Ondot Card Control brings Find My iPhone features to your wallet

A startup out of San Jose, Calif. is handing card holders protection akin to smartphone antifraud services.

Ondot Systems was born out of a moment almost everyone has experienced: the unique mix of frantic terror and anger you feel when you lose a credit or debit card -- or in my case, three cards along with my wallet this past January.

Not only must you act fast to ensure your cards aren't used fraudulently -- even if you suspect you may have just misplaced your wallet or left your card at a restaurant -- but you have to make laborious calls to the card issuers using phone numbers you need to look up online.

With the rise of breaches, like Target's last fall, and holes like Heartbleed in the permeability of the Web's encryption tools that secure our online data, these scenarios are resulting less and less from personal errors like losing your credit card and becoming more an expectation of the world we live in today.

Ondot, a 3-year-old startup out of San Jose, Calif., hopes to alleviate this growing problem by inviting card holders to join their banks in possessing antifraud tools. The solution is Card Control, but it's not a product you can use. Rather, it's a technology that card issuers can empower you with.

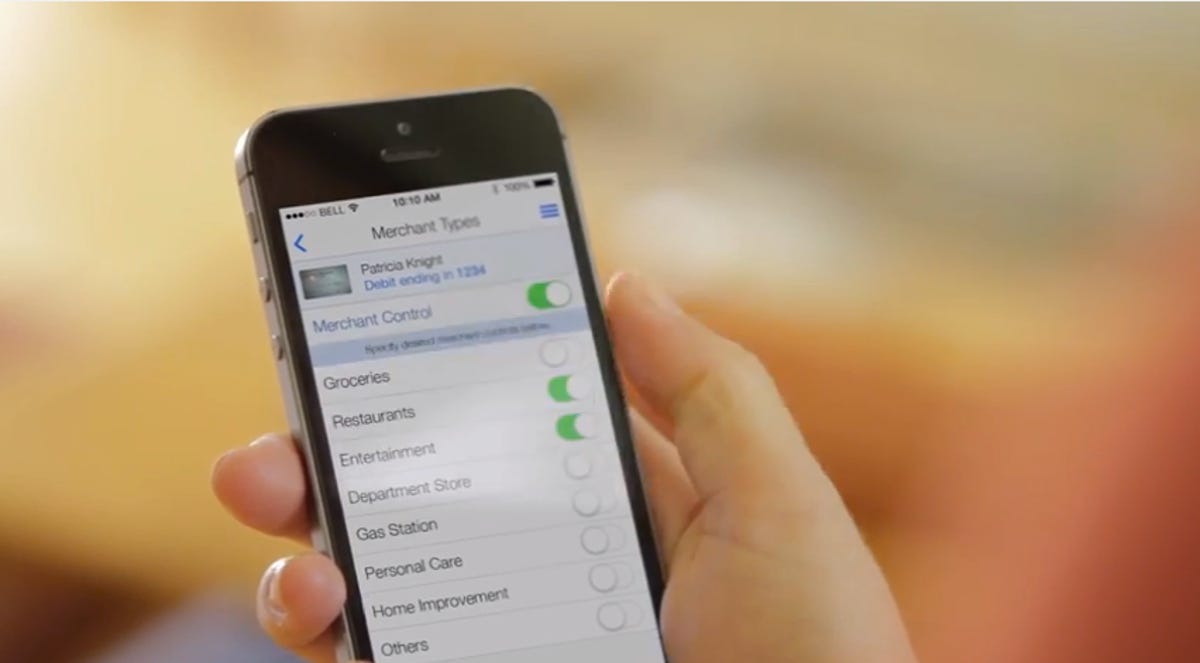

The trick: build antifraud features into an app on your smartphone that can link with your card. That turns any mobile banking service into its very own Find My iPhone app that will let users turn off and restrict a card by both location and transaction type, as well as have it notify users of any transactions immediately through push notifications.

Ondot Systems, headed up by co-founder and CEO Vaduvur Bharghavan, has been around for three years. But on Thursday it announced Card Control, alongside an $18 million round of venture capital funding. Bharghavan is no stranger to Silicon Valley; he took enterprise Wi-Fi venture Meru Networks public in 2010 and went on to found Bytemobile, which he sold to Citrix in 2012.

Ondot Systems remained dormant for a while mostly because it wasn't just developing the technology to enable users to control their cards, but it also was hammering out partnerships with major payment processors. Essentially, Ondot sits in a layer between your bank and its processor, and communicates with both to allow users to be able to remotely -- from a smartphone -- control whether or not a certain transaction is declined or approved based on a number of user preferences.

For instance, you can disable all e-commerce and only turn it on, via your smartphone with a single button, when you plan on making a purchase, protecting your card from being used fraudulently online in the event of a data breach. Or you can restrict a card to as low a level as a single ZIP code, meaning if you leave your wallet somewhere and someone tries to use the card, the transaction will be denied.

Card Control: A technology, not an app

To be clear, Ondot is not making an app. Instead, card issuers that want to use its technology simply work with their processor to partner with Ondot and incorporate its technology into their mobile banking services. Whether the card issuer wants to fold Card Control into its central mobile banking app, or spin it off into a separate app entirely, will be up to them.

"We have two product lines. One is through the processor. Any customer bank of one of our processors just has to go talk to the processor and flip a couple of switches. There's no software at the bank required," Bharghaven said. "For larger banks, we have a direct-to-bank solution where we integrate with the bank's data centers."

Bharghavan says Ondot has covered four of the seven major card processors blanketing more than 10,000 institutions, or roughly two-thirds of all banks and credit unions in the US. Most large banks, such as Bank of America and Capital One, operate as their own payment processors, which is why Ondot must integrate directly.

Ondot's business will charge banks and credit unions a subscription fee based on monthly active users of whatever application utilizes Card Control. The technology will work with debit, credit, and gift cards, and can be activated by banks for current cards no matter when they were issued.

"It doesn't explicitly need to be set up. When I set my preferences, these preferences are stored in a server and this server talks with the processor in the back end," Bharghaven explained. "When the transaction hits the processor, the processor checks with the server." There is no syncing between the card and the phone, just a communication layer. It's "very similar to how you would think of mobile banking," he added.

Ondot has not revealed which major banks are working with its technology yet, but expects to make announcements regarding partners in the next few weeks.

An active partner, however, in Ondot's testing phase has been Lone Star National Bank, which has used the technology for a year. The results let Ondot figure out how useful the app was for both users and card issuers. "Lone Star found that card holders once they use the Ondot system started using the card 52 percent more, and spent 48 percent more on that card," Bharghavan said. "Essentially, this card becomes top of wallet."

Even better, Bharghaven said, is that Lone Star actually lowered fraud by 60 percent. "Banks are thinking about this as a slam dunk," he added.

Ondot makes it clear that the goal here is not to try to supersede a card issuer's standard fraud-protection service, and that is precisely why the company has been received favorably by the typically tech-adverse.

"Fraud has been around as long as cards have. Banks have always tried to come up with preferences," said Rachma Ahlawat, who worked with Bharghaven at Meru Networks and is an Ondot co-founder and its VP of product. "But they create your purchase profile around where they expect you to do things."

For instance, if you travel and forget to tell your bank, you make a few transactions and your card suddenly gets denied. "Then you get a phone call that asks, 'Are you really in New York?' This causes a lot of denial-of-service," Ahlawat said. With Card Control, users are working alongside banks to increase protection and enable more precise control.

"In addition to what the banks will use to monitor their fraud polices, ours is for user preferences. There's another data point available," Ahlawat added. "It's your card -- now it's been personalized for where you want to use it and how you want to use it."