Why You Can Trust CNET

Why You Can Trust CNET Advertiser Disclosure

How to Read Your Free Credit Report

It's arguably one of the most important free documents you'll want to understand.

Do you know what's in your credit report?

Understanding your credit report is an important part of financial literacy. The report not only dictates whether you can get a credit card or an auto loan, it can also factor into landing a job or securing a home. With multiple ways to access your credit report for free, there's little reason not to review yours to understand where you are financially, if you've been a victim of fraud and how to start repairing your credit.

How can I get my free credit report information?

Visit AnnualCreditReport.com to access your free credit report from Equifax, Experian and TransUnion. You can request from eacah bureau at once or space them out throughout the year. Usually, you're only allowed one free report from each bureau each year, but due to the pandemic-era laws, you can get free credit reports every week through December 2023.

What should I look for when reading a credit report?

When reviewing your credit report, be sure to double-check all of the identifying information, including your Social Security number and all listed addresses. Look for any unfamiliar accounts, payments marked as late when they weren't and hard inquiries you didn't authorize. The information on your credit report is used to calculate your credit score, a three-digit number that lenders use to determine if you are a good credit risk. If you spot any errors or accounts that you didn't open, you may be a victim of credit card fraud or identity theft.

Below we explain what's in your credit report and what to keep an eye out for.

