Let's face it.

If you're gonna buy a car, it's fun

It's an emotional decision.

It's, I want that car.

Or I want one of those three cars.

You go down to the show room and yeah, there's a lot of haggling and looking around.

A lot of research online.

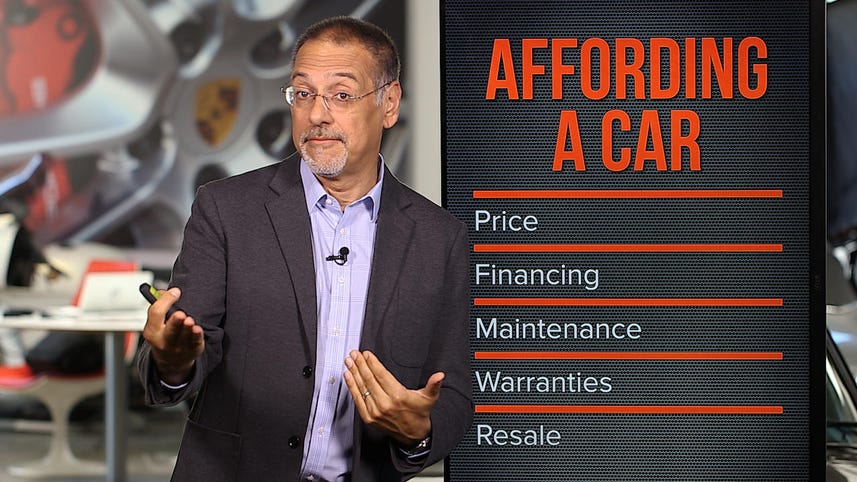

But in the end affording a car, is a very different process.

And it boils down to five things.

First off, buy or lease.

Now if you think leasing is just for business, think again.

About a third of all buyers now lease their car, with millennials doing so the most.

Leasing is a great way to get into a new car with little down.

You're gonna have lower payments over the term of the lease, probably three years.

It's a way to get a new and cycle yourself every few years.

Purchasing is for those who, A, might feel more comfortable buying car.

Knowing that they wanna own the car for more than three or four years.

They wanna pay the car off over a period of time and they just have that sense of I want ownership.

The most obvious component is of course, the price.

But know this about selling new cars Most new carried departments and dealer don't really make money when they sell that new car.

The car itself is almost [UNKNOWN] Reader, thus of course is the information here, so it's easy to look up what a given car is actually fetching in the market around you This is welcome relief from the days of going to the used or new car lot.

We're wheeling and dealing on the new-

And haggling with shell game concepts like sticker price, invoice, and dealer markup.

Look for the big Ford tower on Stevens Creek.

The dealer must tell you about customer incentives.

Those are things like rebates or special financing offers.

But there are also incentives that are, frankly, none of your business.

[MUSIC]

Like monthly sales volume bonuses the dealer may get from the factory.

And if they think they're going to sel a lot of cars and get one of these bonuses, then they reduce the price of each car they sell upfront.

Now if the price has been established, now that there's a financing component that over 90 percent of people take advantage of Through the dealership.

Now that means they're going to either lease you the car or give you timed payments on the car.

And the dealer gets a cut, gets a payment or a fee or a kickback on any of that they arrange.

It's nothing sneaky.

It's part of the service they provide you.

But it's a big part of their profit on the car.

Long term loans were getting very common this days.

About a third of new car loans today are between 73 and 84 months.

But time cost money, if you buy the average new car about 335 and finance about 24,000 of that at a nice rate of 3 1/2% after your trading and down.

You can see, a long loan costs a whole lot more than a short one.

Now, leases are a very different animal.

A lot of people just know they're gonna make a car payment.

They don't wanna be stuck with a car for four, five, six, seven years Leases vary based on several things.The lease money factor, which is basically its interest rate, the capitalized cost or CAP reduction, this is basically a down payment and the residual value, this states what your leased care is going to be worth when you bring it back to the dealer.

It's like resale value, but with a different name, because you won't be reselling the car, you'll be returning it.

So you got your car, you got the right price, and you either leased or financed it as a purchase.

Now you gotta live with the damn thing.

This breaks down into several areas.

Reliability.

JD Power or consumer reports can give you some idea of this.

But remember the top rated cars are often high end cars.

So although they do have infrequent breakdowns, Those breakdowns may cost more to fix.

Insurance cost, you always want to compare this at one of the various online estimators.

Fuel economy and type, a lot more cars than might surprise you require premium these days.

Fuel prices will vary in the years ahead but if you have premium, we know it's going to be a delta higher.

And that alone can add hundreds of dollars a year to the cost of driving any car you buy.

And maintenance intervals.

And remember, you can take your car to any shop to get maintenance done, and still keep your warranty in place.

You can even do maintenance yourself, but document it.

And pay attention to warranties.

I can't tell you how many folks I know buy a car and don't know how long the factory stands behind it.

There's a world of difference Between a five year 60,000 mile policy and a 10 year 100,000 mile factory warranty.

That's several years when your engine could blow and fundamentally turn you upside down on the car for as long as you have it.

There are also extended warranties and damage plans that dealers will try to sell you and sometimes these make sense depending on how you intend to use the car.

An extended warranty usually tries to replicate what a factory warranty offered, but for more time.

Now related to these extended warranties are damage protection plans.

These often covered things like paint or tire damage and wheel scrapes.

Things of that nature that happen fairly frequently.

And depending on your track record with a vehicle, where you store it, what the roads are like where you drive, this may or may not make sense.

But these are often third party insurance policies that are quite a bit different from factory warranties.

Make sure you know who they pay, you or the shop, where the work can be done, a dealer, a shop, any shop, if they duplicate factory coverage for some of their period, what are the deductibles and what don't they cover, and how much and/or how often can you use the coverage.

Now, the last of our five key concerns is the one that most people ignore or don't understand, and it's perhaps the most important.

And that is resale value, or what's called residual value.

That's what your car is worth down the road at the end of your payments, if you're buying it, let's say, or at the day that you turn it back on a lease after two or three years.

This is important because if you buying the car a nice high resale value means you've got a much fatter trade in for your next car.

Or your gonna get more money on it when you sell it on the private market.

If your leasing, a high residual value down the road is gonna make your lease payment lower along the way.

Because the dealer knew they were gonna get a more valuable car back at the end Now, I'd like to tell you there are a bunch of things you can do to pull levers and make your resale value higher than the other guy, but a lot of it is factors that are out of your control.

Popularity and scarcity of a model.

How many of those same cars went into rental fleets?

How many cut-rate finance and lease deals, like you may have taken advantage of, were offered to other people?

How many are coming back to dealers after a lease?

And regional appetites.

A Subaru is gonna fetch a lot more in Vermont than it will in New York City.

So when you go shopping for a car, please don't obsess on getting the price

Put down $500 or $1000 and think you won, that's the opening gambit.

This is your list of things to do to afford a car and not just buy a car.

[BLANK_AUDIO]