Mint: Solid but incomplete online personal finance

The early beta of Mint reveals a well-thought-out personal finance site that's missing important features.

Mint is an online financial management service, clearly designed to compete with Intuit's Quicken and Quicken Online. Unlike many of the existing online banking and budgeting products, you won't run out of gas with this product too fast, although it does not have the depth of software like Quicken.

The product has an interesting business model: It's free. Mint makes money for itself, and for you, by looking at your spending habits and your accounts and recommending offers that will save you money. Got a high-interest credit card? Spending too much on DSL? Mint's advertising network will match offers from its partners to your particular situation. Mint's consumer pitch is that it will save you thousands of dollars a year if you listen to its paid advice. (Not all of its advice is paid, a spokesperson told me, but selling those alerts is the Mint business plan.)

I'm not a fan of software that tries to either nanny or nag me, but I can't fault this business model. We are all leaving money on the table in our personal accounting, and having a tool to point us to easy ways to save some money is a great idea. And even if you don't respond to come-ons, you'll probably find its personal spending trend tracking and budget features illuminating. In contast, Quicken, while it offers deep management options (stock tracking, 401ks, transfers between accounts, custom reports, integration with tax software, etc.), is becoming a buggy, overfeatured product, and is overkill for people either just starting out their financial lives or who have simple accounts.

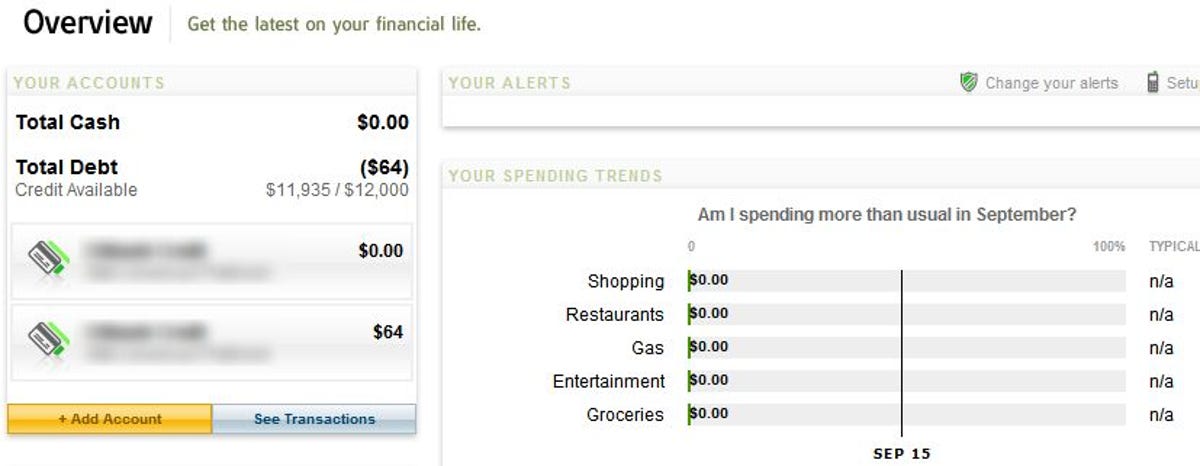

Mint does have some important Quicken-like features. Most importantly, it will interface directly with your bank and credit card companies (there are 3,500+ institutions on the system, the site says) to keep your accounts up to date. That makes Mint not just a budgeting tool but a way to keep track of accounts without going to a bunch of different sites. You can also configure the product to send you e-mail or mobile alerts when certain conditions are met, such as accounts dropping to certain levels, bills coming due, or when large purchases are made on credit cards you're tracking.

Two important features I did not find in the preview I had access to: Online bill payment, and income tax help. These are two great benefits of using electronic accounting: not having to write checks by hand or fill out tax forms from scratch. I presume these features will come to Mint, because without them, the service's utility is only a fraction of what it should be.

Also, you've got to trust Mint with your most important IDs and passwords to get it to work. One of the reasons I didn't evaluate Mint as comprehensively as I do other products is that I'm not about to give it access to my checking or credit card accounts. Mint is a well-funded company, not a garage operation, but putting this info on a startup's Web servers still gives me the willies.

The company is presenting at the TechCrunch 40 event.