Thrive gives automated financial advice

Algorithms tell you where to park your money and which debts to pay.

There's yet another free online finance site to check out if you're interested in having a computer tell you what to do with your money. And, honestly, if you're like most people, it probably wouldn't be a bad idea. This one is called Thrive. It's designed for young professionals (people in their 20s and 30s) and is differentiated by the level of advice it offers. CEO Avi Karnani wants this group of people to have access to the same level of insight and intelligence that financial planners provide for the affluent.

But first, a bit about Karnani. Before starting this service, he worked in institutional finance, in hedge funds and arbitrage. When I found this out, I asked him, "And we're supposed to trust you?" His response: "I know just how complex finances are. And what's done for people who have more money is vastly more beneficial to them than what's offered to people without a lot. It shouldn't be that hard to do, there just haven't been companies that wanted to do it.

Like Mint and other financial sites (see Buxfer, Wesabe), Thrive goes out to financial institutions on your behalf and collects all your spending, debt, and investing data. It shows you where your money is and categories your activities. That's the cost of entry in this space.

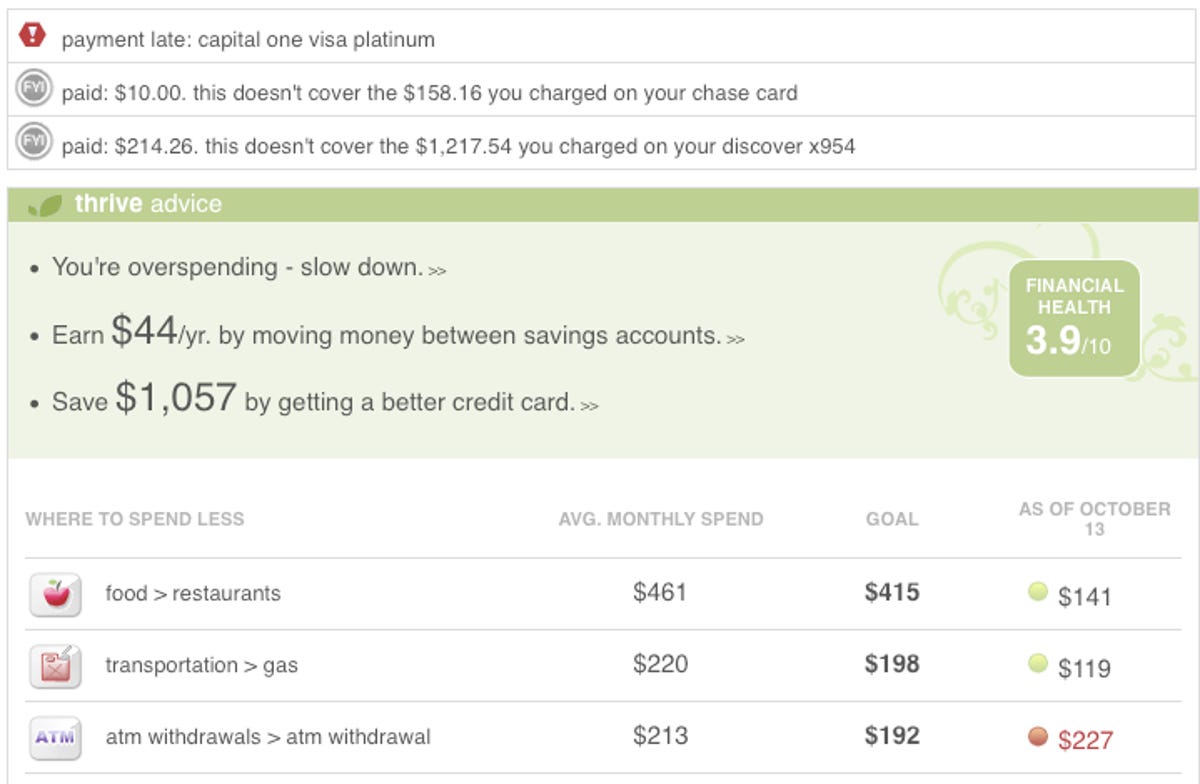

Thrive then looks at your activity, and comes up with recommendations to help you best manage your money. It will advise you on how best to pay down your debts, how your cash should be distributed among your checking and savings accounts, and where you should be cutting back on spending. There's no social angle in the service, yet.

Karnani told me the Thrive won't advise you to cut back on things you can't, like your garbage bill or mortgage, but it will come up with three achievable goals at a time for each user. In my case, they were all spending reductions: It advised me to cut back 10 percent on cash withdrawals, travel, and groceries. I looked at the advice and thought, I can do that. "It's a lot easier to make changes in your day to day purchases," Karnani believes, which is one of the reason the service gives you mundane budget advice as well as allocation plans.

The service gives you an overall financial score, which it calculates for you based on your spending, your retirement planning, your ready access to cash for emergencies, and 11 other "dimensions," Karnani told me. In the future, the score will also take into consideration your credit score (via a new partnership with Credit.com), and when it gives you advice it will factor in how things will affect that score.

Advice on what to do with your stocks is forthcoming, and I'll be curious to see how the site handles speculative investments.

I found that Thrive's presentation of current financial activity less comprehensive and useful than Mint's. Thrive's advice is better, though.

To use the service, you have to get past the fear of giving it your financial passwords. Karnani told me his site is as secure as Mint, and uses a similar architecture to safeguard financial data.

The company has raised about $2 million from undisclosed investors. Thrive makes money from referral fees to banks, and Karnani emphasized to me that the site's advice engine is completely independent of its business relationships. The product will be unveiled at the Finovate conference Tuesday in New York.