Hello, Apple Pay, good-bye credit cards? All bets are off

Apple wants to replace plastic credit cards with the Apple Pay mobile wallet and the new iPhone 6. It's not the first to attempt such a feat. Will it finally be the one to succeed?

The new Apple Pay service is not much different from other mobile wallets already on the market, but it's likely to have a better chance than any other solution of getting people to use smartphones to pay for things.

Google, PayPal and joint venture Softcard (formerly Isis) -- made up of three of the nation's largest wireless operators -- are just a few of the companies that have spent years and millions of dollars trying to convince consumers that they should chuck their plastic credit cards and instead pay for things with a smartphone or mobile app.

Now Apple is getting into the game, unveiling Apple Pay this week at a splashy event that also introduced the Apple Watch and the big-screen iPhone 6 and iPhone 6 Plus to the world.

But so far, consumers have not seen a real need to stop using the plastic cards that already line their wallets. As a result, very few people have actually ditched other forms of payment in favor of using their phones. The number is so small in fact, most market research firms aren't even tracking it.

"Contactless mobile payments is a rounding error for the big payment networks," said James Wester, global research director for mobile payments at industry analyst firm IDC Financial Insights.

The reason? It's simple. Consumers don't have a problem paying the old-fashioned way.

"Paying with a credit card is not that difficult even if you have a fat wallet or a really messy purse," Wester explained. "Even really small children understand how a plastic card works. So to be really successful in mobile payments, you actually have to be better than any other form of payment out there including cash and credit cards."

That sounds like a pretty tall order. But if any company can create a user experience that will convince consumers to change how they do something as fundamental as pay for things, Apple is a good candidate for the challenge, Wester added.

"That's what Apple does," he said. "They are masters at creating unique, compelling user experiences. Apple's entry into the mobile payment space could be the tipping point we've been waiting on."

Other payment experts agree that there is nothing special about the technology or features that Apple is offering in Apple Pay . In fact, several other mobile wallets -- including Google Wallet, PayPal's mobile app and the Softcard mobile wallet -- offer the same exact capability. All three of these companies offer even more flexibility, tying merchant offers, coupons and loyalty programs into their wallets.

Still, Apple's entrance into the market may be the catalyst needed to push consumers and merchants over the edge into greater mobile-payment adoption.

"There's nothing particularly revolutionary about Apple's implementation of mobile payments," said Jason Oxman, CEO of the Electronic Transactions Association. "But Apple can get people excited. That's good for everyone else since even getting people talking about mobile payments and looking for ways to use their phones to buy things could benefit all the other competitors."

A lesson in history

Apple has transformed other well-established markets in the past. And the company has demonstrated that it can change consumer behavior, even when those consumers don't realize they were looking for a new way of doing something.

The digital music market is a key example. Apple almost single-handedly killed the physical CD format for purchasing music. Other digital music stores already existed when iTunes came on the scene, and there were also other digital music players before the iPod. But Apple's iPod and its iTunes store transformed how consumers bought and listened to music.

"Remember when we all used to buy CDs?" Oxman asked. "Apple didn't invent the online music store or an MP3 device to play music. But it somehow created a market in which people no longer buy CDs."

A key part of Apple's potential success in mobile payments is likely to hinge on the long list of key partnerships it lined up for the launch of this new service. Unlike Google, which forged the path with mobile payments three years earlier, Apple had an impressive list of partners lined up before it announced Apple Pay. When the service launches in October, Apple will have deals with three of the four major credit card payment networks in the US. And it has already partnered with six of the largest financial institutions in the US, including Bank of America and Chase, which combined control roughly 80 percent of the credit-card-issuing business in the US.

In some ways, it could be argued that Google paved the way for Apple. Google Wallet also uses the short-range wireless technology known as NFC (near-field communications) to make the actual payment using a mobile device. Since its Google Wallet launch in 2011, Google has been working with merchants to install and turn on NFC capabilities on payment terminals. In fact, most of the large retailers that Apple highlighted as accepting Apple Pay are also partners for Google Wallet. These include big names such as Macy's, Walgreens, and Duane Reade.

An uphill battle

Still, Apple's success is not guaranteed. Like others that have gone before it, Apple could also experience a bumpy road as it tries to spur adoption, said Anuj Nayar, senior director of global initiatives at the well-established PayPal service.

