Why You Can Trust CNET

Why You Can Trust CNET Advertiser Disclosure

Surprising ways to get cash back without even trying, from your credit card and more

You already know about rewards credit cards, but if you're not using these other options, you're missing out on even more dough.

Getting cash back on your purchases can be easier than ever.

Remember how much of a pain it used to be to get cash back through a rebate? For $20 back on, say, a new printer, you had to fill out a form (sometimes several), cut out a UPC, mail everything to the manufacturer, wait eight to 12 weeks and hope that maybe, just maybe, that rebate check would land in your mailbox.

The horror. The horror.

These days, it's a lot easier to get rebates -- except now they're called "cash back," and the process is almost entirely automated. So automated, in fact, that it can seem almost too good to be true.

Good news: It's not. By leveraging one or more cash-back tools and services, you can save money or earn rewards -- not just on a select few items, but on nearly everything you buy. Let's take a look at the various options.

Read more: The best tax software for 2020

Cash-back credit cards

Use a cash-back credit card on your purchases to double up on rebate savings.

I'm not going to spend a lot of time here, other than to say that if you're not using a cash-back card, you're literally throwing money away. It's the easiest and most straightforward way to recoup a percentage of nearly everything you buy.

Let's say you use a card that awards you one point for every dollar you spend. In most cases you can redeem those points for travel, goods, services or the like. You can also convert them to "cash," which usually takes the form of statement credit. You probably won't get a check in the mail, but you will get credit applied to your account -- which is kind of the same thing. It's money, however you look at it.

When searching for a cash-back card, pay attention to the percentages you'll get back -- and the annual fees. For example, there's the Uber Visa card, which pays you back 4% on restaurant and bar purchases, 3% on hotels and airfare, 2% on online purchases (including Uber rides) and 1% for everything else. It has no annual fee.

Those points may not sound like a lot, but it adds up. Let's say your monthly credit card bill is $2,000. Assuming you always pay it off in full, and you get just 1% back, that's an extra $20 in your pocket every month -- or an extra $240 per year. For doing nothing.

