With IPO coming, Lending Club starts pulling out the stops

Apparently feeling some competitive urgency, the dominant peer-to-peer lending company has accelerated its expansion -- and reversed its profitability for now.

- Shankland covered the tech industry for more than 25 years and was a science writer for five years before that. He has deep expertise in microprocessors, digital photography, computer hardware and software, internet standards, web technology, and more.

Lending Club makes the peer-to-peer loan business, which connects individual borrowers and lenders, look easy. But it's not.

The company has shown fast, steady growth in its business for years, staying ahead of competitors and making old-school banks look increasingly like relics. Capping the company's progress was Wednesday's regulatory filing detailing its plans to raise as much as $500 million in an initial public offering.

But the regulatory filing, along with Lending Club's recent moves, shows a sense of urgency. With competitors like Prosper nipping at its heels, Lending Club is angling for faster expansion into new lending markets.

That's why Lending Club added small-business loans in March and acquired Springstone Financial in April, which extends the company into medical and student loans. But all that expansion helped push the company into the red for the last six months after finishing a profitable 2013. Perhaps Lending Club has concluded it was time to leave behind the more conservative approach that characterized its early years.

If Lending Club's expansion succeeds, it's more likely that it will be the company that hooks you up when it's time to buy that new car, send the kid to college, or pay off that high-interest credit card. And those with money to save will be more likely to lend it out for vastly better interest than the near-zero rates that bank savings accounts offer today.

The expansion comes at a cost, though.

Increasing expenses

In 2011, Lending Club had a net loss of $12.3 million on revenue of $12.5 million. In 2012, that went to a loss of $6.9 million on revenue of $34 million. Things turned around in 2013, with net income of $7.3 million on revenue of $98 million.

But its increasing expenses whacked that profitability. Comparing the first six months of 2013, Lending Club's sales and marketing expenses rose from $16.1 million to $39.8 million. Engineering rose from $5.3 million to $13.8 million. Total operating expenses rose from $35.3 million to a whopping $102.8 million.

As the saying goes, you have to spend money to make money.

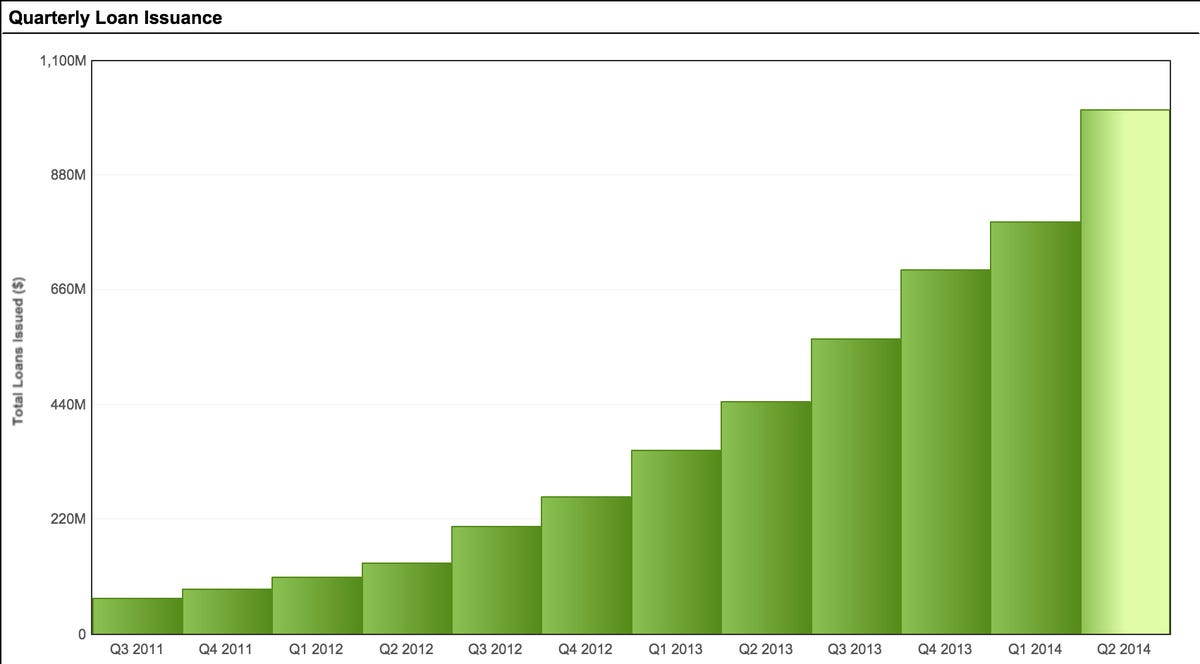

Lending Club is a juggernaut when it comes to peer-to-peer lending. As of June 30, it facilitated $5.04 billion in loans -- more than $1 billion of them in the second quarter of 2014. The chart shows the classic up-and-to-the-right direction that gets businesses salivating.