"The entire industry has been waiting for Apple to come into the mobile-payments market," he said. "There has been an expectation that they would bring something game-changing to drive mobile-payment adoption in the US to the next level."

But he said that the solution Apple unveiled in Cupertino, Calif., this week was a bit of a disappointment, doing little more than providing an alternative to a 16-digit plastic card. He said that Apple needs to give consumers a compelling reason to use its Apple Pay service.

"Are people really that desperate for another way to pay with a credit card account?" he asked.

This is why payment companies have looked for other ways to add value to their digital wallets. PayPal, for example, has quickly ramped up its deals offerings with merchants in the last year, while also adding the ability to preorder and pay for food. Google Wallet has added the ability to include a payment button attached to its wallet to other apps. It has also built its entire digital wallet platform on leveraging coupons and loyalty programs. And it's added the ability to send payments to individuals from its app and its Gmail service.

Apple is also offering some of these features. For instance, like PayPal and Google Wallet, apps and online sites will be able to embed an Apple Pay button in their e-commerce apps. This will allow consumers to do things like pay their restaurant bill through the OpenTable mobile app or order ahead for soup and a sandwich at Panera.

What seems to be largely missing from Apple's offering is integration between Apple Pay and merchant coupons or loyalty programs. The company made no mention of its geofencing technology iBeacon, which could allow merchants to push offers directly to consumers when they are in stores.

Even though Apple's Passbook, which will work in conjunction with Apple Pay, can store coupons and loyalty cards, Apple executives made no mention of a direct link between Apple Pay and coupons or loyalty programs stored in the mobile wallet. In fact, Eddy Cue, head of software development for Apple, seemed to emphasize that Apple had no intention of pushing offers to consumers or using purchasing history to help merchants target consumers.

"Apple doesn't know what you bought, where you bought it, or how much you paid for it," he said during the keynote. "And the cashier doesn't see a name, credit card number, or security code."

Even Apple's key credit card payment network partners say that Apple needs to offer consumers something more than a replacement for their plastic cards.

"The attraction for consumers has to come from the value portion beyond payments," said Jorn Lambert, a Digital Convergence executive for Mastercard. This includes things like digital receipts, coupons and offers.

