What the mobile payment craze is really about: Coupons!

Everyone's talking about paying for stuff via smartphone. But you already have a credit card -- so here's how your phone will really pitch in.

Your smartphone is going to get more adept at handling money, but maybe not in quite the way you've been imagining it would.

There's been a lot of talk lately about mobile payments and how new apps or NFC technology will let you pay for things with your smartphone. But the truth is that this market is less about finding a new way for you to pay for things and more about offering you an easier way to carry and redeem coupons and special offers.

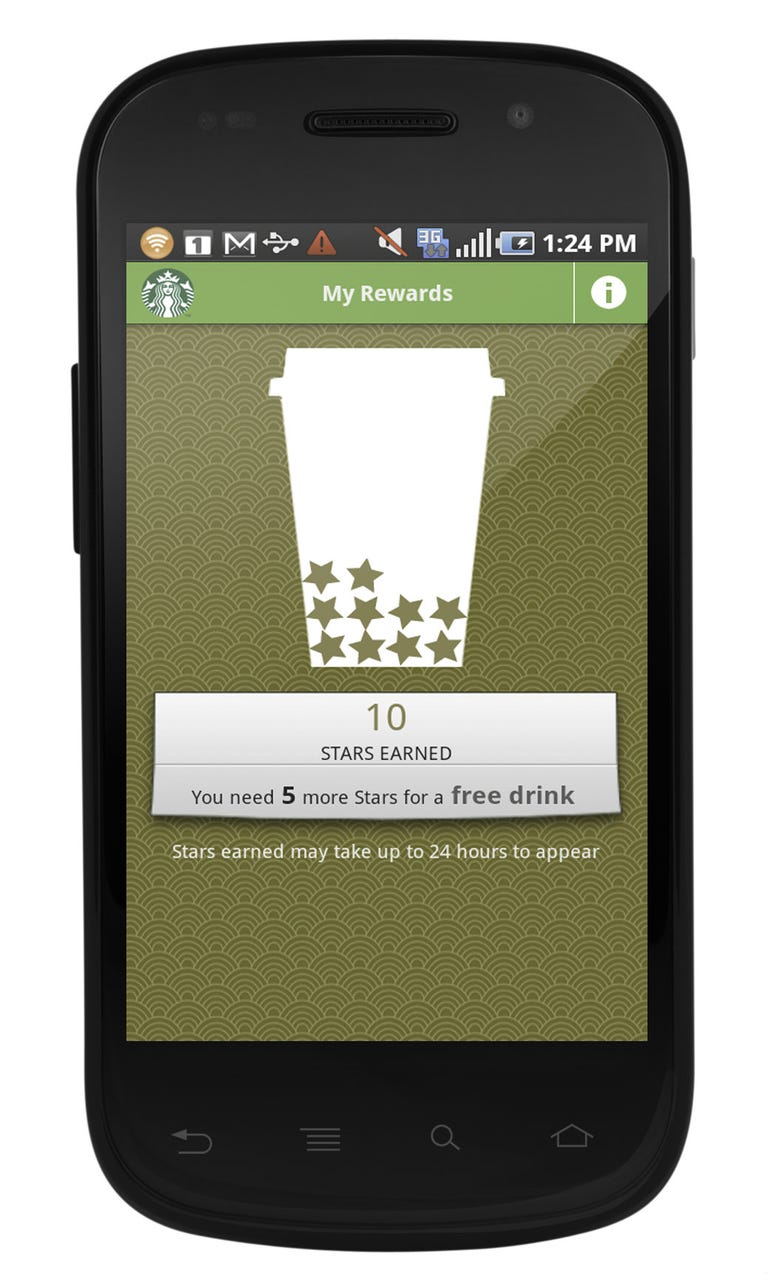

What's the most successful mobile payment system to date? It's an application that can be downloaded onto your phone to pay for coffee. Yes, the Starbucks app, launched in January 2011, has processed 55 million transactions, the company has said, adding that it processes more than a million mobile phone transactions per week. The app, which is quite simple, uses a bar-code-like technology to scan your phone. But that's as far as it goes -- it's a payment app used by only one merchant.