But it sees itself as actually pretty small in the scheme of things -- so far, at least. "We estimate that in June 2014 approximately $380 billion in outstanding consumer credit would meet our marketplace's credit policy," Lending Club said in the filing detailing its IPO plans.

Most loans are from borrowers consolidating earlier loans or paying off credit cards -- in other words, taking debt out of the existing financial system and moving it to Lending Club, whose loans charge lower interest rates than credit cards and pay higher rates than bank accounts.

Traditional banks take the money people deposit in savings and checking accounts and lend it out to others who need to borrow money. Typically, though, banks are more heavily "leveraged": they lend out more money than people have deposited, something that's possible because borrowers steadily pay back what they've borrowed, with interest. That's great when borrowers pay their loans back, but when lots of them default at the same time, it's a big -- perhaps terminal -- problem for the bank.

Lending Club, though, is inherently more conservative than traditional banks in some ways. The company isn't leveraged at all, because it doesn't accept deposits. Instead, it just connects those who want to lend money with those who want to borrow it, then takes 1 percent of each monthly payment for itself.

Chief Executive Renaud Laplanche told CNET the impetus for the business was the realization of just how big a gap was between lending and borrowing interest rates. In a 2013 interview, he told CNET he noticed it while looking at his credit card statement during a vacation:

I started thinking there could be a better way to get capital from the depositors to the people who need it, to the borrowers. I started digging into that spread between the 1 percent and the 18 percent. When you're an entrepreneur and you see a spread like this, you see an opportunity. It turns out my instinct was right. It goes into the operating costs of the bank. That's where we could generate efficiencies.

Those efficiencies have been put on the back burner through the company's current expansion plan, though.

Expanding to lending for small businesses, medical expenses, and student debt isn't the only direction the company is going. It also plans to expand to lending to borrowers who are a lower and a higher risk than the current spectrum of people. It will arrange loans for more than just the 36- and 60-month terms it currently uses -- something that could help it expand to home loans. And it will expand operations beyond just the United States.

It's not yet clear how aggressive the company will be in this push, but its origins indicate caution won't be thrown to the winds. Lending Club was born in 2007 and almost immediately ran into the 2008 financial crisis whose after effects still are present around the world.

Passing Prosper

Laplanche said the company's conservative approach is what allowed it to surpass Prosper, which today is the No. 2 peer-to-peer lending company.

"We've always been focused on prime consumers and on offering responsible borrowers the ability to lower the cost of their credit, and offer investors better terms than they could get from their bank. Prosper took on more risk, went deeper into the credit spectrum," Laplanche told CNET last year. "I think that really backfired in 2008."

Prosper has turned itself around, though, at least partway. According to its latest regulatory filing, its revenue for the first half of the year rose from $5.5 million in 2013 to $27.2 million in 2014. It arranged $370 million in loans in the second quarter, more than all of 2013.

Prosper sees plenty of room in the marketplace.

"This is not a winner-takes-all situation," Prosper CEO Aaron Vermut told CNET. "There is more than $800 billion worth of consumer credit card debt, and it rises to the trillions when you add in other categories, so there is definitely room for multiple marketplaces."

Prosper is growing in Lending Club's home turf, but the world is a big place, and others are trying to replicate Lending Club's success elsewhere.

Estonia-based Bondora, while vastly smaller than Lending Club, offers loans in Spain, Finland, Estonia, and Slovakia, with €22 million ($29 million) worth of loans arranged so far, said CEO Pärtel Tomberg. It'll expand to five more countries in 2015, and investors can come from all over Europe.

"I do not even see the need in the next 10 years for any of the P2P lenders to really go head-to-head for customers as the market is enormous and has a lot of niches," Tomberg said. "We are focused on becoming the largest marketplace lender in continental Europe by creating a pan-European money market."

Bigger is better?

Laplanche sees things differently. "A larger marketplace becomes more attractive just because it's larger," he said, with borrowers able to reach more investors and vice-versa.

With its expansion strategy, Lending Club has shown itself willing to pay for more growth. It wouldn't be a surprise to see more acquisitions -- of peer-to-peer lending companies in other countries, for example.

An IPO that raises something like half a billion dollars opens up Lending Club's options. "We may use a portion of the net proceeds to acquire businesses, products, services or assets," the company said in its prospectus.

Perhaps the big will be getting bigger.