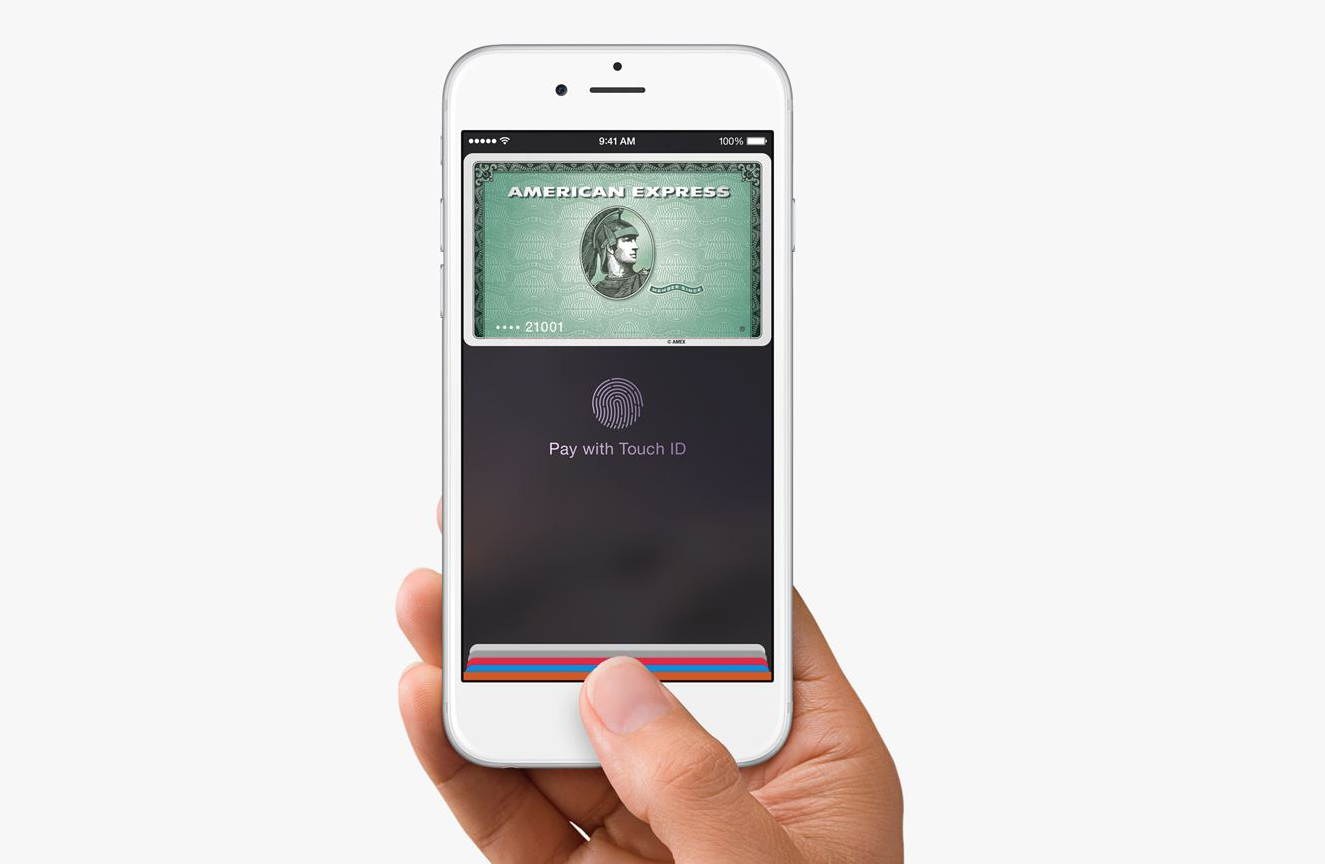

But Lambert thinks that despite these limitations, Apple has made its digital wallet much easier to use than others on the market, especially through the use of the TouchID biometrics.

"It makes it a very smooth thing to do," he added.

Is security the answer?

TouchID not only makes it easier for a consumer to access the wallet, but also more secure. And it could be this notion of beefing up security that Apple hopes will resonate with consumers.

A survey published in July by Thrive Analytics found that the reason that so few customers use their phone to pay for things is because they are concerned about security and they fear a "lack of usability."

"An overwhelming majority of consumers acknowledge the presence of digital wallets, however a minority have actually used them despite fewer shoppers carrying cash today," Jason Peaslee, a managing partner at Thrive Analytics, said in a statement when the study was published in July.

Apple executives seem to understand what may be holding consumers back from adopting mobile payments. During the keynote Tuesday, Apple's Cue played up the advanced security features of Apple Pay as compared to the old magnetic-strip technology used on credit cards. He explained the company's use of tokenization, a way of encrypting credit card information so credit card companies can easily verify who is making the purchase without transmitting a static code that could be intercepted and used by fraudsters to make future payments.

"We've integrated security from software and hardware," he said during the company's presentation on Tuesday. "We create a device-only account number and put it in the Secure Element. No longer have the static code on the back of the card."

Additionally, Apple's fingerprint scanner, TouchID, helps ensure the person making the transaction is authorized to use the credit card accounts stored in the secure element on the device.

Of course, Apple isn't the first company to employ such technologies. Tokenization will soon be available on new chip-enabled credit cards. And other device makers, such as Samsung, have incorporated fingerprint authentication in their smartphones to unlock mobile wallets. PayPal announced in February at Mobile World Congress that the fingerprint-reading technology used on the Samsung Galaxy S5 would be used to unlock its PayPal mobile-payment app.

Still, Apple played up security as a major reason why consumers should use an iPhone to make an in-store purchase rather than a credit card. Of course, some have viewed Apple's claims as ironic coming off the Apple iCloud security scandal that surfaced last week. Apple was criticized for weak security measures on iCloud that may have allowed hackers to access private photos of celebrities.

"This may be why [Apple CEO] Tim Cook and Eddy Cue made it clear that Apple will not be taking your credit card number," Wester said. "They know that consumers are very sensitive about security when it comes to financial information."

The big question is whether Apple's pitch of improved security in addition to an improved user experience will actually get consumers to change their behavior, as well as get merchants to upgrade their payment terminals.

Donna Tam contributed to this story.