Cash back for online purchases

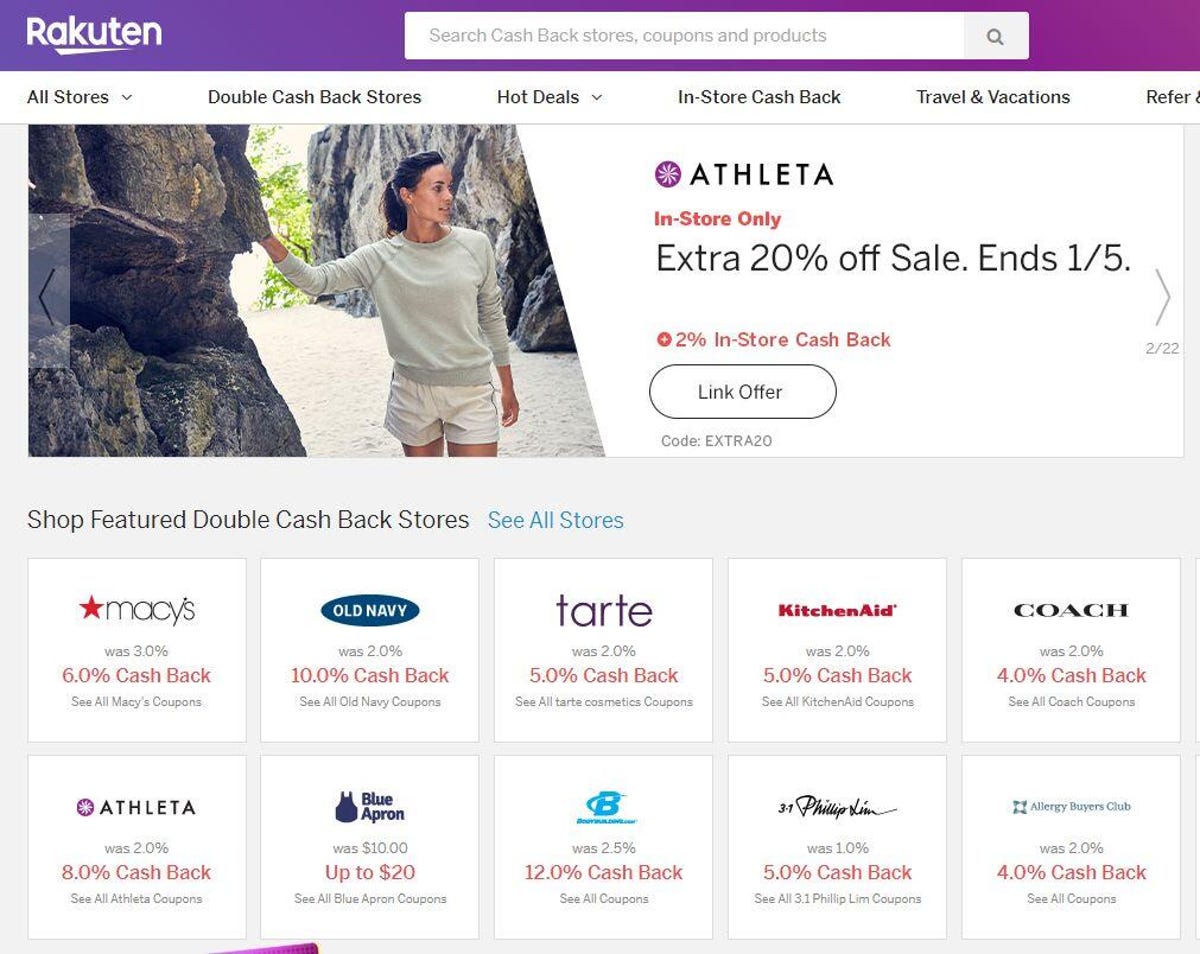

Rakuten (formerly Ebates) offers cash back from a huge number of online stores, but also has some in-store options as well.

Here's a hypothetical: You need a new fridge. You do some research, find a model you like, then proceed to shop around online for the lowest price on that model. Turns out it's at JCPenney.

Then, remembering the sage advice of one Rick "The Cheapskate" Broida, you head to cash-back service Rakuten (formerly Ebates), where you discover you can get a 3% rebate on JCPenney purchases. So you click through from Rakuten to the JCPenney online store and order your fridge like you normally would.

Not long after, you get a $51.42 credit. After that, you receive an actual check (or PayPal deposit). For doing almost nothing.

Full disclosure: That wasn't a hypothetical. It happened to me. And it's why I've been championing online cash-back services for years. They're easy to use and come with no strings attached. (Actually, I guess there's one string: Rakuten and similar services collect data about where you shop and what you buy. Some people are bothered by that. I'm not.)

Over time I've recouped hundreds of dollars I'd have otherwise forfeited. Little purchases here, big ones there. It adds up. Here are two services I recommend checking out:

- Rakuten: Rakuten is arguably the best-known service of its kind -- or, at least, it was before the inexplicable name-change. I like it for its simplicity and reliability. Its browser plug-in makes it easy for me to check if there's a cash-back option for any given store, and its apps support mobile cash-back shopping. (Many, if not most, cash-back services require a desktop browser.) The service is also among the few to support in-store cash-back shopping as well. Every 90 days, Rakuten pays out your rebates in the form of a check or PayPal deposit.

- Honey Gold: Built around a browser plug-in that finds discount codes at store checkout pages and tracks price histories at stores like Amazon and Best Buy, Honey Gold takes a different approach. "Each reward is a surprise," it says, meaning the cash-back percentage remains a mystery until after the purchase. It could be, say, 1-5% at eBay, 1-10% at Walmart and so forth. This isn't straight-up cash back, however. Points can be redeemed only for gift cards, and only at about a dozen stores. Use Honey Gold only if you can't find a cash-back option from one of the other services.

One important thing to note: If you use any of these tools in a desktop browser, be sure to deactivate any ad blocker you might be using -- at least for the service itself and the store you're visiting. Using an ad-blocker can interfere with the necessary tracking, meaning you might not get your rebate.

Cash-back services for credit card purchases

A growing number of services offer a computer-free way to score cash back. By linking your credit card, you can nab those extra savings just by shopping like you normally do. Go to restaurants, book hotels and buy stuff like usual, and presto: cash back. And, yes, they work even if you're already getting cash back from the card provider. Double-dip, anyone?

The only catch is that you don't get rewards everywhere, only from stores that participate in the given program. So you may have to do a little advance recon.

