Facebook's IPO: Massive valuation brings business model scrutiny

Questions about Facebook's business model and growth prospects explain why GM ending an ad experiment on the social network has gotten blown out of proportion.

If GM pulled $10 million in advertising from Google no one would notice. And Ford and Chrysler already have indicated that they are going to stick with Facebook.

So what's the big deal? With great valuations comes great business-model scrutiny. Investors want the next Google. The problem with Facebook is that it hasn't quite figured out its model yet. Today, Facebook is reliant on display advertising, but we all know that your data, direct marketing, and peer recommendations are probably the future. Repeat after me: Facebook doesn't have its license to print money yet.

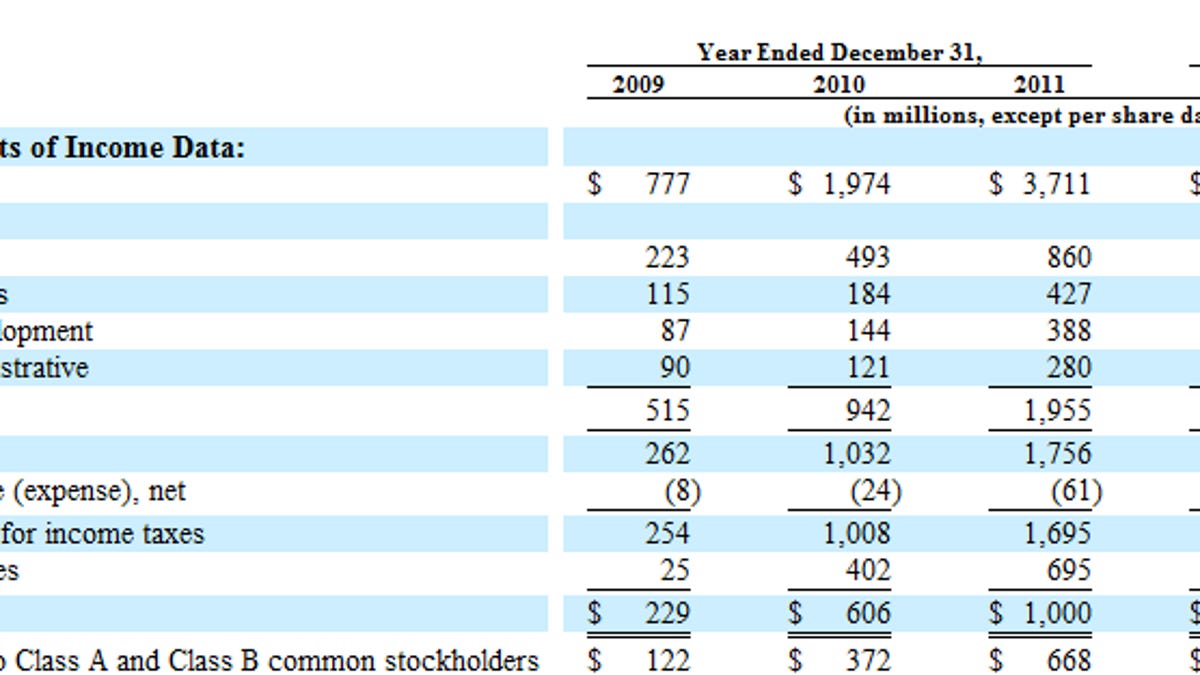

Here's the catch with the Facebook IPO: anyone buying shares on Friday and beyond will be paying up big time for a company that may or may not find a strong business model. Facebook isn't Google. And Facebook doesn't monetize as well as Google and may never come close.

Serial entrepreneur Chris Dixon, co-founder and CEO of Hunch, which was acquired by eBay, has a fine post on Facebook's business model. He gets to the point quickly:

Facebook relies on an old internet business model: display ads. Display ads generally hurt the user experience, and are also not very efficient at producing revenues. Facebook makes about one-tenth of Google's revenues even though they have 2x the page views. Some estimates put Google's search revenues per page views at 100-200x Facebook's.

Dixon argues that Google's business model better matches buying intentions with the user. You search for something and Google hits you with a relevant ad. Facebook is like a park. Perhaps you notice an ad or sponsorship, but you're not at a park to buy anything. You're there to goof around with your friends. Ads can be annoying.

Certainly, Facebook can improve with better ad targeting. And Facebook knows more about you than Google does when it comes to user data. It doesn't take a brain surgeon to reckon that Facebook can be a cash cow.

But Facebook isn't a cash cow yet. It has to figure out mobile. It has to walk a privacy line. It is dependent on users showing up. It's a company nearing the saturation point in mature markets, and China is closed to Facebook.

Eric Clemons, a Wharton operations and information management professor, has argued that Facebook's IPO is a $100 billion option on some unknown business model. He's right. Today, Facebook's valuation can't be justified under any metric.

More than enough investors will take the leap that Facebook is worth the money Friday in hopes of a more lucrative tomorrow. It remains to be seen if IPO hope today turns out to be a good investment in the future. Generally speaking, hope isn't an investment strategy.

Updated at 8:13 a.m. PT: A typo in Facebook's valuation has been fixed. The company's valuation is expected to be around $100 billion with its IPO.