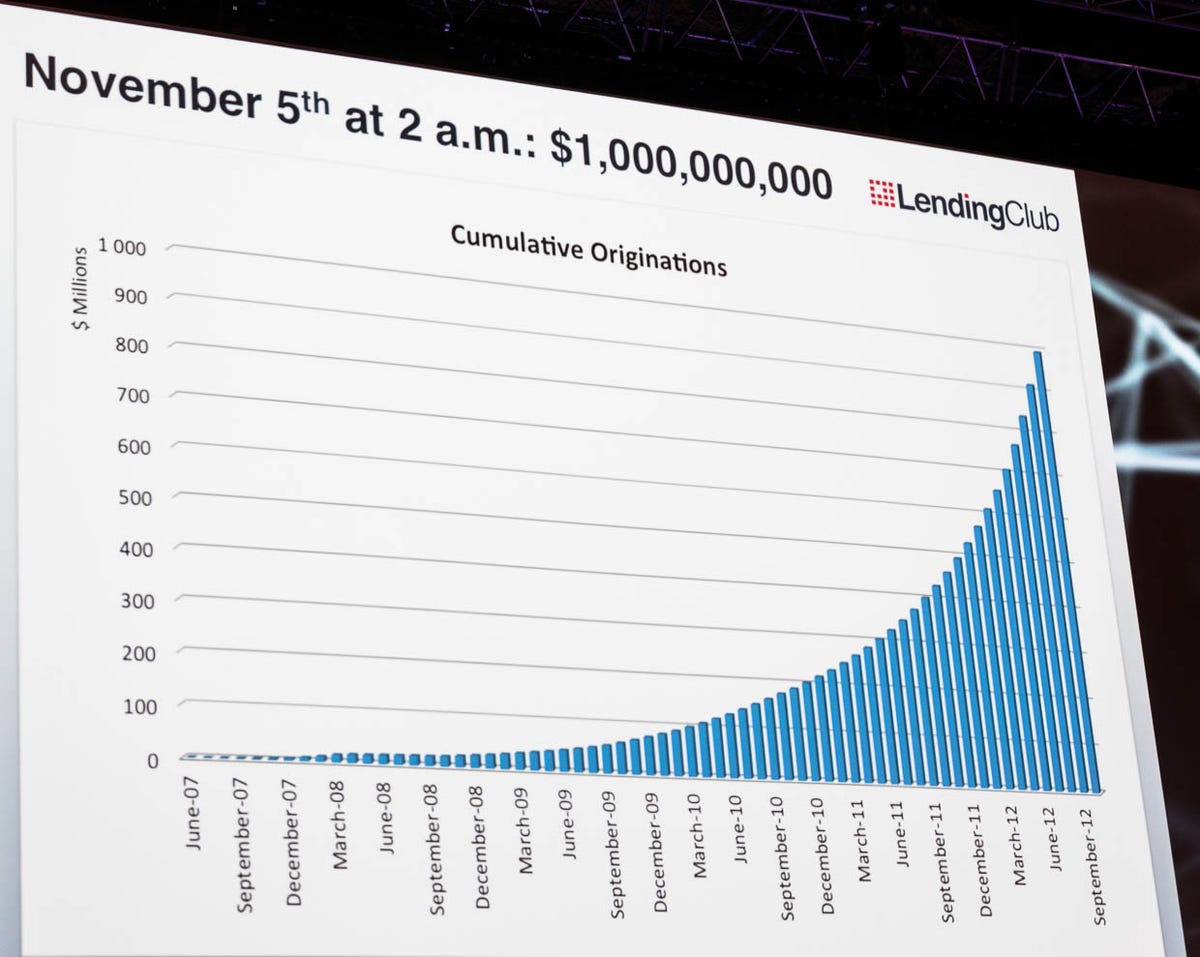

Of course, publicly traded companies also must keep the shareholders happy with revenue and profit. There, Lending Club has plenty of growth it can show off. It originated $100 million in loans in April 2011, $500 million in February 2012, and $1 billion in November 2012.

More growth is possible, too, Laplanche said. Today's emphasis is on refinancing credit card debt at lower interest rates, but it aspires to enter other lending markets, too: student loans and home mortgages.

Laplanche had the idea for Lending Club when looking at a credit card statement, he said.

"Why is it if I put money into a bank I'm going to earn 1 percent interest, if that, but if I borrow the same money from a bank, I pay 18 percent?" he said. "That seemed like a very big spread. When you're an entrepreneur and you see a big spread, you immediately think big disintermediation opportunity."

Lending Club loans are offered at an average interest rate of 14 percent, though those with good credit ratings can borrow as low as 7 percent, Laplanche said. With a default rate of about 3 percent and Lending Club's fees, borrowers typically make about 9 to 10 percent interest.

Lending Club gets by with a narrower spread by using the Internet, of course, and forsaking a lot of banking overhead like branch offices. Traditional banks have operating expenses between 5 to 7 percent, but Lending Club's is at 2 percent and dropping as it gets bigger.

"We're applying technology to an existing, proven market," he said.

And it's outpaced a half dozen or so other rivals that got started at the same time. Lending Club has benefited from economies of scale: "The larger a marketplace gets, the more attractive it gets," he said. Lenders have a choice of people to lend money to, and borrowers get funded faster.