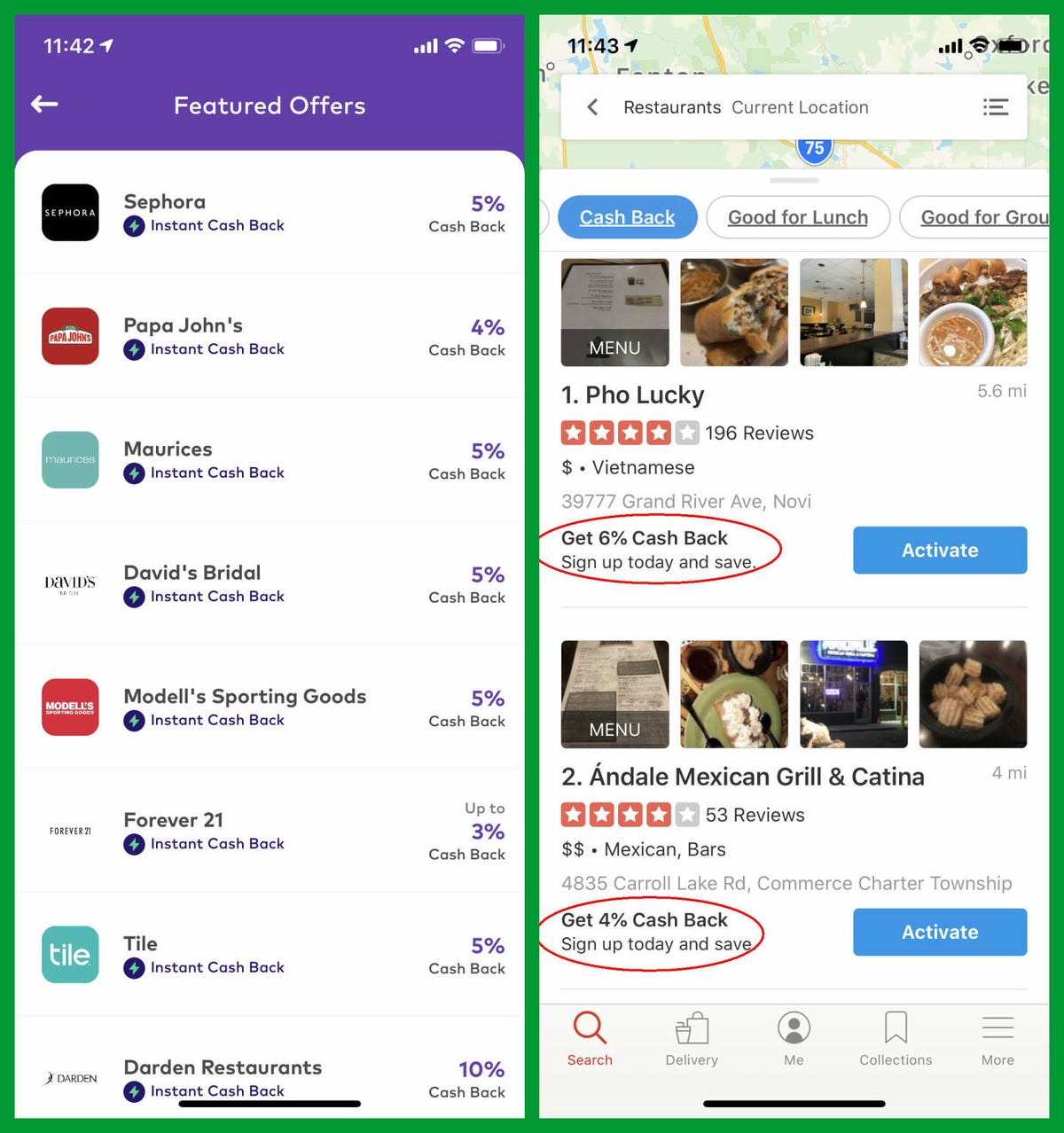

Dosh and Yelp Cash Back link to your credit card to automatically give you extra cash-back savings at participating stores, restaurants and services.

Here's a look at three of these services, all of which I've tried and can definitely recommend.

- Dosh: Launched in 2017, Dosh has evolved into one of my favorite cash-back services. Just link one or more credit cards to your account, then browse the available offers. Those typically include not only local restaurants and businesses, but also national chains (such as 5% at Sam's Club) and online stores (3% at Old Navy, for example). The app recently added cash back for hotel reservations, too. Payouts can be donated to charity or routed directly to your bank or a PayPal account.

- Drop: Similar to Dosh, but with a points-for-gift-cards system in place of actual cash, Drop works on a combination of ongoing and one-time offers. You can pick up to five "favorites" that earn you points with every purchase, from places like Starbucks, Walmart, Whole Foods and Uber. As for the one-time offers, they're for things like "30 points for every $1 you spend at Zenni," and "15 points per $1 spent at Apple." Generally speaking, I don't love this kind of structure, but it's so easy to automatically earn points (and therefore rewards) by shopping at your favorite stores, I definitely recommend Drop.

- Yelp Cash Back: I'd call this "Dosh for restaurants," because it works much the same way: Link a credit card, dine out at selected restaurants, earn cash back. Unfortunately, a single credit card can't be linked with both Dosh and

Yelp

, because both leverage third-party ecommerce company Empyr for the actual payments. And that explains why I noticed a lot of overlap between the two, both in restaurants and cash-back percentages. Consequently, you stand to save more overall by using Dosh, but if restaurants are your focus, Yelp Cash Back is certainly worth a look.