Then why is it so popular? It's not because you can pay for a latte with your phone instead of pulling out cash or a credit card, but because it's also your loyalty card. It keeps track of how many times you've visited the store and what you've purchased so that Starbucks can push you more offers and coupons that keep you coming into its stores. And the beauty of integrating this into a mobile app is that you don't have to carry around that card on a key chain or tucked into your wallet. It's always with you on your phone.

It's this concept of digitizing things you often carry in your wallet that has customers excited, says Jaymee Johnson, director of marketing for Isis, a new mobile payments company established by three of the nation's largest four wireless operators.

"I can give you a better way to pay," Johnson said in a recent phone interview. "But that's not broken. It's not too taxing to pull out a plastic credit card from your wallet. But what mobile payments also give you is a way to manage your loyalty cards and your financial life."

In other words your "digital" wallet is where you can store all your loyalty cards, coupons, receipts, and even some day your driver's license. These apps also have the potential to give you real-time banking and financial information, so that you know how much money is in your account.

But it's the couponing and special offers that consumers get from using these apps that will drive usage most immediately. With the growth of local daily deals services like Groupon, and with the use of coupons on the rise, consumers are looking for more convenient ways to redeem rewards. According to the retail trade publication Retail Gazette, 58 percent of consumers now shop with coupons. And coupon use has grown by 40 percent in the last four years.

Isis's Johnson said people are tired of carrying around wallets bursting with paper coupons and key chains overloaded with plastic loyalty cards.

"The ability to put all of that on a device that you carry with you 24/7 and offers an added level of security is a big step forward," he said. "That is what consumers get excited about when we talk to them about mobile payments."

Big opportunities

Juniper Research estimates that the mobile market could be worth about $670 billion worldwide by 2015. Forrester Research's numbers are a bit more conservative, estimating that mobile payments in the U.S. by 2016 could be worth $31 billion.

It's big numbers like these that have enticed Starbucks and other companies eying this market. Earlier this month, more than a dozen retailers including Target, Best Buy, and Wal-Mart announced that they are joining forces to create their own mobile payments app that can be used in all their stores. Google and eBay's PayPal are already in the market with their own versions of a digital wallet and mobile payment system. And the carrier joint venture Isis plans to launch its mobile payment system this month in its first two cities, Salt Lake City and Austin, Texas.

What's more, other players are also in the market, including the startup Square, which started out offering small merchants a way to process credit card transactions with its postage stamp-sized card reader. Now the company, which is backed by a $25 million investment from Starbucks, has the "Pay with Square" app that allows users to pay for things like a cup of coffee via the mobile app.

Google Wallet Product Manager Robin Dua acknowledges that the crowded field of players is a bit confusing.

"In the near term we're going to see quite a few companies out there in the mobile payments market," he said. "But there will be a shake-out. In the end, there won't be thousands of wallets like there are today."

At this point, it's unclear who will win the day. The retailers teaming up to build their own mobile payment app haven't been clear about how they will build the app or what technology it will use. Partnerships could form between companies that today seem to be rivals. For example, if retailers use near-field communications, or NFC -- the technology that Google Wallet and Isis use, allowing people to tap their phones to a terminal to make payments -- there may be opportunities for the companies to work together. The big motivation in working together is that Google and Isis may provide the technology, while the retailers could provide the processing capability that sidesteps or minimizes the credit card processing fees they often complain about.

Currently, Google Wallet and Isis are not involved with the processing piece of the payment business. And it's not likely they will try to compete in that world anytime soon.

"From our perspective, we leverage the existing processing and fee structures that are already in place," said Google's Dua. "Processing a Google Wallet transaction fits into the existing fee structure already negotiated. There is a reason that the four-party system for payments works well. Everyone brings something to the table."

