Prosper CEO says P2P lending could reboot economy

Peer-to-peer lending system gets a tool to help the banks: a platform to trade small loans as securities.

In advance of the Finovate ("Financial Innovation") conference that kicks off on Tuesday in San Francisco, I talked with Chris Larsen about his peer-to-peer lending company, Prosper. The prospects for peer-to-peer lending dimmed last year when the Securities and Exchange Commission decided to regulate some of the P2P financial instruments as securities; this forced P2P lending companies to retrench as they'd previously been treated more like banks. Prosper itself shut down its lending platform six months ago.

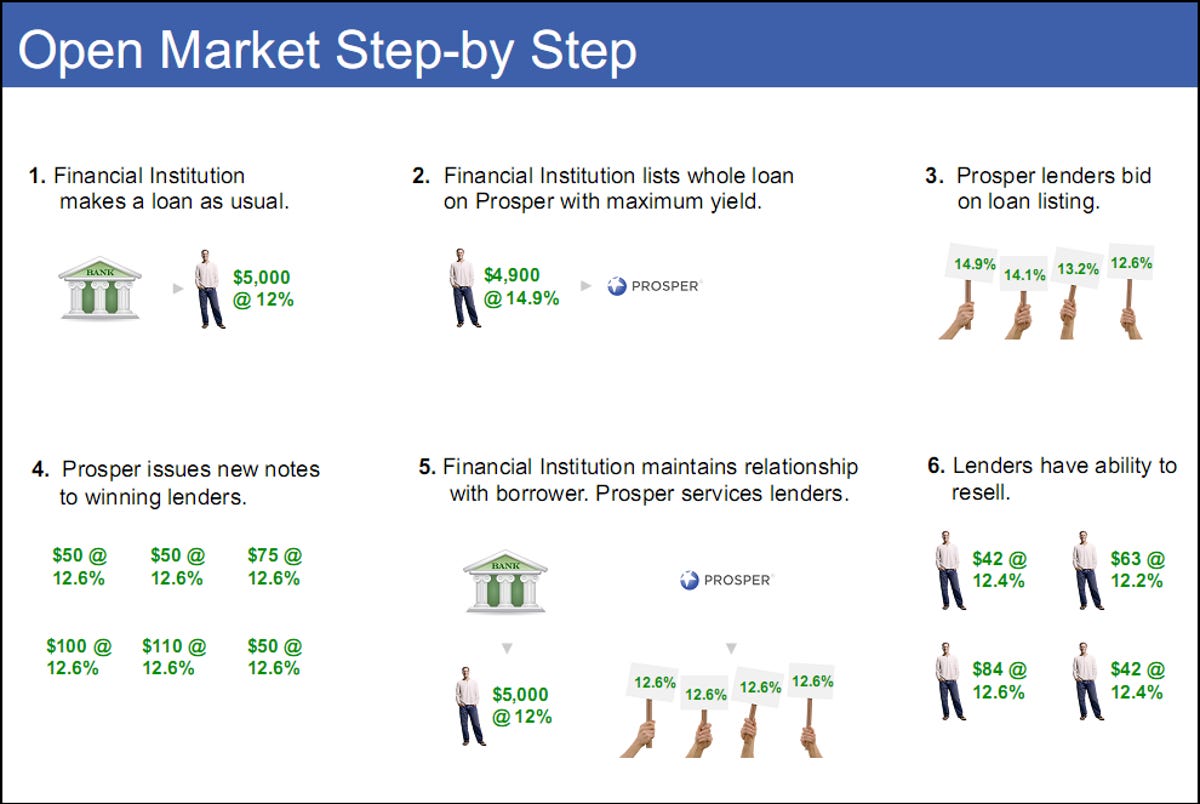

However, California in particular is getting ahead of the game and has given Prosper the green light to start up again and to operate its latest service, a trading platform called Open Market that lets any financial institution securitize (package and re-sell) its portfolio of loans to individual P2P lenders.

With the credit markets still reeling from the 2008 Wall Street collapse, Larsen says "credit in the street is needed now more than anything," and that his company's new feature enables that by providing liquidity to banks. The new loan-trading platform gives secondary loan buyers full visualization into loans currently being serviced by a financial institution.

So instead of a bunch of mortgages being collected and then rated by a rating agency, a method that obscured value and contributed to landing our economy in the mess it is in now, buyers of loan securities could see all the way down to the individual loans if they wanted, and could, theoretically, choose to buy only certain ones. Prosper securitized loan packages will be sold on auction, again providing a level of transparency to their true value.

Only loans currently being serviced--and with at least three months of payments against them--are eligible for these securities.

I'm sure I am missing some key financial details here, but the upshot is that the Prosper lending platform removes one of the bottlenecks that shunted nearly all security-related instruments through New York ratings firms.

Prosper will continue to also operate its person-to-person lending system, so individuals can loan money to, and get loans from, their neighbors. As before, options in the Prosper system let borrowers and lenders spread their transactions around. For example, if you're looking for a $5,000 small-business loan and I'm lending money via Prosper, I wouldn't lend you all of it; rather, if I had $5,000 to lend, I'd lend little pieces of that fund to people who meet the criteria I specify. You might end up with $100 of my money. This reduces risk for both of us. At least in California, where the Department of Corporations has authorized P2P lending in the state.

Larsen appreciates the "regulatory clarity" he's getting in California in advance of the federal government's SEC approval. He thinks it's fitting for California. "You can see a path to new technology in finance" in the state, he says. And, he says, a distributed, transparent loan marketplace is needed urgently. The "fragile" economy has had a single point of failure thus far, and it indeed did fail, so "this is the golden opportunity for new credit systems," Larsen says.

Prosper has about 800,000 users, Larsen says. About 100,000 of those are currently lenders. The average loan amount is $6,000, and $180 million has been leant through the system to date.

Related: Peer-to-peer lending is not dead yet