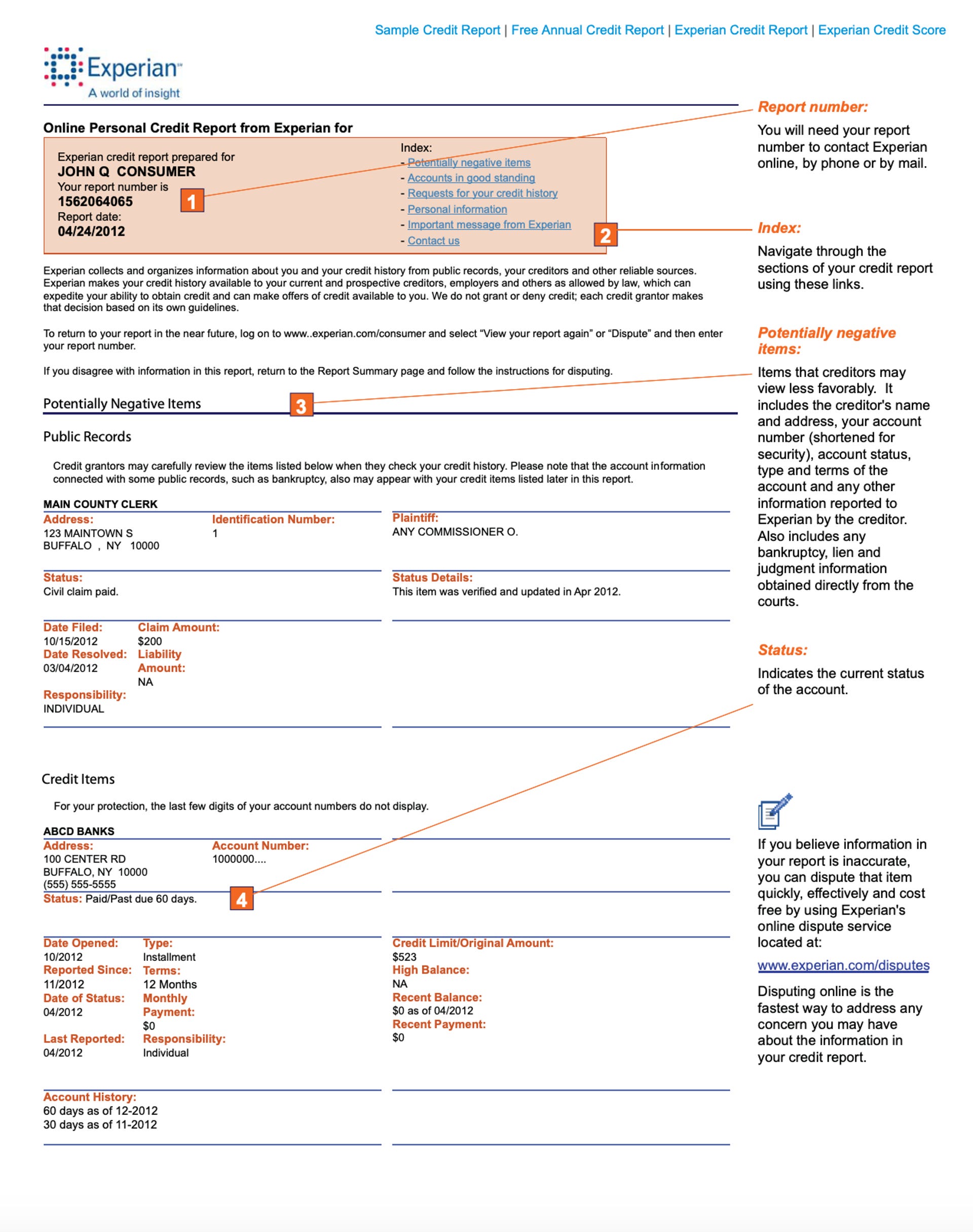

Personal information

This section is self-explanatory and also one of the most important parts of your credit report. This is where you'll see your Social Security number, date of birth, name, employment data and addresses, both previous and current. It's important to make sure these details are correct.

The first page of a sample credit report from Experian.

Credit account information

Here's the credit part of the credit report. The accounts under your name, including credit cards, personal loans and other revolving lines of credit, are listed here. Each entry should include:

- Account type

- Date opened

- Credit limit or loan amount

- Current balance

- Status of account

- Payment history

When reviewing this section, you want to verify that each account listed is yours. If there's an entry that's not yours, then you'll need to file a dispute with the agency that provided the report.

Aside from confirming that the accounts are legit, you'll also want to confirm that the info is accurate. Each account listing will show whether you made a late payment, and the more late payments there are, the more it'll negatively affect your credit score.

This section of the report will also show closed accounts. Most credit details will stay on a credit report for seven years.

Inquiry information

If a bank, realty company or employer requests a copy of your credit report, often called a "hard pull," the inquiry will be listed here. Having an excessive number of such requests can negatively affect your credit score.

There are also promotional inquires, or "soft pulls," usually conducted by financial institutions that want to offer a preapproved line of credit, or by credit monitoring companies that review your details as part of their services. These organizations request some info from the credit card company, but they don't receive all the data from the credit report. These kinds of pulls don't impact a credit score like the hard inquiries do.

Card issuers will also periodically review your credit info for various reasons, such as increasing or lowering your credit limit. Like the soft pulls, these account review inquiries don't reduce a credit score.

Bankruptcy and public records

If you've filed for bankruptcy, the details will be listed in this section, including the type of bankruptcy, date filed, which court and how much you're liable for.

Other public records also show up here, such as any court judgments against you. Listed details may include the company that filed the suit, how much it was for, the court where the suit was filed and the judgment on the case.

Collections accounts

A company may turn over an account to a collection agency after a period of time if no payments are made. This includes creditors, as well as doctors, hospitals, cable companies and mobile service providers. In some cases, the collection agency's info will be listed here, and not that of the original company that's owed the money. Just like the credit account info, it's important to verify the details in this section.

To see what a full credit report looks like, click to the sample of an Experian report, below.

How can I dispute errors on my credit report?

If there is inaccurate or incomplete information on your report, you should contact both the credit bureau and the company that reported the error. You can typically contact the credit reporting companies online, by mail or phone. Explain -- preferably in writing -- to all parties what you think is wrong, and include copies of documents that support your dispute.

The credit bureau may take up to 30 days to investigate your dispute. If the information is found to be inaccurate or incomplete, it will be updated or deleted from your report.

The bottom line

Checking your credit report regularly can help you identify inaccurate or incomplete information, know what lenders may see, ensure accounts are reported properly, detect and dispute errors, stop identity theft and credit card fraud early on, save money by being proactive about your credit, and save time and hassle in the future. Pulling your own report won't hurt your credit score and usually takes no longer than 10 minutes.

The editorial content on this page is based solely on objective, independent assessments by our writers and is not influenced by advertising or partnerships. It has not been provided or commissioned by any third party. However, we may receive compensation when you click on links to products or services offered by our partners.