Slow start

One thing is clear, the market for mobile payments is off to a slow start. For years, everyone from handset makers like Nokia to credit card companies talked about the promise of paying with your phone. But so far the concept has not taken off. Google has been in the market for a year now with Google Wallet, but it's gotten very little traction. Part of the problem was the fact that the NFC technology necessary to complete the transactions was only on a handful of devices. And the company also had a hard time adding banks and credit card issuers to its network.

To help rectify the latter issue, Google has recently changed how the service works so that it can scale the number of credit cards it supports. Instead of adding individual cards to the virtual wallet on the phone, Google has put all the credit card information in the cloud. And users can utilize what used to be known as a Google Checkout account to make payments from any credit card stored in that wallet from their smartphones.

The lack of NFC-enabled phones in the market continues to be a problem. For more than a year proponents of the technology have said that massive deployments of NFC-enabled devices were just around the corner. Last summer, Bill Gajda, head of Visa Mobile Global, said he expected dozens of Google Android devices to have NFC technology embedded by the end of 2011. Now it's the middle of 2012, and there are still few NFC devices on the market. And at least one wireless operator, Verizon Wireless, is still blocking the functionality on its network.

Isis's Johnson says that NFC devices are coming. And they will proliferate through the market quickly.

"There will be a number of announcements in the coming weeks and months with devices that have NFC," he said. "And given that the average consumer buys a new phone every 18 months, the technology can diffuse through the market very quickly."

Indeed, the new crop of Microsoft Window Phone 8 devices expected to be announced this fall will have NFC. Samsung announced the first such device in Berlin last week. And Nokia is expected to announce its first version of a Windows Phone 8 device with NFC embedded this week.

What will Apple do?

The big question hanging over the market now is whether the upcoming Apple iPhone, expected to be announced September 12, will have NFC. Rumors over the past several months indicate that the company will include NFC in its latest device. The addition of electronic ticket organizer Passbook to iOS 6 helped fuel rumors that the iPhone would enable mobile payments. And many experts assumed that would be enabled via NFC.

But earlier this week, a blog called AnandTech argued that the iPhone may in fact not include NFC. And it's possible that if Apple is enabling a payment system via the Passbook function in iOS 6 it may do so using some other type of technology such as low-energy Bluetooth, or even a QR code-based payment system like the one used in the Starbucks app.

PayPal says the answer is to forget NFC, which requires special technology on devices and on terminals. Instead, it has a completely different approach that requires entering a phone number and PIN as opposed to an NFC chip in a smartphone. Its cloud-based mobile payment system that links your PayPal account to credit cards is accessible by some 50 million mobile users.

"History has shown us that unless a new technology saves you time or money, it won't reach mass adoption." said PayPal spokesman Anuj Anuj Nayar."NFC is a tech in search of a problem. Tapping a phone against a reader is no faster than swiping a credit card."

But the one thing that's missing in PayPal's approach is the direct connection to the mobile device. Because consumers don't even need to have their phones with them at the point of sale, it's more difficult for retailers to get coupons and offers to users as they are shopping. By using NFC, Google and Isis are tying the wallet directly to the phone, which means that other features on the device, like GPS, can be used to target a users' location.

For example, the Gap may know you are in the mall shopping based upon the fact that you've used your phone to purchase lunch at the food court, and it might then send you a 20 percent off coupon if you purchase something from the Gap in the next two hours.

Knowing users' locations is very important to merchants in targeting consumers. NFC enables location-based offers because users have to tap their devices to complete the sale. Google's Dua says this is something that simply can't be done with plastic or by typing in a phone number and PIN.

"The credit card in your wallet or typing a phone number into a terminal have limited interactivity," he said.

For consumers it may not matter which technology is used to enable mobile payments. In the end, the mobile payment systems that will stick around will be the ones that offer consumers the most value and ease of use in redeeming coupons and scoring good deals.