If you're not wild about giving your credit card number(s) to services like these, I can certainly understand that. Do, however, note that your numbers are encrypted, all credit cards have protections in place to safeguard you against fraud and your card is already on file at any number of stores and services. So what's one more, especially if there's money in it for you?

Post-purchase cash-back services

There's one more option for dipping into the cash-back till. Post-purchase services provide rebates after the fact -- usually by looking at your receipts. (And if that raises privacy concerns, well, I'm kind of surprised you even made it this far. But keep reading.)

Let's take a look at two notable options, starting with one that can score you price-match refunds without you lifting a finger.

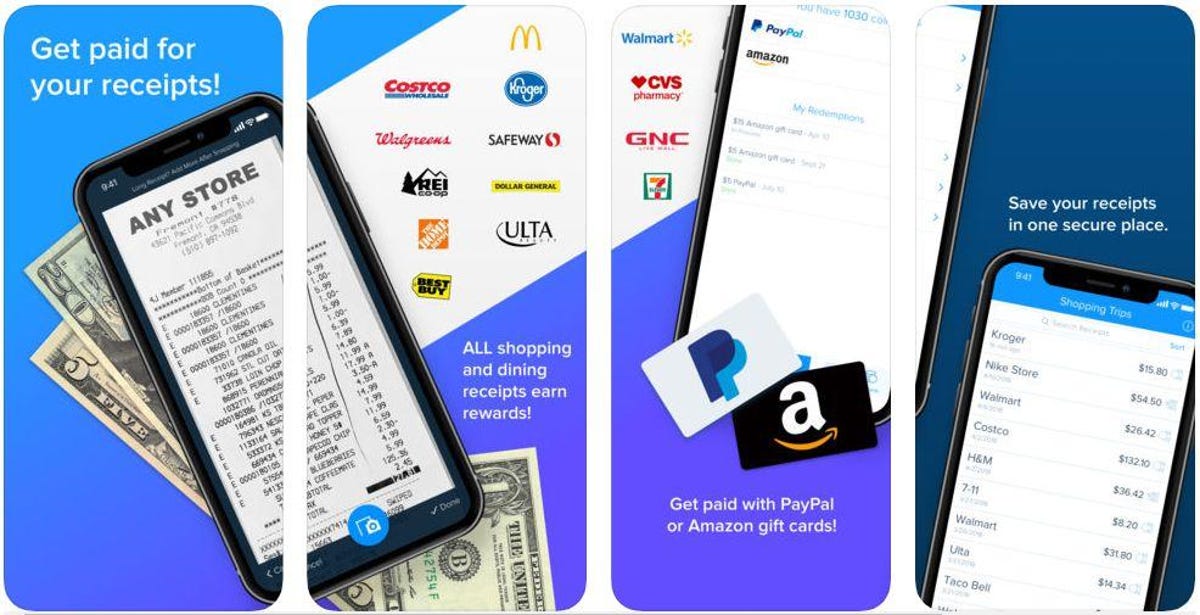

You can use an app like Receipt Hog to turn your receipts into cold, hard cash (or gift cards).

- Paribus: Many online stores offer price-matching and purchase protection. So if you buy something and then the price drops, you can get a refund for the difference. Paribus tracks your purchases and, when a lower price is found, contacts customer services on your behalf to get that refund. There's no charge to use the service, but you do need to let it monitor your email so it can automatically locate receipts. Fortunately, there's this big disclaimer right up front: "We don't sell or share your data to third parties." Note: Paribus compensates us when you sign up for Paribus using the links provided.

- Receipt Hog: Mind sharing your paper receipts for market-research purposes? If not, scan them with Receipt Hog. Each one nets you coins you can eventually redeem for cash or gift cards. You can also earn coins by completing surveys, connecting email and Amazon accounts and playing the "hog slots." Honestly, I don't love this app, largely because it requires full-time location access. There are similar apps, such as ReceiptPal, that can also work with electronic receipts. Even so, I feel it's too much work for too little reward. But it's another form of cash back, and therefore worth a mention.

If you're wondering why I didn't include the popular Ibotta in this story, it's because the app requires a fair bit of hoop-jumping. For example, to get cash back on grocery-store purchases, you have to claim offers before you shop, then remember to submit your receipt after. And to claim offers, you have to answer questions about your household, education and so on. You can definitely save money with Ibotta, it just requires more effort.

Likewise, there are lots of other tools and services I didn't cover here. If you're using one of them and think it merits a mention, by all means do so in the comments!

Originally published last year and updated with new information.